I know I might get a lot of brickbats from the NBFC bulls for writing this post. Anyway, this post is an attempt to capture what I have been thinking while exiting NBFCs during the crisis. I acknowledge that my exit call may be proven wrong in the future and looking at this post, a few years down the line, people might think wow this guy got scared out of his NBFC stock holdings.

Or they may say, wow that was a good call, in the middle of a crisis. We’ll see how this plays out.

So here’s what Ben Graham, the famed role model, once said.

Notice that he puts safety of principal before an adequate return. He did not put an adequate return first. So, let’s explore how this applies to the ongoing Covid19 situation and how it concerns NBFCs (and should concern their investors). Are NBFC investors really putting safety of principal before an adequate return? Or are they prioritizing returns over potential risks that are hiding behind the curtains?

So, before the Coronavirus situation started, I was invested in 2 NBFCs, one was a popular multibagger stock and another was a lender whose loans were secured by the yellow metal. I will not be taking company names for obvious reasons and leave it to the reader to guess what those names are. I will be addressing the first company as the unsecured lender and the second as the secured lender.

Cutting losses quickly vs Staying invested for the long term is a paradox every value investor runs into, at some point in their investing journey. But what makes this game interesting is exactly this dilemma.

So here are the thoughts that came to my mind before I exited these 2 stocks.

Reasons for exiting the unsecured lender’s stock

Macro analysis is not my forte. My circle of competence lies in picking quality growth stocks at reasonable prices and I should stick to that. By investing in an NBFC or by continuing to stay invested in an NBFC today, I am becoming a macro analyzer and by definition, straying outside my circle of competence. More on this further down in the blog.

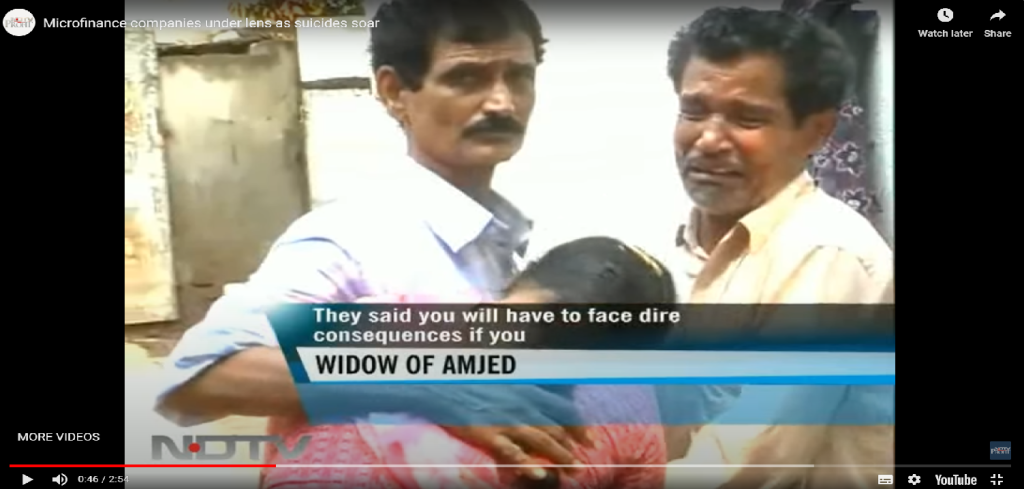

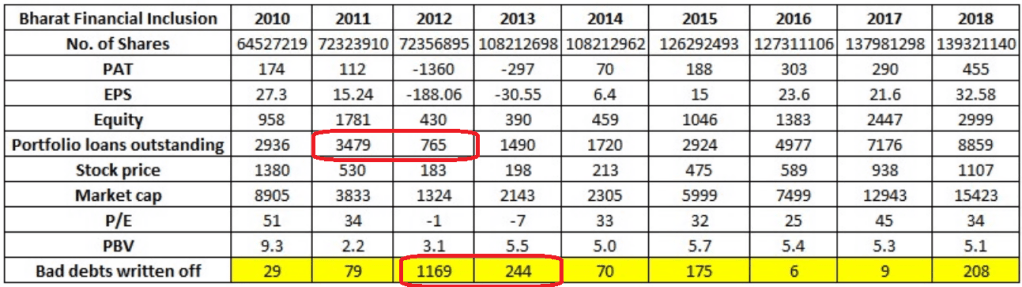

We all know what happened to SKS microfinance (subsequently renamed Bharat Financial Inclusion) when Andhra’s politicians stepped in to pass a law to protect their vote bank from loan sharks, back in 2010. Will history repeat itself and will the government intervene again and tell lenders, boss you are not going to use hard tactics to recover your bad loans. What happens to those low NPA numbers then? What happens when shit hits the ceiling? Nobody knows. And here’s what happened to SKS Microfinance and it’s continuing shareholders when a crisis happened. I realize this is not THE perfect example but what the heck, that’s the best correlation I can think of.

So here’s how the SKS MFI story played out back in 2010-11.

- SKS were an aggressive but successful MFI lending company. They had grown their loan portfolio at a phenomenal 150% between 2007 & 2010 and PAT at a staggering 250% !! The unsecured lender I was invested in, had high growth rates as well, but not nearly as high as those of SKS.

- Looking at their scorching growth, other MFI players entered the Andhra Pradesh MFI market.

- Next, bad lending and recovery practices became the new normal, for both borrowers and MFI lenders.

- What happens when you lend without checks and balances is your borrowers start defaulting and in Andhra this took a turn for the worse. Due to hard handed recovery tactics, some of their borrowers committed suicides.

- Next came the politicians who wanted to obviously protect their vote banks. Some of them might have had good intentions of protecting borrowers from loan sharks, but the crux of the story is that the AP govt. subsequently passed a law which halted operations of MFIs in the state, adversely impacting lenders’ recovery and liquidity.

- And as a consequence of this law, out of the total 3500 Crs of loans that SKS had lent in 2011, they had to write off 1400 Crs or 40% of their total loan book.

- Climax – The company’s equity shrank by 78%, from 1780 Crs in 2011 to 390 Crs in 2013. This led to the company’s stock price never coming back to the high of 1380, that it had touched in 2010, even until 2018 when the company was taken over by Indus Ind Bank. And this was despite the fact that SKS’ was trading at a princely PBV multiple of 5 in 2018. This was also despite a string of sustained growth in sales and profits between 2014 & 2018. Eight years and the stock was still below it’s pre-crisis high. WTF!!

- Will bad behavior drive out the good, yet again? How will bad borrowers influence the good borrowers in the case of the unsecured lender I was invested in? In 2010, the total number of MFI related suicides in Andhra was reported to be between 50 & 60. Can 50-60 borrowers on their own, cause an MFI to lose 1400 Crs. Mathematically speaking, no. Because the average ticket size of each MFI borrower was just a few thousand rupees. But the psychological impact of these suicides was devastating for SKS, the bad loan borrowers, the good loan borrowers, the politicians and all other stakeholders in that ecosystem, and rightly so. After all, the SKS management team might have looked the other way, when their goons were out there, in those villages, harassing their borrowers.

- What kind of an impact will the moratorium have on the unsecured lender’s borrowers’ psyche? Nobody knows. Will some of them think, not paying EMIs is the new normal? Will the moratorium be extended beyond the current 6 months? Who will bear the interest costs during the moratorium period? The borrower or the lender or the lender’s lender aka we the investors? Some folks are already disputing the logic of interest getting accrued during the moratorium period.

Next, I come to opportunity costs and cutting losses quickly. By staying invested in the unsecured lender, I was ignoring the opportunity costs of investing in other companies. At one point NBFCs had tailwinds and so I invested in 2 of those. Today, they don’t have tailwinds or at least it looks like that. So shouldn’t I be moving my money to a sector like Pharma or Specialty chemicals where I can foresee growth. Isn’t growth a core component of the GARP investing style? And if these lending companies aren’t promising me growth, why should I continue holding them? Buy and Hold does not mean Buy and Forget. It means Buy and Monitor and most importantly, act, and cut losses quickly when the time comes. As Ian Cassel put it beautifully, fall in love with companies that execute, but be prepared to divorce quickly.

I am not the proprietor of this lending company. I am a minority shareholder. And as a minority shareholder I have the advantage to move my money to a business/sector with better prospects over the next 3-4-5 years. Why would I even want to give up this advantage? As Lord Keynes had once said “When facts change, I change my mind. What do you do, Sir?” And there’s no denying that the world has changed for lenders.

Now, coming to the “somewhat secured” lender’s balance sheet. The first table shows their share of secured and unsecured loans. And the second table shows the potential downside in a case wherein, their unsecured loans go bad by 20, 30, 40 & 50%. For example, SKS had bad loans to the tune of 40% of their loan book. If such a thing happens to this secured lenders’ balance sheet, then the potential downside could be in the range of 54% or more, depending upon Mr. Market’s mood swings.

The other thing that could happen is that the MFI subsidiary will be forced to declare bankruptcy with no support from the parent and is non recourse to the parent co. This would mean business as usual for the secured lending part of the parent’s business. What would be the financial and psychological implications of such a move from the company? How will Mr. Market treat the parent for orphaning his MFI child? Will the parent’s borrowing costs go up because his kid defaulted? I don’t know the answer to this and it’s difficult to even make an educated guess, I suppose.

Another point noteworthy is that, back when the SKS crisis happened, MFIs were NOT regulated by RBI. Today, they are. So we don’t know how RBI will step in to save the MFI industry.

Subjective vs Objective probabilities

Objective probabilities are those which stay constant regardless of the external environment.

Subjective probabilities, on the other hand, are those which depend upon the probability that something will occur.

Let’s take NPA numbers of these NBFCs for example. In the past, both the secured and the unsecured lending companies, kept reporting a very good set of low NPA numbers. Now some investors might have assumed these to be objective numbers. But were they? They were subject to the following dependencies-

- The overall economy doing well.

- A subset of this was the rural economy had to do well for the secured lender’s MFI business to do well.

- And since a big chunk of the rural economy depends on agriculture which, in turn depends on monsoons, the rain gods become another factor as well.

- For their Vehicle Finance and SME lending business to do well, India’s GDP needed to keep growing at 5-6-7%. In the absence of growth, boy there are problems in an economy. Go check out the period when America’s GDP kept shrinking after the 1929 stock market crash and the subsequent recession. GDP Growth is like oxygen. It’s presence is barely noticed and it’s absence is sorely missed, as some unsecured lenders may learn, over the next few years, if not quarters.

- Do we know how long borrowers will be out of their jobs or for how long borrowers’ businesses are going to be down? No. By staying invested in this lending company we are assuming it’s borrowers will be back up, on their feet, in the next 4-6-8 quarters.

- Are we also assuming once borrowers’ incomes are back to pre-crisis levels, they will start paying back their loans immediately, leaving aside other priorities they might have deferred during the lockdown, such as paying their children’s school fees, getting their sore tooth removed, fixing their leaking roofs, taking a small vacation or whatever else. In the pre-crisis era, these same people had been programmed to borrow, to meet their requirements. But now that the lender has locked his wallet, in a safe, what will these borrowers do, in order to meet their needs and wants?

- How many of these companies’ borrowers will lose jobs? How many borrowers will close their businesses, for good? How many of those closed businesses are big ticket borrowers?

As you can see, when you think NPAs, there are so many moving parts, that making an educated guess could well be a fool’s errand. NPAs are not objective probabilities, they are subjective. Subject to the factors stated above, among so many other things.

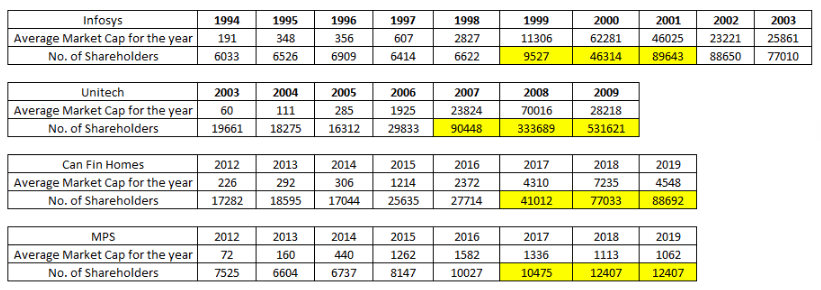

Next, I explore what happens to shareholders’ psyche during market crashes.

I think it’s lies in our sub conscious nature to catch falling knives. Here’ what the data says and as Sherlock Holmes says, it’s an error to argue against data.

As we can see, the number of shareholders almost always goes up when a sector leader falls. Even after these companies’ glorious days were over and their market caps were decreasing, the number of new shareholders kept increasing. Like everything else in the stock market, there will be exceptions to this rule. But generally speaking, this pattern plays out. So we should watch out and not fall in the trap called Anchoring bias. Could the number of shareholders increase in these 2 NBFC sector leaders in their FY20 annual reports? If I had to bet, I would say yes, this pattern is likely to be seen in NBFC annual reports for FY20 as well.

Fear of Missing Out and What if I go wrong with this bearish view that I have?

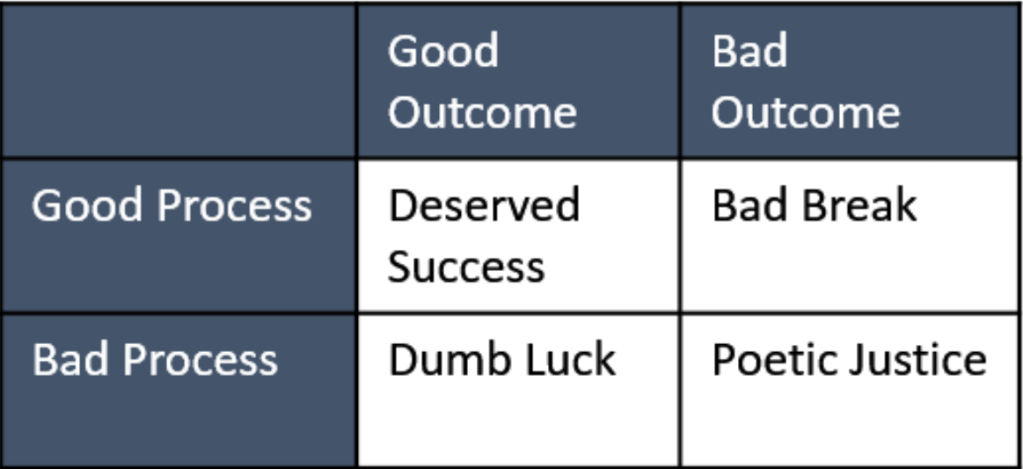

If the process of buying or selling is good, eventual outcomes will be good. In other words, I should be worried about whether or not my process is good and not what my clients will be thinking, should my sell decision go wrong and the stock price starts moving up after I sell. My duty is to have a good process, such that the outcome takes care of itself. Occasionally, a good process will result in a bad break and as a fund manager I am okay to accept a bad break, provided, the process of buying/selling was good. Should I be worried, that I will lose out on potential gains that could come from continuing to hold onto the stock? Yes that worry is real. But it comes with risks attached, that I do not want to take with mine and my clients’ money.

With that being said, I am ready for the brickbats from NBFC bulls. There’s no messenger of bad news, who doesn’t get trolled after all.