Blog on Alembic Pharma – May 2020

Every crisis brings with it, changes, and some of those changes spell OPPORTUNITY. Of course, not all opportunities pan out the way we intend them to. But what if we manage to ride one such opportunity and manage to benefit from it.

This is my first attempt to understand a Pharma business and I started deep diving only after the Covid19 situation started evolving, since I thought it might be a good idea to expose my clients’ portfolios to fast growing companies from an industry which is basically, recession proof. It would be fair to say I am quite new to this industry and have been trying to understand a very complex business. On the other hand, from my interactions with several value investors, over the years, Pharma as a sector, is a black box in a lot of value investors’ minds, due to the complexity involved, and that exactly, makes it a bias worth exploiting.

The purpose of this post is to be able to come back a few years later, do a post-mortem and understand what worked and what didn’t. My views are biased and what follows is, how I look at the situation today. My opinions could change rapidly, depending upon how internal and external factors play out over time.

On 21st March, Donald Trump tweeted this.

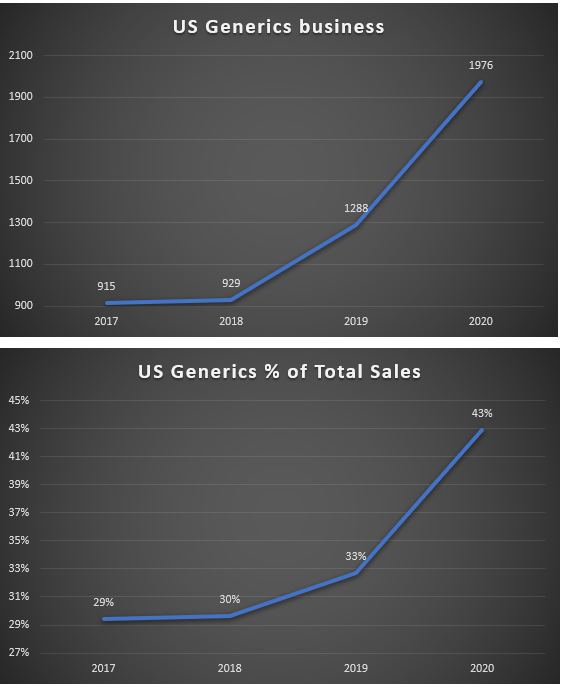

There are quite a few listed companies that produce Hydroxychloroquine & Azithromycin. So here’s what differentiates Alembic Pharmaceuticals, a company that I started investing in, in Sep 2019. My initial reason for buying was the company was growing well, was run by a fantastic management team and the price was attractive, given the growth numbers.

What the company sells..

What are Generics / Generic Drugs?

Generic drugs have a similar chemical composition as branded drugs. They are accepted globally and are of the same quality with a lesser cost as compared to branded drugs. Along with no compromise on quality, they are also cost-effective as the cost of R&D and drug discovery is not included in the case of generic drugs.

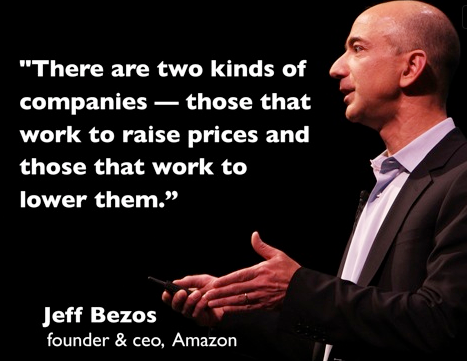

Generic drug manufacturers like Alembic fall in the latter category because they help reduce prices of essential drugs vs companies like Valeant Pharmaceuticals which work to increase prices. We all know what happened to Valeant and some of it’s very savvy investors, a few years ago.

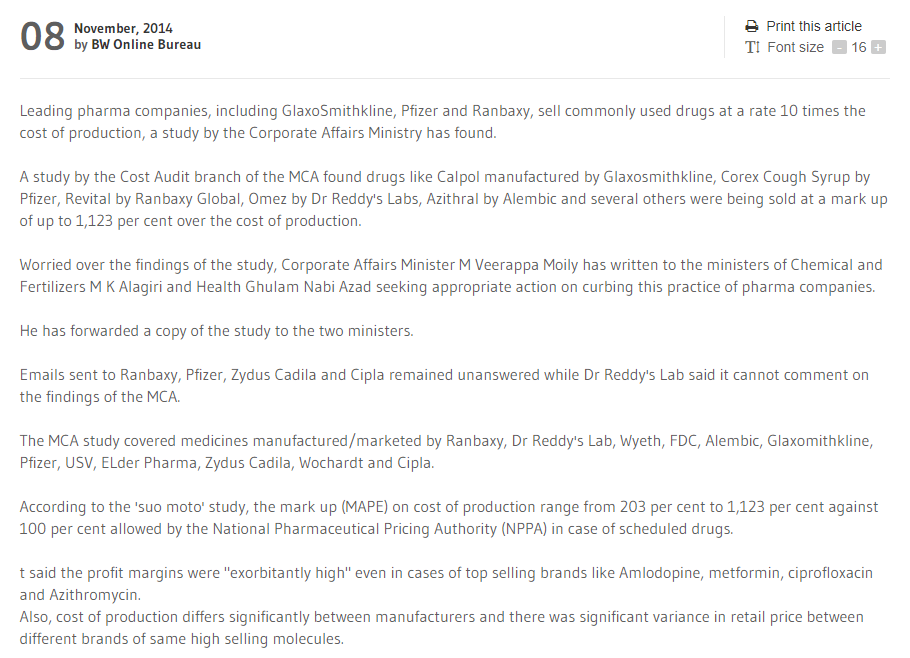

Below is an old news article that shows staggering price differences between Generic & Branded drugs

And here’s what happens when a company creates win-win situations for itself and it’s customers, by selling drugs at a fraction of the prices that branded drugs sell at. The company wins by increased sales and customers are happy to buy the same unbranded drugs at unbelievably low prices.

Branded drugs – A company develops a drug over several years, secures approvals from FDA or equivalent regulatory bodies, secures patents for it and then milks the cow. Medical patents typically last for 17-20 years after which other companies are legally allowed to manufacture the same drug using the same ingredients. Since the company manufacturing the generic drug, has not incurred R&D and related costs, it sells the drug at a fraction of the branded drug’s prices.

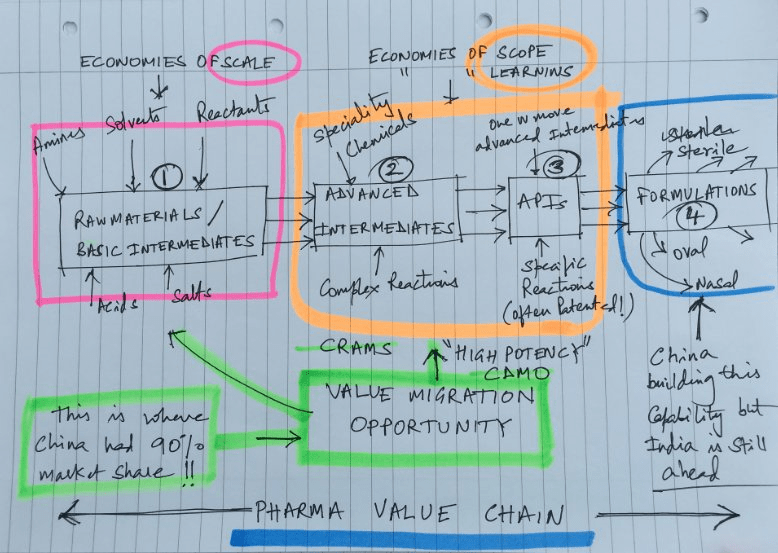

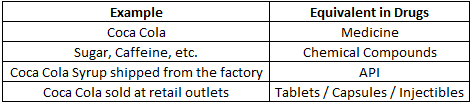

API Business

API (Active Pharmaceutical Ingredient) means the active ingredient which is contained in a drug. API and raw materials are often confused due to similar usage of the two terms. An API is not made by only one reaction from the raw materials but rather it becomes an API via several chemical compounds. In layman terms, Medicines are composed of APIs, and APIs, in turn, are composed of raw materials that go through various manufacturing processes before they turn into APIs. To give you an analogy, let’s take Coca Cola.

Peter Lynch once said “When there’s a war going on, don’t buy the companies that are doing the fighting; buy the companies that sell the bullets.” In the current context of war against the virus, one can equate APIs with bullets being used to fight the war against Coronavirus. Effectively, Alembic is fighting the war (through their Azithromycin drug) as well as supplying the bullets (APIs) to MNCs like Pfizer.

Icing on the cake – Azithromycin shortage in the USA & other countries

As per the US FDA website, there has been continuous shortage for Azithromycin all the way until 8th May, 2020 and the shortage continues as of the time of writing this blog. Only 3 companies out of 10, seem to be in a position, to supply the drug. And because, Alembic manufactures the API as well as the end product, it seems to be better placed to continue supplying the drug vs it’s competitors.

Alembic has the capacity to manufacture 10 Crore tablets a month. Retail price in the USA is between ₹120 & ₹174 per tablet. This price does not exclude retailer / distributor’s margins and how much of an upside this situation brings for Alembic, is hence open for debate. I believe there could be significant upside from this opportunity for the company, this year, and leave it to your judgement as to how much of an upside there is.

Capacity expansion

The company has been investing a good chunk into expanding their production capacity and this should take care of the next leg of growth for the company. The company’s balance sheet shows Capital work in progress has grown by 17x between 2016 & 2020. Sales has grown by 1.5x during the same period.

There is no denying that the company is capitalizing some of it’s R&D and related costs. On the other hand, the purpose of the above graph is to roughly understand what kind of an upside potential there could be. Before the company started expanding capacity in 2016, it used to have sales of ₹4 for every ₹ of Fixed assets and CWIP. Even if we were to assume, the company moves to ₹2.5 of sales for every ₹ of fixed assets and CWIP, coupled with increased assets in the future, from the current ₹1.4, the upside could be significant.

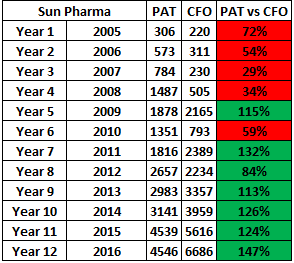

Earnings quality check

In FY2020, Alembic earned a return on equity of 26% after incurring high R&D expenses. While ROE can be used to measure a company’s efficiency, it is also my hunch (based on number crunching several fraud cases), that companies with 20%+ ROE in some industries are less likely to give us things to worry about vs the ones with lower ROEs. Barring exceptional cases, companies with ROEs above 20% and high cash flows are less likely to result in permanent loss of capital for minority shareholders. In most cases where there are corporate governance issues, you’ll either find low ROEs or low cash flows as compared to PAT. This is a shortcut that I use to filter companies quickly.

What are a few things that can kill this idea?

Exporter risk – Early in March 2020, the government of India, banned exports of APIs and some basic chemicals. If the situation changes, and exports are banned again, for reasons (unknown-unknowns) that we can’t anticipate, this would adversely impact the company.

Infection risk at plants – At least 2 other pharma companies have reported several of their employees got infected, recently, possibly at work.

Pricing power risk – The company may not end up being able to pass on the increase in API costs or other raw materials to it’s customers. We will need to wait and see how this plays out over the next few quarters. This risk also applies to their generics business. Other generics players producing the same drugs may result in margin erosion for the company.

For example, data from an article from the US FDA site states, higher the number of generic players, lower the drug prices.

So if the branded drug sells at ₹100 and there is just 1 generics player, then the generic drug would sell at ₹61. However, if there are 6 Generics players, then the generic drug gets sold at an abysmal 5 bucks.

Other risks include Macro risks due to uncertainty around Covid19, Opportunity cost risk, Logistics / Raw material risks & Dilution / Leverage risk (The company has been growing faster than the ROE it delivers)

Valuation

Why investors are likely to pay top dollar for pharma companies in the near future?

- The markets hate uncertainty and given the current uncertainty around earnings prospects of most companies, one sector that is recession proof is Pharma. This is because, no matter how the Covid situation impacts the economy or no matter how long it takes scientists to develop a vaccine, patients are not going to reduce consuming medicines. For example, I looked up sales numbers for pharma companies between 2008 & 2010 and a majority of pharma companies’ sales went up, although every other sector was hit by a recession. I believe it is reasonable to assume that pharma companies (and other sectors with good earnings visibility) will see better valuations in the near future, compared to sectors which have low or no earnings visibility, such as Oil, NBFCs, Real Estate or Auto, etc. Moreover, if lockdowns are extended or reintroduced, Pharma companies are less likely to have a production impact since they serve an essential human need which cannot be deferred to a future date. Unlike most other industries, there is no concept of pent up demand in the essential drugs business and patients cannot postpone consuming drugs to a later date.

- Scarcity of high growth companies in the current environment is likely to drive up valuations for the ones that promise growth in tough times. Some investors may perceive 17-18 PE as expensive but I disagree with that notion, and believe we should buy growth and not PE. For example, in 2009, Page Industries’ stock was selling at 17-18 PE at some point and some people considered it expensive and fell into the statistical cheapness trap. They ignored the fact that Page had grown revenues at 45% CAGR between 1996 & 2009 and PAT had grown at 68% CAGR between 2005 & 2009. We all know the outstanding returns it subsequently delivered for the ones who looked at growth instead of PE.

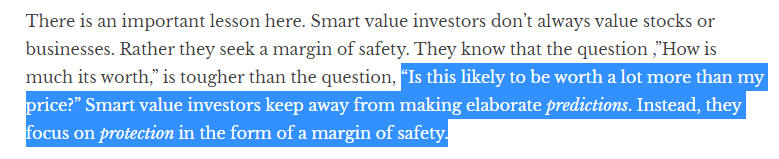

- In his wonderful blog on VST industries, Prof. Bakshi mentioned this

I believe, at my buying price, this would apply to Alembic too. At 17-18x TTM reported earnings, for a company with high R&D exp and one that’s rapidly growing, the downside looks limited, whereas there is option value embedded in the stock in the form of an upside from the Azithromycin opportunity as well as the other approvals that the company hasn’t monetized yet. In other words, I may be wrong on how much upside there is from the Azithromycin situation, but I don’t think I have paid too much for the growth I anticipate from it. My average buying price is a little less than 700 bucks, which is marginally higher than, what the market was pricing this company’s stock before the Azithromycin opportunity knocked the company’s doors.

If the Azithromycin situation plays out as I expect, then it’ll result in a significant growth in earnings for the company.

If it doesn’t play out, then there is a high chance the company might still continue to grow well, as it has demonstrated over the last few years.

- Besides, economic earnings are higher than reported earnings because the company spends a fortune on R&D. A high R&D expense shows that the management is willing to forego immediate benefits, in order to ensure future growth and has the deferred gratification gene. The management team mentioned they are looking at 700+ Crores R&D Exp in FY2021, on their latest concall & this increased R&D Exp is in a year where most other sectors are announcing layoffs, cost cutting measures, etc.

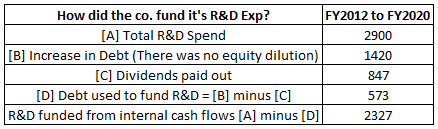

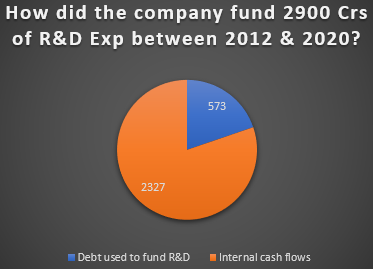

How did the company fund it’s massive R&D program?

The company spent a total of 2900 Crs on R&D between 2012 & 2020.

In the same period, their debt increased by 1420 Crs.

Out of this 1420 Crs, 847 Crs were paid out to shareholders as Dividends.

So these guys went to the bank, borrowed 1420 Crs from the bank and out of this 1420 Cr loan that they took, they passed on 850 Crs to Shareholders as dividends.

So that left them with 573 Crs which they could now use to fund some portion of their R&D.

So, this means the company funded 2300 Crs or 80% of it’s R&D exp from cash flows that the business generated and 573 Crs or JUST 20% of R&D from debt.

Was it funded by diluting equity? No, because no new shares were issued.

So that leaves us with the only other source of funding which is Cash Flow from Operations.

So 80% of their R&D exp was generated by cash that the business generated.

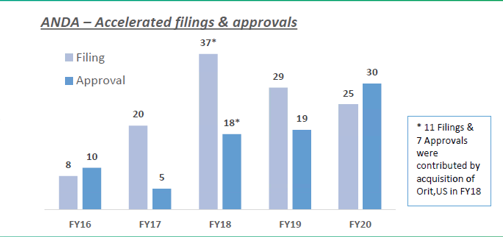

The outcome of all this R&D expenditure can be seen in the new approvals that the company receives from the US FDA.

Some folks I spoke to, raised concerns about high R&D expenses (investments?) by the company. Lets think about what happens when, a company has a lot of approvals.

By securing more approvals with potentially huge payoffs, the company gets more exposed to positive black swans. A case in point would be Alembic’s opportunistic plays at 3 different times. Alembic,

- benefited from the opportunity in Abilify drug back in 2016 or thereabouts

- is benefiting from the ongoing opportunity in Sartans drugs in 2018 (expected to last until Dec 2020 or beyond)

- has the potential to benefit from the ongoing opportunity in Azithromycin in 2020

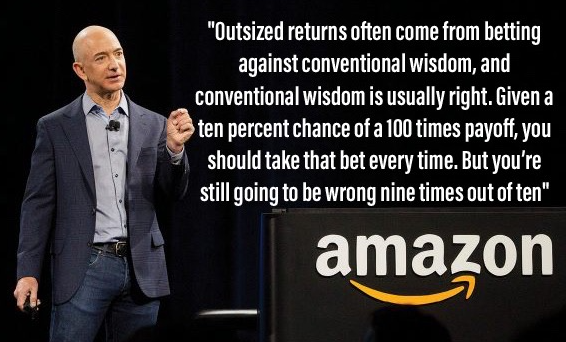

Was it a case that company got lucky thrice or was it because the company had so many approved products / approvals in place, which ensured they were (almost) exclusive sellers of 3 products that were in solid demand? Were they thinking “Heads I win big, tails I don’t lose much”?

In my view, Alembic seems to be taking the approach outlined by Jeff Bezos – Given a 10% chance of a 100 times payoff, you should take that bet every time.

Here’s what somebody somebody wrote about ANDA filings elsewhere. And this is one hell of a way, to think about the big number of ANDA filings this company has, in comparison to other companies of similar sizes.

I personally think of filing ANDAs as Making Dices which the pharma company gets to roll once. If you roll and you get “6”, you get a windfall. If you roll the dice and get “4” or “5”, you get a reasonable amount. If you roll the dice and get “1” or “2” or “3”, you get nothing. The more dices you manufacture, the more number of times which you can possibly roll. There is a role of luck, but for that to happen you have to have a dice in your hand. And possibly as many dices as you can. Abilify was one of the dices which alembic rolled and luckily got a “6”. With the money from this, Alembic is now manufacturing many more dices . We don’t know which dice in future would be a jackpot, but what we know is that Alembic is surely producing many more dices to roll in future.

From the book – 100 to 1 in the Stock Market by Thomas Phelps

Imagine Nifty was a single company. Which of the following companies is likely to have better prospects?

Here’s a good way to think about High R&D expenses. From Prof. Bakshi’s Relaxo lecture.

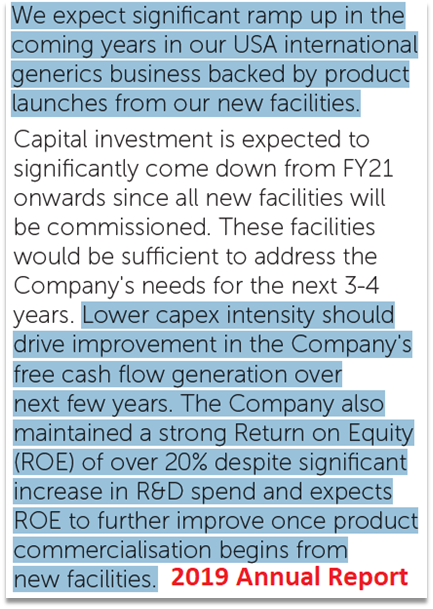

As stated earlier, Alembic earned a return on equity of 26% after incurring high R&D expenses in FY20. And here are the managements’ thoughts on R&D exp, ROE and Free Cash Flows in the next few years.

Addendum – Writing about some questions I was seeking answers to – 26th May, 2020

Why are margins high?

The company’s FY19 annual report states – “A good supply chain helps protect margins and also provides us with some room to improve our pricing.” I believe the reasons for higher margins could be the company’s supply chain + their US front-end marketing team + some pricing power due to the Sartans issue.

With this I conclude my investment thesis on the company.

Disclosure – I and my clients have substantial positions in this company and my views are certainly biased. This blog is not to be construed as an investment advice. Please consult your investment advisor before investing.

Disclaimer: This is NOT investment buy/sell/hold advise. I am not SEBI registered. May change stance on above business anytime with new developments and/or new insights, and/or overall market conditions. May NOT be able to update periodically. Please do your own diligence and/or take professional advise, before investing.

-Barath Mukhi

13th May 2020