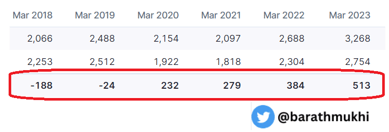

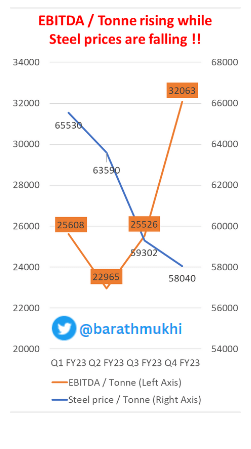

I tweeted this on Usha Martin today and thought might be a good idea to post it here as well.

After 14 years, in Dec 2022, the steel company’s stock finally crossed it’s previous all time high of 147 it had hit in 2008, along with unusually high volumes.

Let’s roll back a bit. In 2018, things weren’t looking rosy for Usha Martin. They had made a loss for 4 consecutive years.

So what happened? In 2018, one of the company’s promoter and currently Usha Martin’s Managing Director, Mr. Rajeev Jhawar, had several disagreements with the board of directors. Eventually, he successfully persuaded them to sell off their steel business.

In 2019, Usha Martin sold off their steel business to the Tatas.

Hang on.

A steel co. sold off their steel business 4 yrs back and their operating profits have been growing steadily.

How did that happen? Something isn’t adding up.

The answer lies in Usha Martin’s Steel Wire Ropes business.

I know. I know. I hate jargons too.

Let me tell you more about what Steel Wire Ropes are.

Steel wire ropes are like really strong and tough ropes made of many small metal wires twisted together. They are used in things like elevators, cranes, and bridges to help lift and hold heavy things safely.

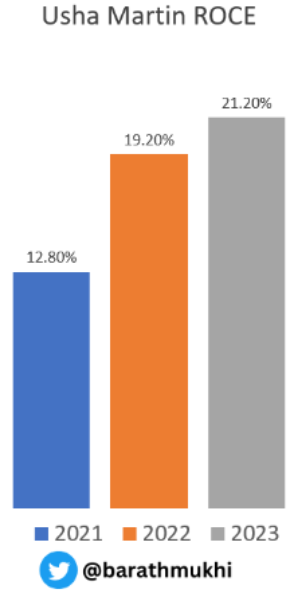

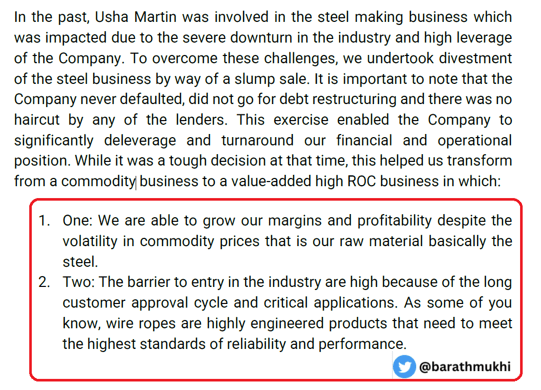

The first thing that comes to one’s mind is Steel Wire Ropes are another commodity business and are likely to suffer due to the ups and downs in Steel cycles. But then one needs to look beneath the surface. Mgmt recently clarified that they are doing 2 things to improve ROCE.

One, after selling off their steel business in 2018-19, they decided to focus on more Value added products. What happens in value added Wire Ropes is that the % of steel in the price of the end product, goes down, leading to better return ratios.

Second, they decided to focus more on their international Wire Ropes business, because the margins are much better there.

Ok so how do we know they have been able to maintain margins in spite of highly volatile steel prices. If you compare their EBITDA per tonne figures with steel prices, you’ll notice that the management’s claims are aligning well with the actual results.

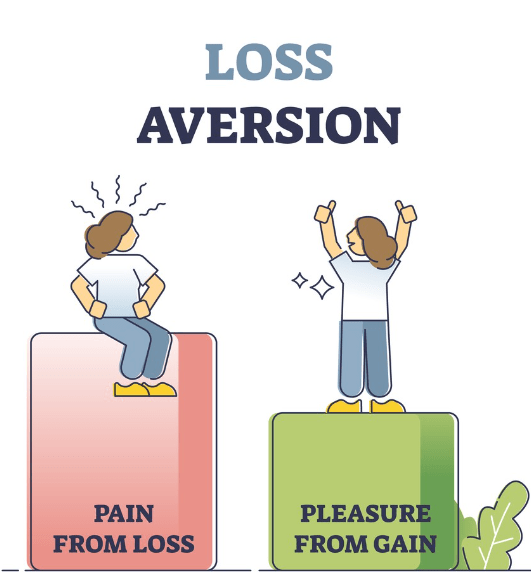

Ok. So what about entry barriers and margin sustainability? As per Mgmt, Steel Wire Ropes have high entry barriers because of long customer approval cycles and critical applications.

Here comes, Loss Aversion, an important mental model in psychology. Imagine I am an employee at an Elevator manufacturer buying ropes from Usha Martin and the cost of an Elevator Rope is a fraction of the overall Elevator cost and I decide to switch vendors.

If my employer, the elevator co. saves some money by switching vendors, then I get some applause.

However, if the new vendor’s quality is a little less than Usha Martin’s and the rope snaps, what happens to my job and my reputation?

Most humans would rather not switch.

Ok. That kind of explains entry barriers.

What about future growth and margins, because the market is a future discounting machine?

Valuation – The stock trades at 20 times earnings. If the same growth trajectory continues and return ratios further improve, will the stock get re-rated? We don’t know the answer to that because Mr. Market is gonna decide that.

And when these new businesses come in, there are huge advantages for the early birds. And when you’re an early bird, there’s a model that I call “surfing” – when a surfer gets up and catches the wave and just stays there, he can go a long, long time. But if he gets off the wave, he becomes mired in shallows. But people get long runs when they’re right on the edge of the wave, whether it’s Microsoft or Intel or all kinds of people.

Charlie Munger

Today I am gonna be writing about a specialty chemicals company that has shown a compounded growth rate of 60% in one of it’s verticals. The growth of this vertical is being driven by demand from lithium ion batteries, which are critical to the continuation of this EV wave.

We’ll take Tesla’s sales, currently the biggest and the most undisputed successful electric vehicle company in the world, as a proxy for what’s happening in the EV industry. Here’s how they’ve grown over the last decade plus.

The electric vehicle wave is here to stay. Here’s a chart that shows the kind of explosive growth EVs have been seeing, worldwide. And we are just getting started in EVs. EVs were just 8% of total cars sold in 2021. Can this number become 50% over the next decade? Nobody knows!!

Demand for EVs in turn is leading to demand for Lithium Ion batteries.

“What about the next 10 years? I’ll be surprised if it’s not over 100 million in 10 years.”

Elon Musk about the future volumes of Tesla – Aug 2022

In 2022, Tesla is likely to produce 2 million cars. And Musk thinks they’ll be able to produce 50x that number of cars in 10 years.

50x in the next 10 yrs!! To grow 50x in 10 yrs, Tesla will need to grow at 50% per annum, every year for the next decade. To put things into perspective, the total number of cars (ICEs + EVs) registered in the US in 2021 was 290 million (This includes old as well as new cars). And the EV market leader there, is selling a miniscule 2 million cars this year. Wow!!

And here’s what he recently said about Lithium batteries!!

The Indian business we are interested in, is Gujarat Fluorochemicals, a 37 thousand Crs Market Cap co. that I expect, could surf the EV wave neatly, over the next few years, or at least it looks so, at the moment. So GFL makes stuff that goes into Lithium Ion batteries.

Let me start with a notice that GFL gave to it’s customers in April 2021.

Basically they were saying:

There was high demand for PVDF & FKM and will continue to remain so.

R142b was in acute shortage, globally!!

What exactly are FKM, PVDF & R142b? What does this stuff have to do with the EV wave? I’ll come to that in a minute.

First, here’s an overview of GFL’s backward integration, which it has painfully developed over many many years.

Let me start with a story.

So back in 1987, countries basically came together and decided to gradually phase out CFCs that were killing the ozone layer. R22, which GFL also makes, is one of the gases that was phased out. R22 can still be made by cos and used as a raw material for other stuff.

If a competitor needs to make PVDF and FKM, they’ll need R22, R142b (which again is in high demand worldwide, without enough supplies).

So what is PVDF? And where does it fit in the EV battery chain?

PVDF is a fluoropolymer that is used in stuff that requires the highest purity, as well as resistance to solvents, acids and hydrocarbons. Below is an image which describes the stuff that goes into batteries.

Source – Arkema, another PVDF maker from France

More on PVDF Binders and Coatings from Solvay, another global player that is into fluoropolymers.

Moving on to FKM. What exactly is it?

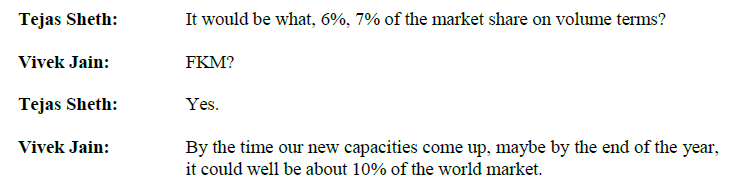

Why is FKM, another fluoropolymer, in demand? And what kind of market share does GFL have in this product? The answers are in their July 2022 concall.

And they will have at least 10% worldwide market share in FKM.

Okay so what’s the big deal in having a 10% market share? Can’t another set of players just come in and make more FKM and other stuff that GFL makes?

Dated Feb 2022 – Got this from Google so can’t really verify the authenticity here.

Here’s one more from another site, which says building chemical plants will take longer than building semiconductor plants. Semiconductors are another industry where FKM is used. This comes from an executive from Daikin which is a major fluoropolymer manufacturer.

What stops a potential new entrant from coming in with new capacities here?

Besides, GFL started out as a commodity Fluoropolymer player and over a course of time created a large no. of Fluoropolymer grades specific to their customer. This leads to a lot of customer stickiness and makes life difficult for a potential new entrant.

One of the raw materials that is not available for producing FKM, PVDF and other fluoropolymers is R142b, a refrigerant gas that not many cos on the planet are allowed to manufacture. New approvals for these gases take a long long time because of the ozone depleting potential of these gases.

And here’s a co. that will not only use R142b for captive consumption but also export it. Talk about having your cake and eating it too.

Essentially these facts mean fluoropolymer cos worldwide are:

In huge demand, thanks to rising consumption of Lithium Ion batteries.

There are not enough capacities that can meet this demand.

Players that make both, the raw materials as well as the end product, are at a huge advantage, compared to the others.

It takes many years, lot of effort, approvals and expertise to add capacities.

This puts players like GFL in a sweet spot. Btw GFL is the only company in India to make and export some of the products I have written about and other spec chem players in India are likely to take a while before they can catch up.

One of the things I’ve learnt as an investor is that we should view businesses as stories that are unfolding and not as pictures of still water. A lot of these growing businesses spring up happy surprises when you least expect them to. I am sure very few investors or perhaps nobody, a few years ago, would have imagined PVDF would become such a big business for GFL.

Yet, here’s how the movie unfolded. Starting with PTFE suspension, they gradually moved to PTFE Emulsion, FKM, PFA, FEP, Additives and eventually to PVDF.

Source – 2020 Annual Report

And here’s how the management is expecting their Specialty Chemicals business to play out. Specialty Chemicals which is a 300 Crs business in June 2022 could potentially transform into a 2000+ Crs business over the next few years, thanks to battery chemicals such as LiPF6 that they are planning to make in the near future.

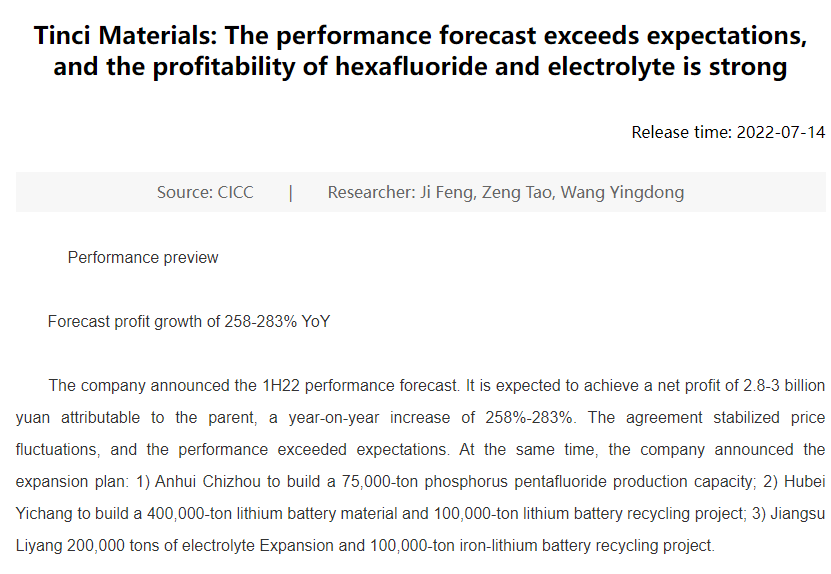

Here’s a Chinese player, Guangzhou Tinci Materials, which makes LiPF6 and below we can see the kind of supernormal growth they are seeing in their business.

Source – Investing.com

And Tinci’s business in no mood to slow down. Here’s a recent news article which shows the kind of exponential growth they are seeing. The article also states they are expanding capacities.

Source – Tinci Materials Investors’ page

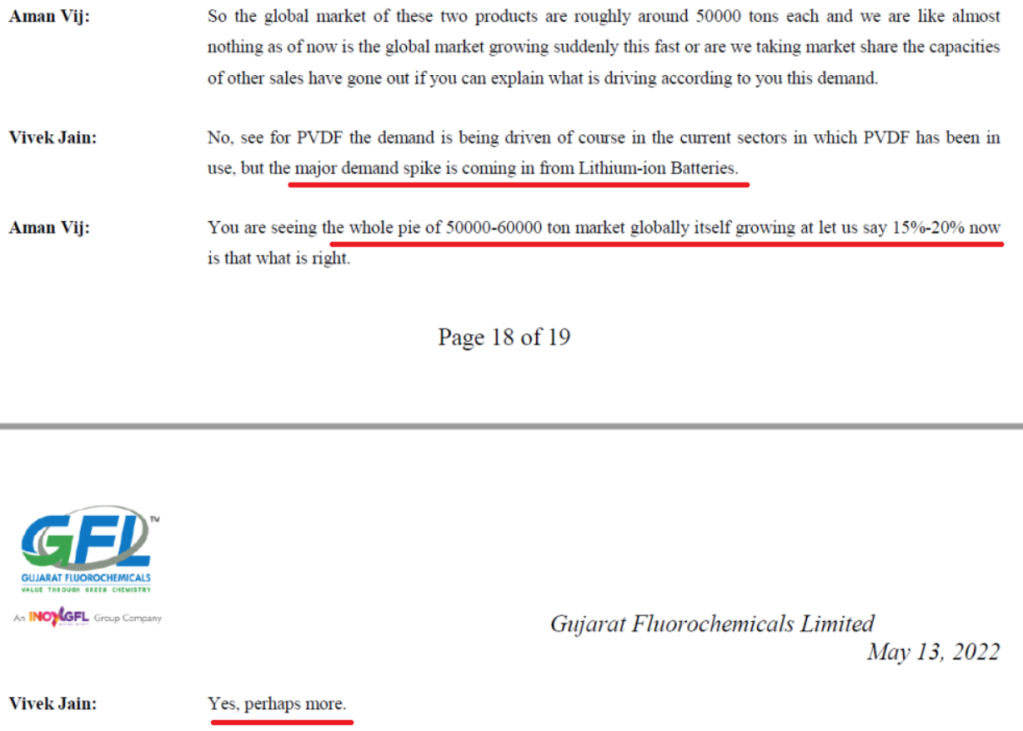

The fact that the lithium ion battery market is growing at more than 20% was also confirmed by GFL’s management in their May 2022 concall.

The future will tell whether or not GFL can execute their LiPF6 business the way they have done for PVDF & FKM. If LiPF6 works out well, that’ll be an icing on the cake.

New Fluoropolymers, which consist of PVDF & FKM are just 18% of their TTM sales. I foresee this division becoming a larger chunk of the overall pie in the near to medium term. Specialty Chemicals which would consist of LiPF6 in the future, is 7% of TTM sales and that could become a big one as well.

Risks

Corporate guarantees worth 1000 Crs+ given to Inox Wind – Inox Wind is another entity from the same promoter group. This one has been a bee in the bonnet for GFL’s stock for quite sometime. Promoters have committed to return this money to GFL by March 2023. Any other hanky panky in this area would be a show spoiler.

Disruption risk – If EVs start adopting other technologies owing to supply chain issues in PVDF / FKM and other fluoropolymers, this would lead to GFL’s business getting hurt. As of today, I haven’t been able to find any evidence to support this argument. But then technologies & supply chains can evolve rapidly given there is enough moolah involved, and one can never say for sure.

Fire hazards – Last year there was a fire at one of the GFL’s plants and that led to a shut down of that plant for sometime. Although it was covered by insurance, something similar happening again could spook investors.

Environmental hazards / gas leaks in the future.

LiPF6 business not kicking off as expected.

Other unpredictable risks – Risk is what is left over after we’ve thought about everything else.

More availability leads to more consumption

Charlie Munger once said “You’ll drink a hell of a lot more Coke if it’s always available.”

Charlie was implying the power of Coca Cola’s worldwide distribution network. Just because Coke is available everywhere, we tend to consume more of it. Imagine someone keeping a new Coke bottle at your and all your colleagues’ desks every day. Without doubt, it will lead to more sales for Coke, no matter how health conscious you or some of your colleagues are.

Here’s one more from one of my favorite self-help books.

“Environment is the invisible hand that shapes human behavior. Despite our unique personalities, certain behaviors tend to arise again and again under certain environmental conditions. In church, people tend to talk in whispers. On a dark street, people act wary and guarded. In this way, the most common form of change is not internal, but external: we are changed by the world around us.”

Atomic Habits

It’s easy not to read a book when the bookshelf is in the corner of the guest room. It’s easy not to take your vitamins when they are out of sight in the pantry. When the cues that spark a habit are subtle or hidden, they are easy to ignore. If you want to remember to take your medication each night, put your pill bottle directly next to the faucet on the bathroom counter. If you want to practice guitar more frequently, place your guitar stand in the middle of the living room. If you want to remember to send more thank-you notes, keep a stack of stationery on your desk. If you want to drink more water, fill up a few water bottles each morning and place them in common locations around the house.

Atomic Habits

Will something similar happen with EV adoption? What will happen when charging stations become available at more and more parking lots, malls, restaurants, offices and apartment car parks? Chances are high that if the external environment makes more charging stations available, it will lead to faster adoption of EVs.

And your guess is as good as mine on what kind of an impact this will have on the financials of EV beneficiary companies such as GFL.

Disclosure – I have a position in this company and my views are certainly biased. This blog is not to be construed as an investment advice. Please consult your investment advisor before investing.

Disclaimer: This is NOT investment buy/sell/hold advise. I am not SEBI registered. May change stance on above business anytime with new developments and/or new insights, and/or overall market conditions. May NOT be able to update periodically. Please do your own diligence and/or take professional advise, before investing.

Barath Mukhi 12-August-2022

Correction – May 2023

Only recently I realized, the making of PVDF does not require R22. This was pointed out to me by a friend. The other thing about making R22 is not restricted for feedstock use.

Essentially this means, there are not as many restrictions on the supply side as I had expected. I continue to stay invested and bullish on the company. As stated earlier, I may change stance on above business anytime with new developments and/or new insights, and/or overall market conditions. May NOT be able to update periodically. Please do your own diligence and/or take professional advise, before investing.

Imagine your equity advisor told you to buy this pharmaceutical company’s stock in year 6. Considering that their cash flows aren’t reflecting the profits that are being declared by the company, would you still buy? (A consistent cash flow of below 8 bucks for every 10 bucks (80%) is generally considered not good)

And then you find out that cash flows are low because their receivable and inventory days have gone up 5x. Would you still consider buying, that too in the middle of a small/mid cap bear phase?

You decide to give the stock a miss, because the company’s working capital and cash flows aren’t looking good.

Much to your disappointment, the stock goes on to become a 6 bagger over the next 5 years, compounding shareholder wealth at a stunning 42% CAGR. What could you have potentially missed?

In my workshops I am often asked for a formula or an excel sheet that can help people spot life changing stocks. A related question that comes up rather frequently is how important is it to compare cash flow from operations vs profit after tax. And I am going to be deep diving into that aspect.

Note: This isn’t to pin point faults in any investor’s analysis. All of us are learning, and making mistakes is the tuition fee we pay to the market. And these case studies are vicarious experiences for normal mortals like all of us.

Case study 2 – Opto Circuits

In 2012, an investor wrote a blog about a very interesting fast grower called Opto Circuits. Here’s how Opto had been doing until then.

At 6 times earnings. This was a GARP investor’s dream come true. A 50% grower available at just 6 P/E.

Why was it trading at such low multiples? Perhaps it was because small & mid caps were in a bear phase or perhaps the market had doubts about the company’s cash flows or maybe it was a gold nugget waiting to be discovered.

In his blog post, this investor also mentioned Opto’s cash flows were worrying.

Yet, this risk was not given enough weight and this investor and many others who invested around that time, lost a big chunk because the market was right about the company’s shady accounting/business practices.

Investors who made a second mistake by not cutting their losses and stayed invested in Opto subsequently lost 98% of their capital.

The author subsequently accepted that his investment thesis had been broken at the hip, by writing another post mortem blog in which he reflected upon what had gone wrong. (To this person’s credit, not every blogger is bold/conscientious enough to do this. Unlike this blogger, some others just try to push things under the rug.)

Case 3 – Photoquip India

In another article published in a financial magazine, another investor talked about his experience with Photoquip India, which he picked up in 2011. Since this is a paid article, I don’t want to quote anything written in it. But the gist of the story is he trusted the management at face value, did a lot of scuttlebutt on the company/sector and yet ignored the fact that cash flows were lacking before, during and after he’d invested.

Now this was not some rookie investor. Instead he was the CIO of a PMS firm and somebody who’s experienced in many equity markets such as India, Sri Lanka, Bangladesh, Kenya, US, UK, Canada, Australia, and New Zealand.

And here’s the subsequent downfall in the company’s stock price. Even after a rare & phenomenal bull market like that of 2020-21, the stock is still down 70% after a decade.

So we have contrasting cases here. In case 1, the stock performed well despite low cash flows and in the cases of Opto & Photoquip, cash flow was the straw that broke the camel’s back.

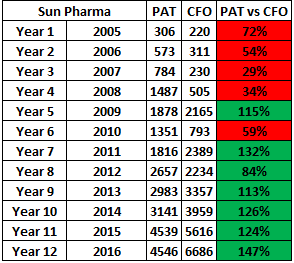

Case 1 is that of Sun Pharma between 2005 (Year 1) & 2015 (Year 11).

In all 3 cases, cash flows were low and yet, the market was lenient towards Sun. So how were Sun’s lower CFO numbers different from Opto Circuits’ and Photoquip’s?

The answer lies in the following piece of wisdom from Albert Einstein.

In the case of Sun, a fanatic promoter drove cash flows back to high levels, from year 7 and Mr. Market said I am gonna be patient with this promoter for 6 years and I am not gonna count too much.

With Sun Pharma, the market believed in the promoter’s ability to eventually turn things around whereas Opto Circuits and Photoquip were cases of outright fraud. Mr. Market was perhaps smart enough to discount the fact that Opto & Photoquip would never grow their cash flows to sustainable levels.

The point I am trying to make is that one needs to look at the holistic picture, the grand scheme of things going on at a company. Perhaps we should not forego investing in companies if a single metric is out of whack, if other factors such as scuttlebutt feedback, management track record, competitive advantages available to the company are impeccable. Focusing too much on any single metric is the functional equivalent of paying too much attention to the scoreboard and not focusing enough on the playing field.

Yet, there are times, a single metric such as low cash flows become deal breakers, if other red flags start showing up. Perhaps some of these red flags would become obvious only after resulting in permanent losses of capital. As we can see, long term investing in equities will never boil down to a single formula, ever.

Case 4 – Laurus Labs in July 2020 Some investors were worried about Laurus’ receivables being high and chose to skip investing in its stock, at a time when it was available at one-fifth of it’s current price. In effect they were saying, Laurus’ future CFO would be impacted because cash would be stuck in receivables and some of those receivables would become bad debts and would therefore lead to cash flow problems for the co.

What they missed is that receivables in pharma usually don’t end up being bad debts and write offs because relationships between pharma cos and their clients are multi year and there is a lot of inter dependence. If one of Laurus’ large clients defaulted or delayed payments, Laurus could simply cut-off future supplies to that party and start recovery.

Besides who were these clients that owed money to Laurus? Were they some fly by night operators that would vanish into thin air some day? Or were these clients big MNCs that could potentially delay but not deny payments to Laurus? In my view, the answer was the latter and hence I took a big position despite their receivables being high, at 102 days at the time.

To conclude, like any other metric, a low CFO vs PAT can tell you there could be something getting cooked in the books. Yet, as the case of Sun Pharma shows, if the jockey is good, he can turn things around and a low CFO doesn’t become a problem then.

Too many times, we get stuck up on a single metric, and let go of some great opportunities, without looking at the grand scheme of things instead. If this isn’t analysis paralysis, what is?

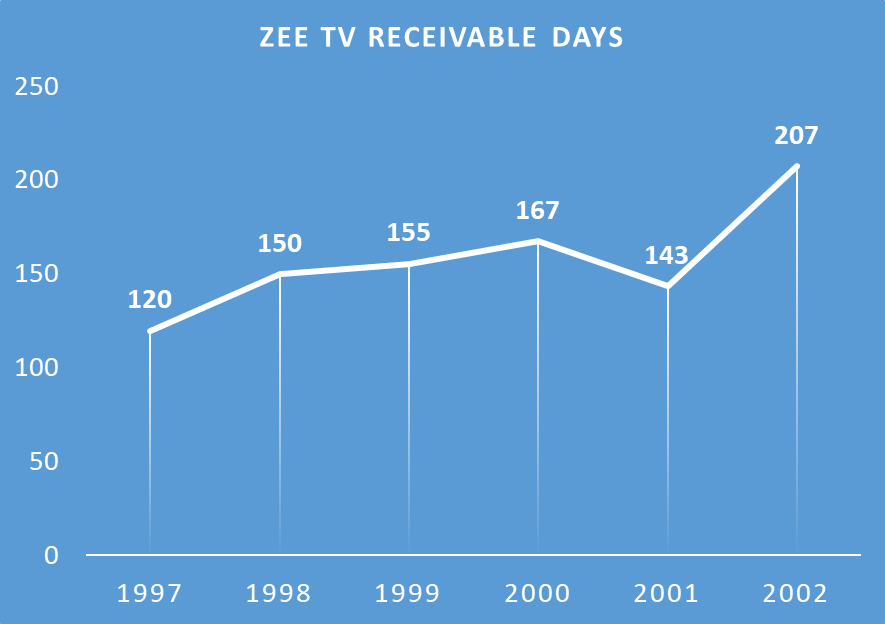

Addendum – Case 5 – Zee TV during the TMT / Dotcom bubble phase

I was reading India’s Money Monarchs and this response by Mr. Samir Arora caught my attention, this morning (23rd Jan 2021).

“If you look at our history, both the reason for success and the reason for criticism are the same, “You hold your stocks too long.” Zee, multiplied 160 times since we bought it. Every Rs 10 invested in the company had multiplied to Rs 1600. But we did not multiply our investment to that extent because by the time we sold, it had already fallen to Rs 700. So, we basically ended up multiplying our investment 70 times. I remember having said in an interview with one of the business magazines that our year-end target for Zee was Rs 250 when the price was around Rs 100. However, the stock had multiplied 10 times by the time the year had ended and we did not sell during the year. Even if I had sold at Rs 300, I would have tripled my money in a year and that would have been considered as a great job. While some might say that not selling at Rs 300 was a good decision, others might criticize me for not selling at Rs 1600.”

And then I looked at the numbers for Zee TV during those years and what I saw blew my mind.

Zee had a net cash flow of below zero while the TMT bull run was in progress. And the reason it’s insanely high receivable days. Zee was taking an average of 6 months to recover due owed to it by its customers.

Yet the market wasn’t worried because Zee went on to become a 100 bagger. Now I doubt how many people would have actually made 100x their money but we can at least get a rough idea of how things went.

Maybe the market was inefficient, back then. Or perhaps, it had a good enough reason because Zee’s profits had been growing at a very fast clip.

So yet again, we have a case where the market prioritized growth over balance sheet quality and cash flows and hence it makes sense to keep an open mind about all these metrics.

Disclaimer – Not SEBI registered. Not a recommendation to buy/sell any of the above mentioned stocks. Don’t hold any of the above either.

There’s this German company that makes a key component for automotive, aerospace, and industrial uses. The company initiated a restructuring program in Sep 2020. Due to rising costs, management wanted to reduce headcount & manufacturing capacity in Germany.

Here’s the press release from the company in Sep 2020.

Now, if we were to read between the lines, a big chunk of these jobs and production capacities would be moved elsewhere.

How do we know where these jobs are moving to? One, by reading between the lines and two with some data. First, let’s see what the management of the Indian listed entity of the same group, is saying.

So the Indian co. is saying, they will grow their exports but cannot reveal, at what rate. My guess is they either don’t have a go ahead from the parent due to geo-political reasons or perhaps it is an evolving situation and they don’t know themselves, what their German bosses have in mind.

Now let’s move to the data. A rising export trend, indicates that management is walking the talk and business is indeed moving to India and could be an indicator of things to come.

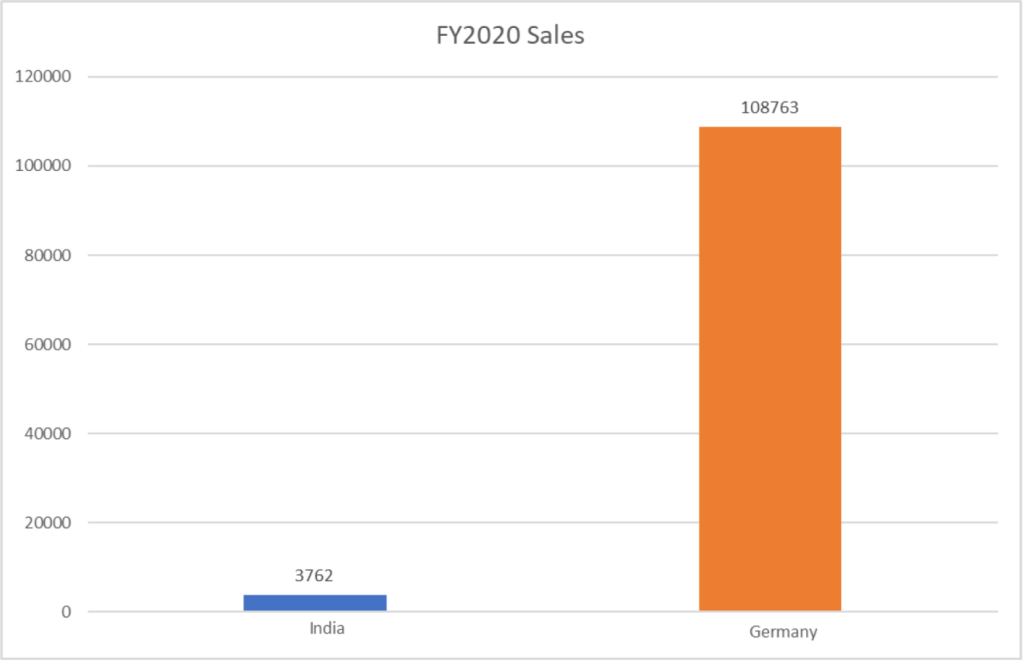

Now let’s look at, what sales look like for the German parent and for the Indian entity.

The German group’s worldwide sales are 29 times that of the Indian entity’s 3762 Crs, last year and that means there is a lot of room for growth here and scalability is not likely to be an issue.

Now, this is not a company that is struggling to sell its products. It is a company which is trying to cut costs and move jobs to lower cost locations such as our very own. In fact, it is an seven decade old company which holds a significant global market share in the segment in which it operates.

Risks

Plants are operating at full capacity and future growth relies on Capex. Current fixed assets = 1000 Crs. Capex for next 3 years = 1200 Crs.

German politicians are already doing everything they can to retain jobs within their geographies. As of today, cost economics are winning over politics and business is moving to India. This may or may not turn out to be the case, in the future.

Margins drop due to fluctuation in raw material prices. Although margins have stayed relatively stable for the company in the past, there is no guarantee that they will be able to pass on commodity price risks over to their customers in the future and remains a key risk for investors.

At the time of this writing, the business trades at 50 times earnings. For a business where things can change quickly, does it make sense to value the business based on a P/E multiple?

I’ll leave you with that thought.

Disclaimer: Invested in the Indian co. from lower levels. These are my views and are not to be construed as investment advice. As always, please do your own research before proceeding to buy/sell/hold.

Let me just start by saying that my views are positively biased because I have stayed invested in this company since much lower levels.

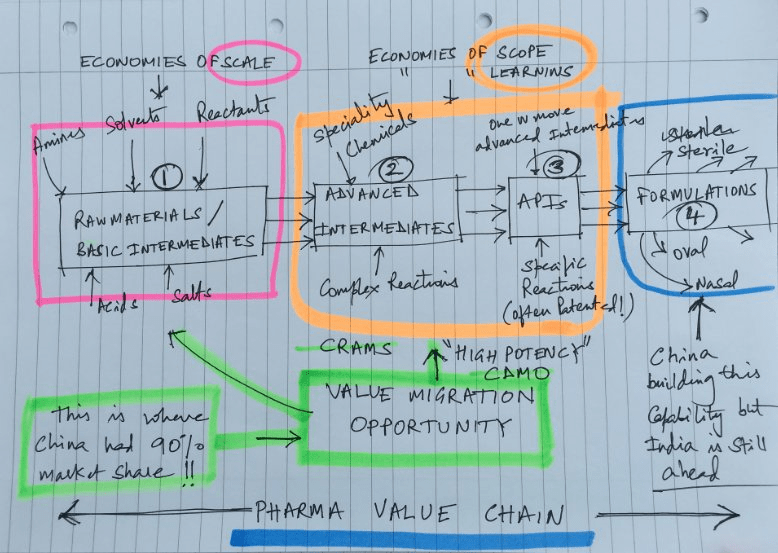

This post is an attempt to articulate what I have learnt so far, about Indian Pharma.

We have all read recent news reports about the Chinese government cutting power to polluting factories in certain areas. These power supply cuts mean that the factories operating out of such provinces will have lesser capacity to produce goods and operate at a much lesser scale.

This change could mean that if Chinese manufacturers are unable to produce as much chemicals or APIs (active pharmaceutical ingredient) or Key Starting Materials, as before, there would be a shortage of these products across countries. This could possibly lead to higher prices of these products for whoever is able to make them and thereby result in increasing sales and margins. These manufacturers could be from China, India, Timbaktu or anywhere else.

In our case, it could either be beneficial or not, depending upon which side of disruption, the companies that we are invested in, are on.

What are Key Starting Materials (KSM)?

The textbook definition of KSMs – Critical input used in the manufacturing of an essential generic medicine, as well as ingredients or components that possess unique attributes essential in assessing the safety and effectiveness of such essential generic medicines, including excipients and inactive ingredients.

From Mr. Sajal Kapoor’s Twitter handle

From what I have understood so far, KSMs include stuff like Amines, Solvents, Reactants, Acids & Salts. Maybe there are things beyond this too.

With this background, let’s define the problem now. Raw material supplies for Pharmaceutical companies are likely to get hit and these shortages will lead to spikes in input costs.

Question – Who will be impacted negatively and who will be impacted positively, by this change?

There are certain products where Indian API manufacturers are completely dependent on China for APIs and KSMs. For instance, fermentation-based products like anti biotics, statins, vitamins etc. These players may see cost escalations in input costs of fermentation based products and some of them will pass it on to their end customers over time. Conversely, Pharma players without pricing power won’t be able to pass on these increased costs and their margins will get negatively impacted.

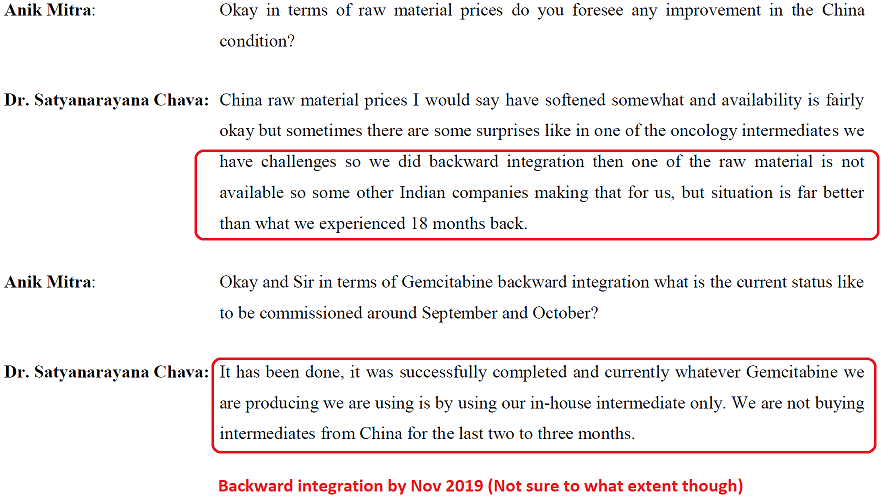

Since I am interested in Laurus Labs, I was worried about this angle and decided to deep dive.

What will happen if Laurus Labs is not able to pass on these price increases to their customers?

Here’s what I found.

This China problem is not new. It keeps cropping up every once in a while. They had a similar issue in 2019 as well.

And here’s how they handled it.

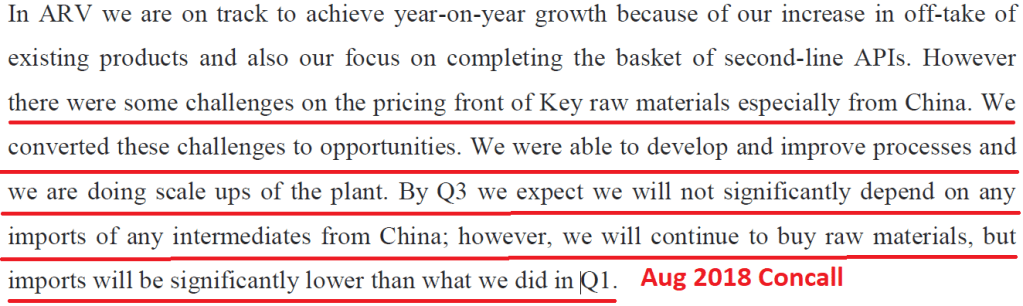

Let’s go back another year now. The year is 2018 and they were having the same troubles. Prices of key raw materials had gone up and Laurus was able to convert a challenge into an opportunity.

Based on the above events, one gets a gut feel that even if there are challenges in the supply chain, here’s a team that can do things, to resolve the issue.

Now let’s look at the situation from the vantage points of various stakeholders involved.

The Chinese factory owner: Last week it was the pollution control officers. This week it is the damn power cuts. How am I gonna pay my bills? How am I to pay salaries to all those people working on the shop floor? I am not sure how long I can sustain in this business.

The Indian Entrepreneur: There’s a plant closing down in China. I am sure there are opportunities out there for me to go out and grab, and thereby grow my business. While that happens, my margins could take a hit and let me keep my eye on the ball and focus on the long term.

The Customer: Everything was going so well and then thanks to all the polluting factories, I need to find another skilled guy in another business friendly geography where my supplies are guaranteed with equal or perhaps better quality.

Mr. Market: He is swinging in between what will happen in the next quarter and what will happen over the long term. On days when he is worried about the next quarter, he offloads his stake. And on days when he is focused on the long term economics of the business, he thinks “This China + 1 thing is real after all. More and more business could fall into this company’s lap. Let me just hold on to this business. Better yet, let me increase my stake in this business.”

Let’s look at some disconfirming evidence too. Below is one instance wherein they were unable to pass on price increases to their customers.

That being said, here are my conclusions.

Equity investing is not a science. Sometimes, we just need to stomach the volatility, the uncertainty & the self-doubt that accompanies falling stock prices. Particularly so, if the entrepreneur has a decent, execution track record.

Disruption in APIs isn’t new. It’s been there for a couple of years and is here to stay. And entrepreneurs who have handled it successfully before, could possibly handle it well in the future too.

What Mr. Market perceives as disruption, is perceived by the entrepreneur as an opportunity. There are times when blind belief in the entrepreneur is foolhardy. Yet there are times, when you need to go with your gut feel and just trust that the jockey will make things right.

You don’t want to be that guy who calculates too much and thinks too little.

Disclaimer: I have been wrong with my thesis in the past and could be wrong this time or in the future too. These are my thoughts today and could change as and when the situation evolves or whenever disconfirming evidence presents itself.

I recently revisited an interview by Mr. Raamdeo Agrawal, where he said “I am very happy when the markets fall and I can buy something that adds more value to my portfolio. Markets don’t understand high quality value in the short term. Focusing on value is the key. What we have learnt is that the value of the company remains steady even if there are external events. Only the price changes. Till 1998 nobody knew about the index. People looked at only individual stocks. This focus on index has spoilt the game. We focus on value instead.“

The question I am seeking an answer to is whether the index really matters or is it just plain noise and we should be focusing instead on what our portfolio companies are doing currently and expected to do in the future, while disregarding what the market does.

The idea behind doing this post is to explore what happens when a small or a mid cap investor buys a basket of growing small caps and does not worry about the small cap index or the Nifty or the Sensex or any other indexes, at all. And should one really worry about index levels if businesses we are holding in our portfolios are doing well regardless? Articulated differently, is time in the markets more important than timing the markets.

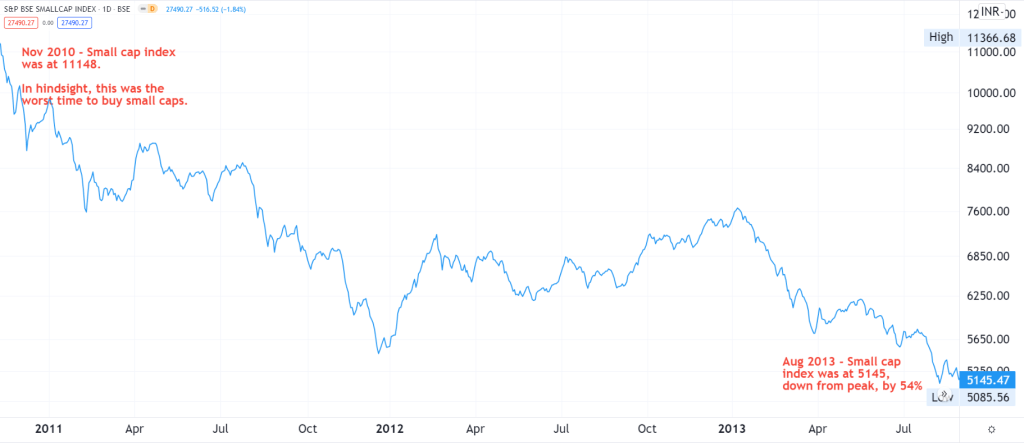

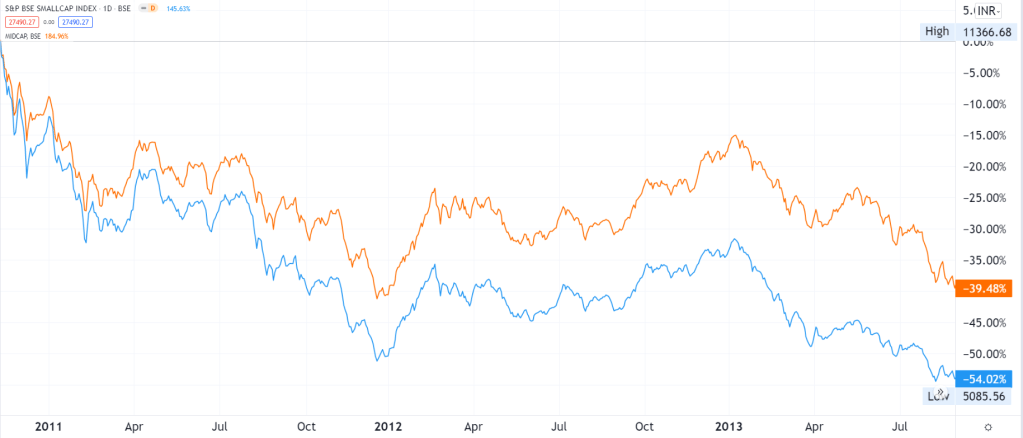

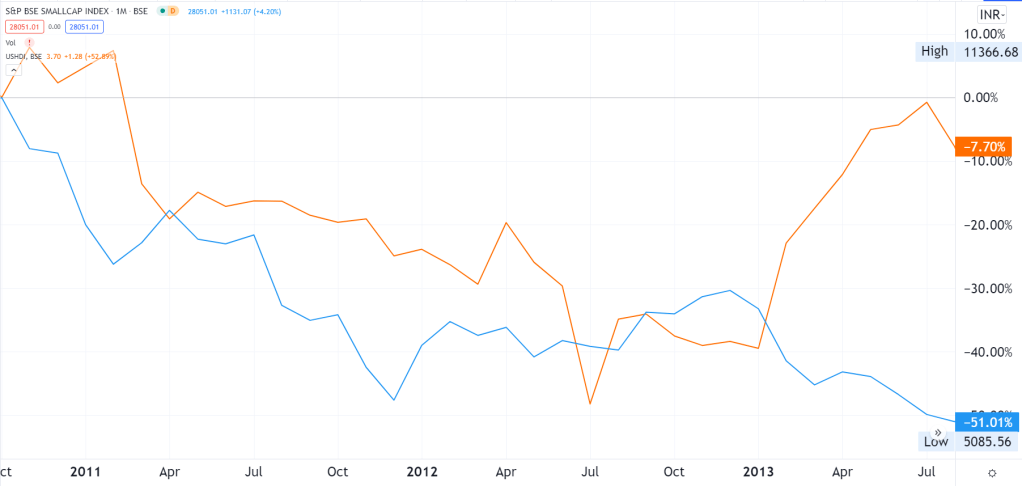

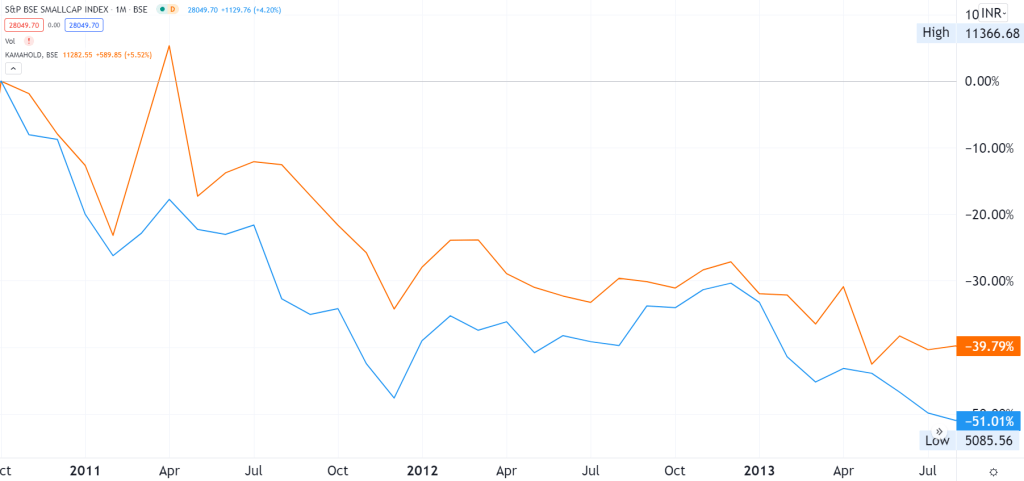

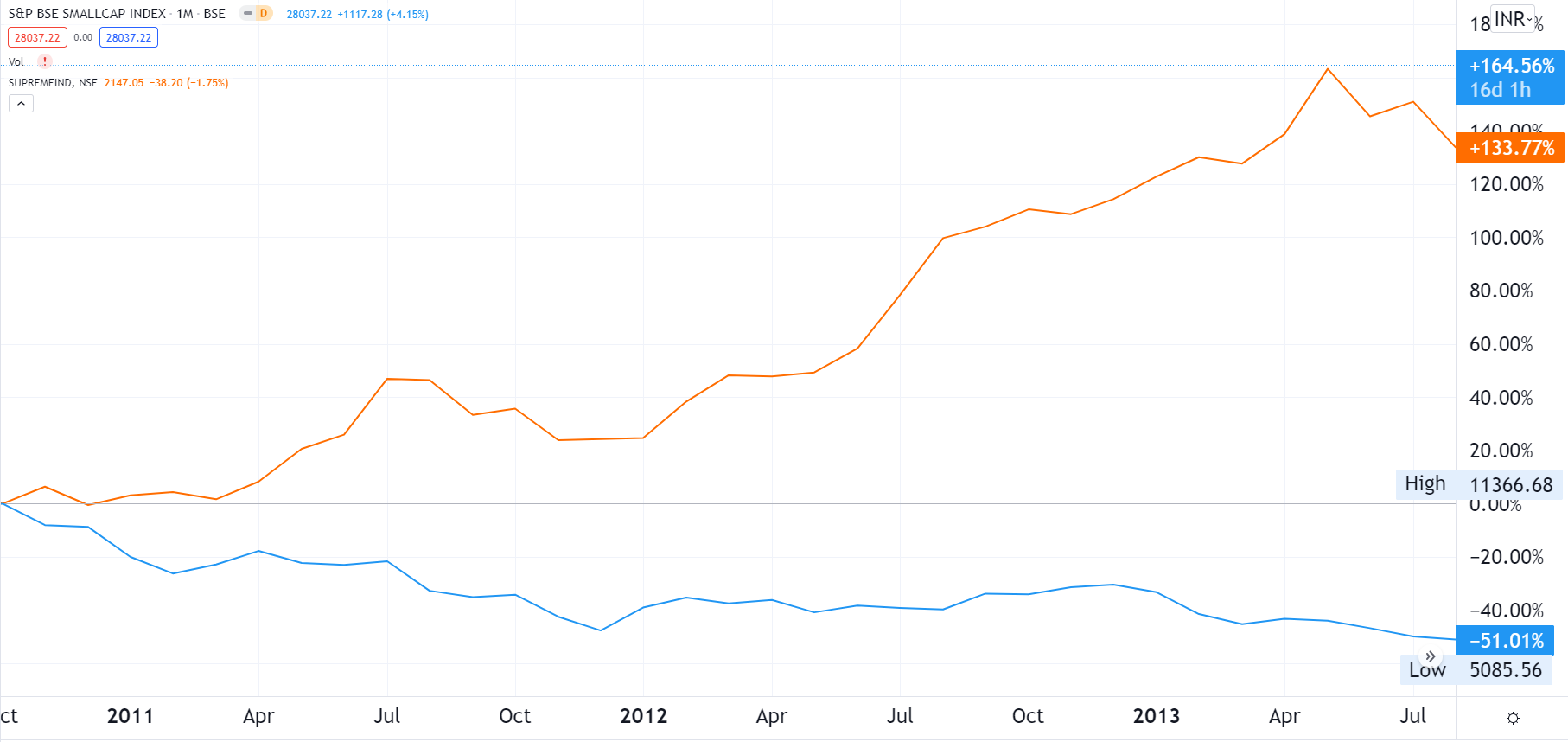

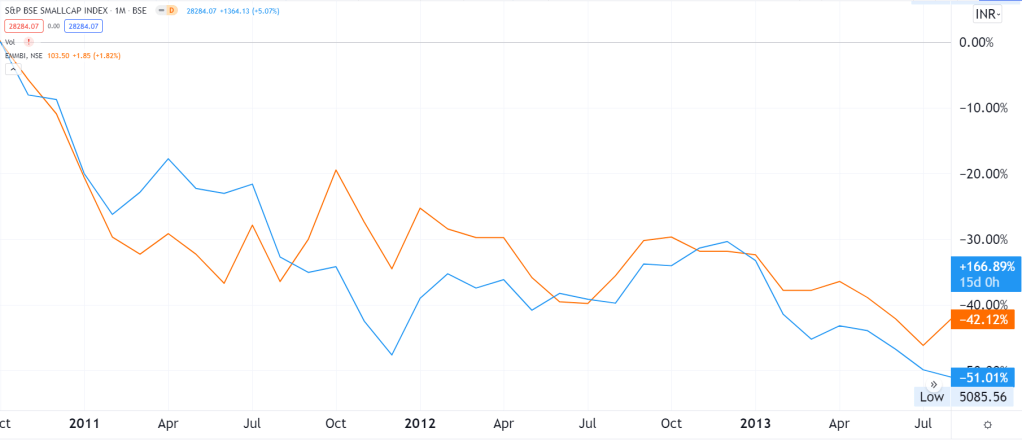

What kind of profits or losses would one encounter, if he/she bought small & mid caps in Nov 2010, when the small cap index topped out & held them until Aug 2013, when the index was down by 54% from its previous peak?

And here’s how the BSE Mid cap index moved during the same period. The mid cap index was down by 40% while the small cap index was down by 54%

Methodology used

Filtered companies that grew their profits by at least 15% in FY2009, FY2010 & FY2011.

Removed a handful of companies where charts are not available due to corporate actions such as delisting, mergers, etc.

Removed large caps since most of us are interested in small/mid caps only.

Analyzed the out-performers from this group.

Dividends excluded.

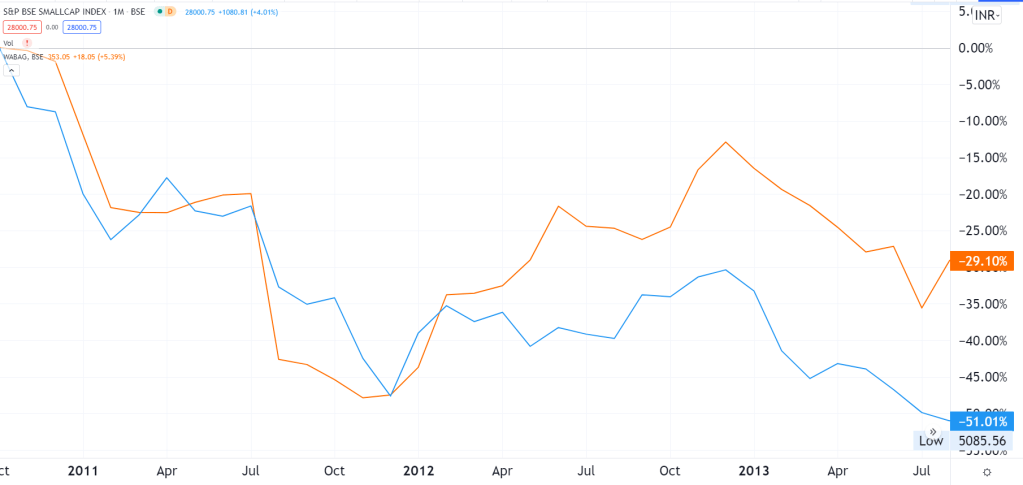

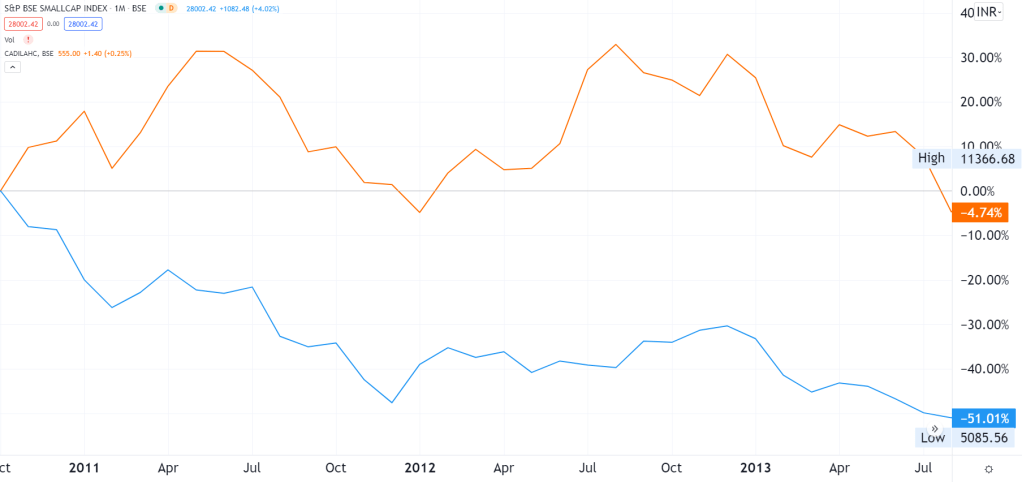

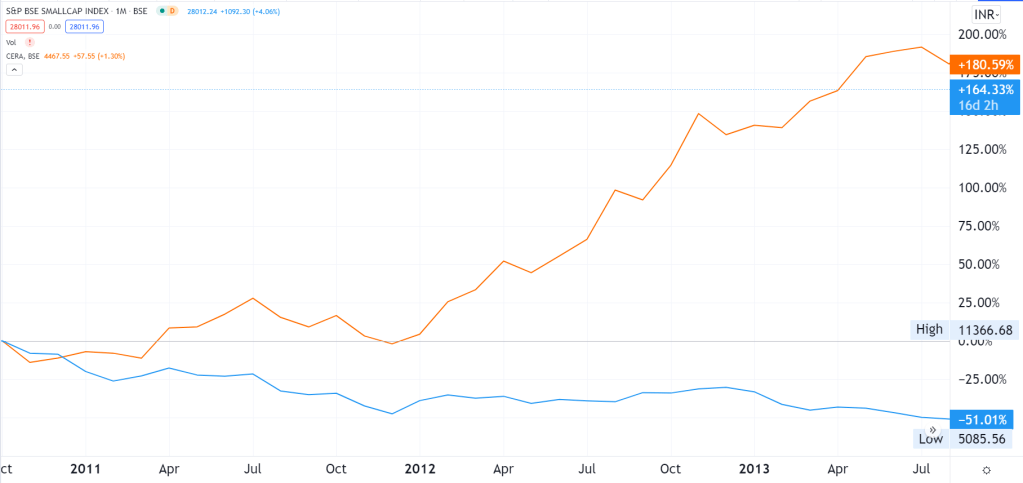

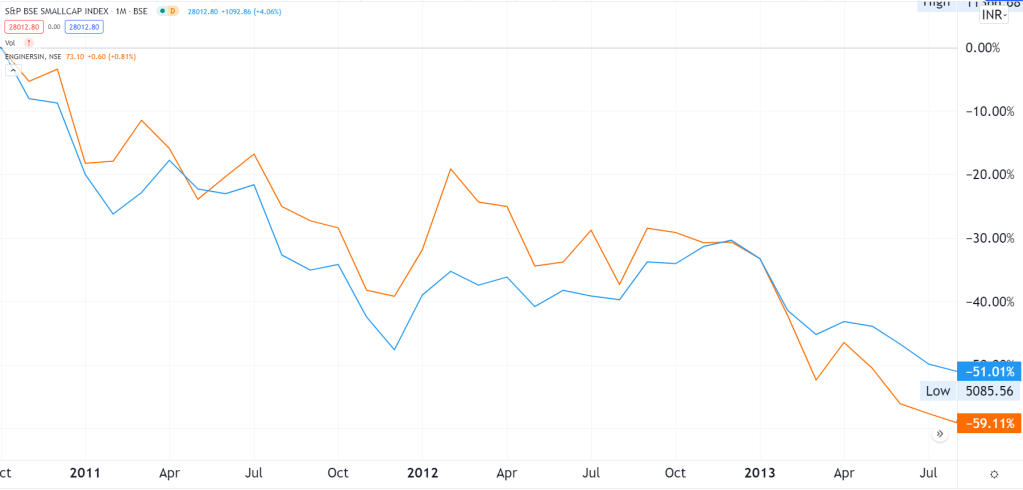

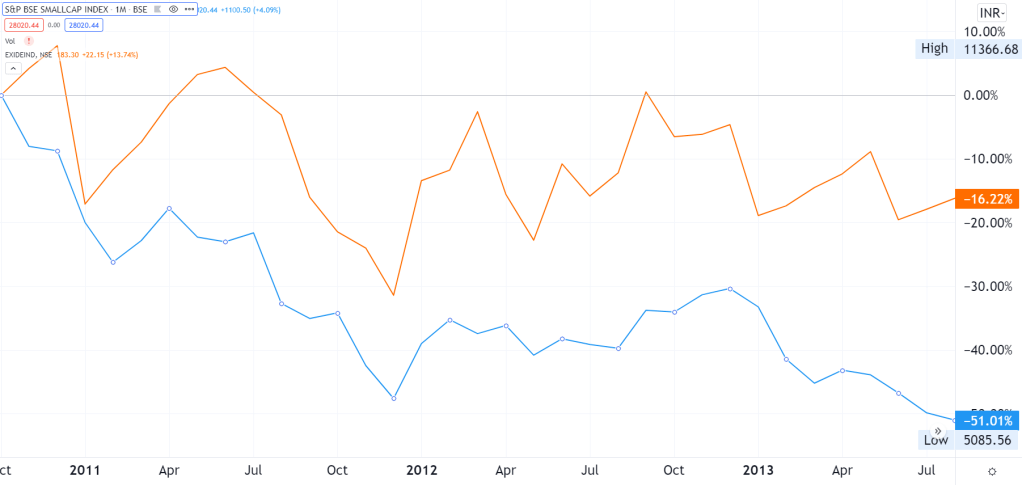

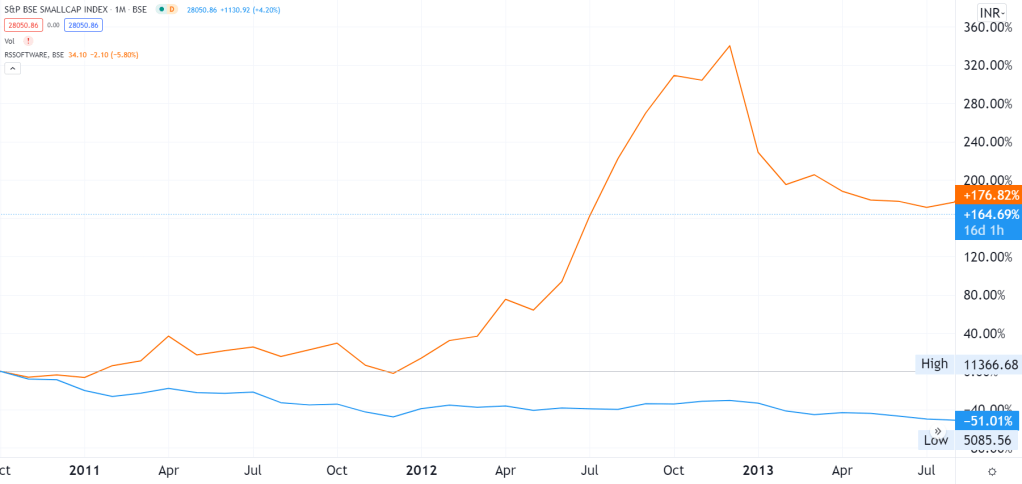

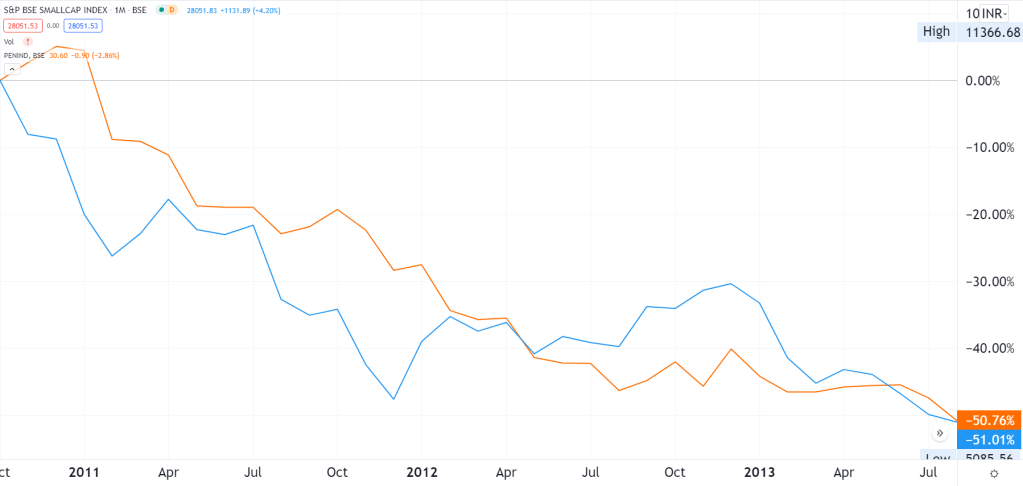

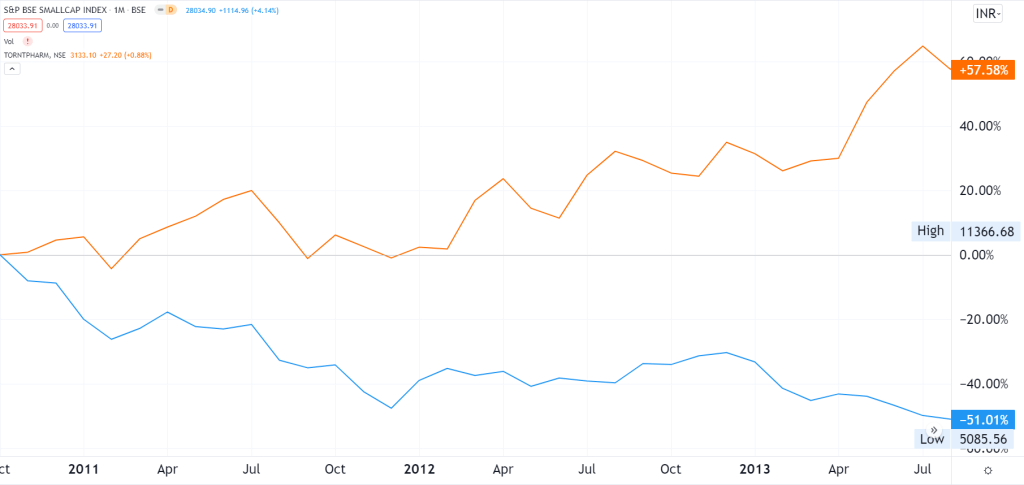

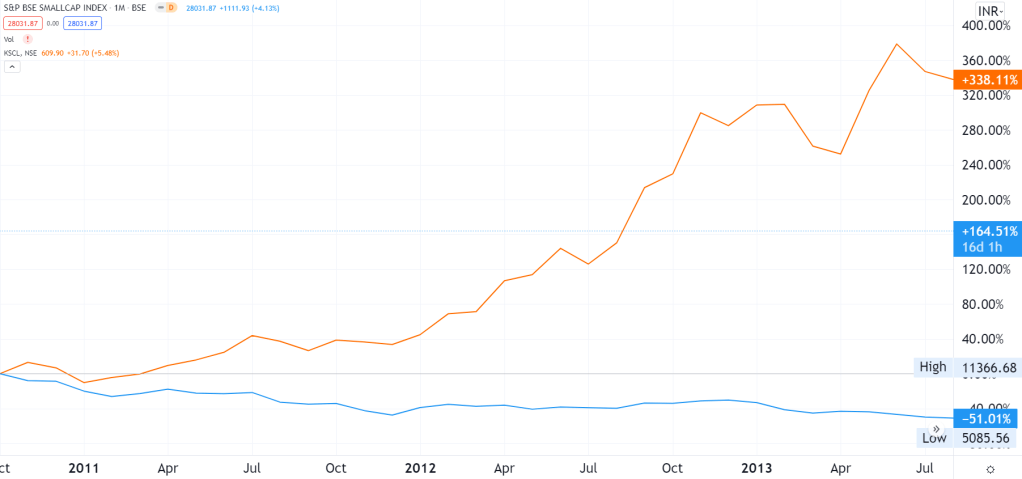

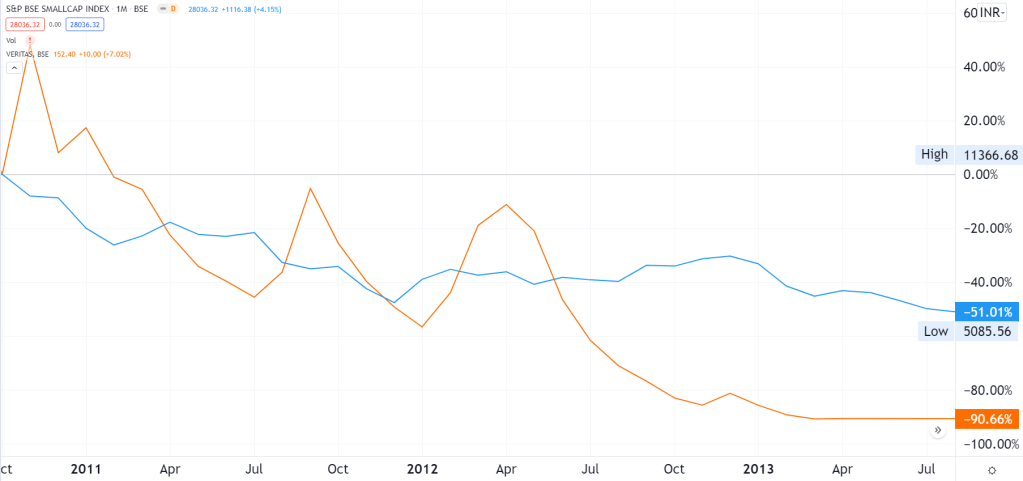

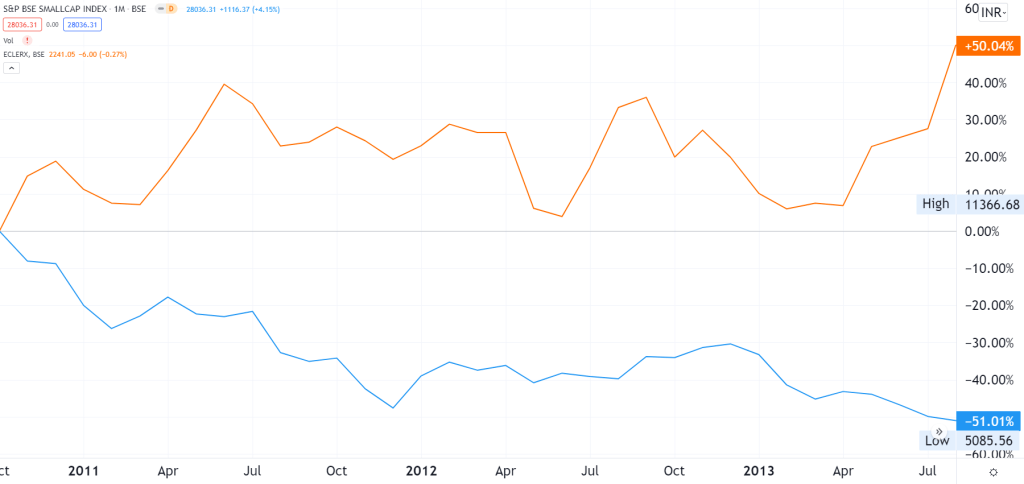

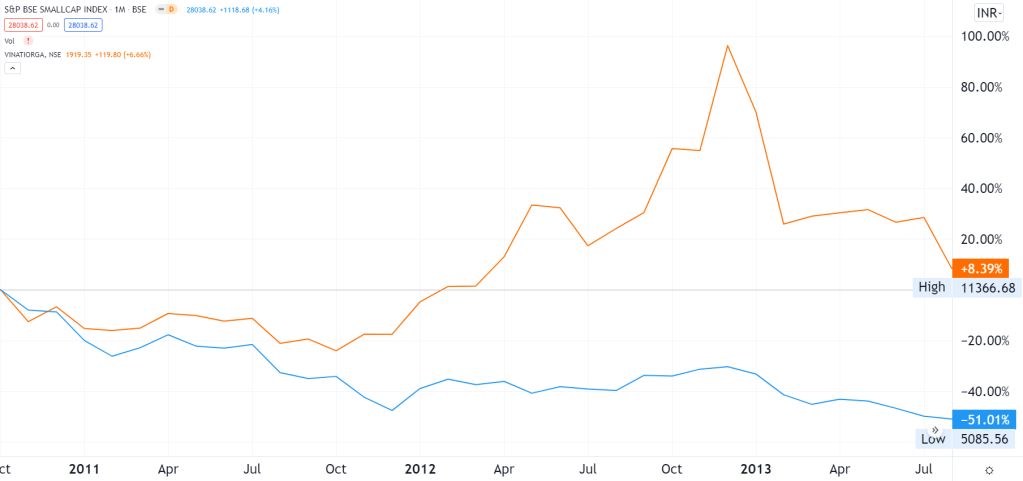

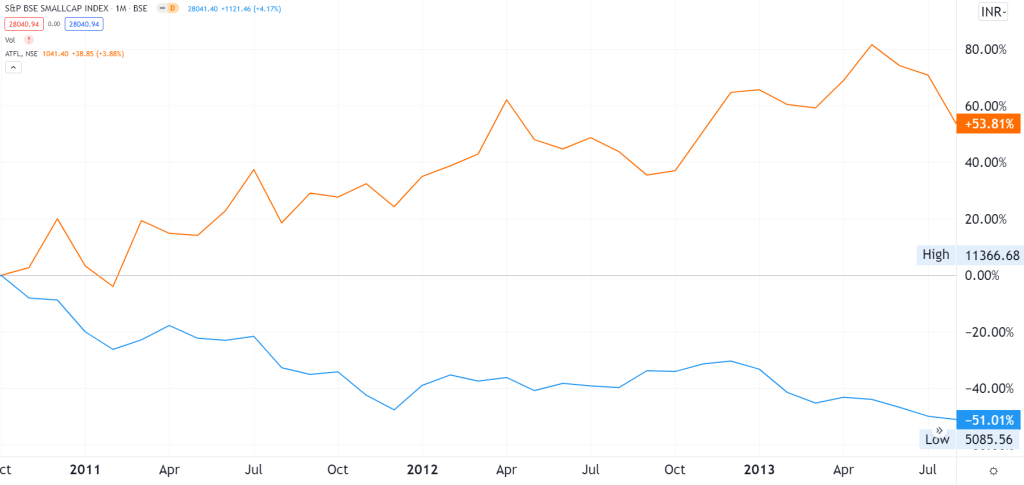

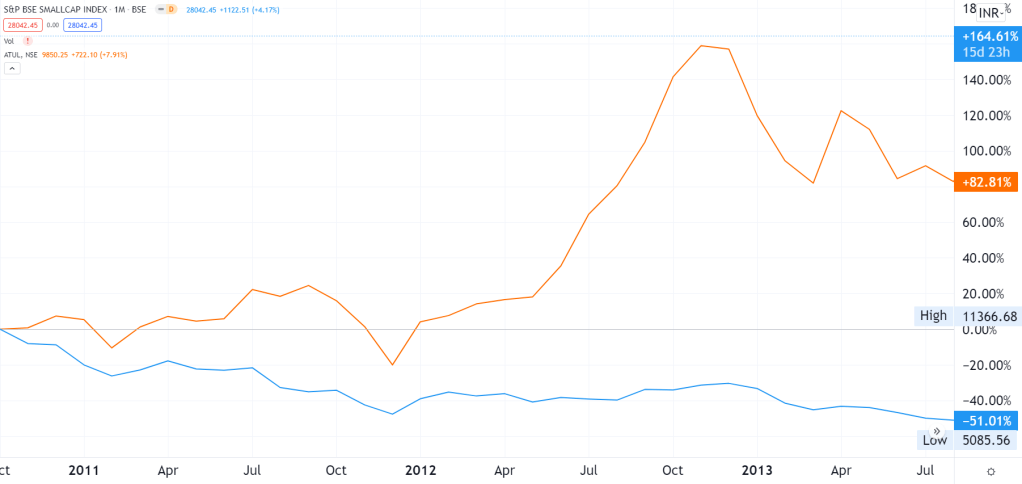

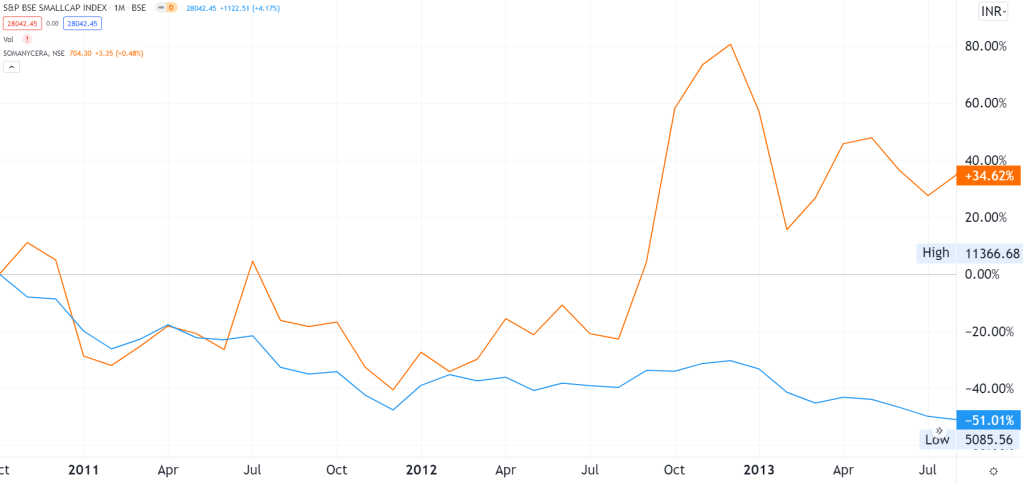

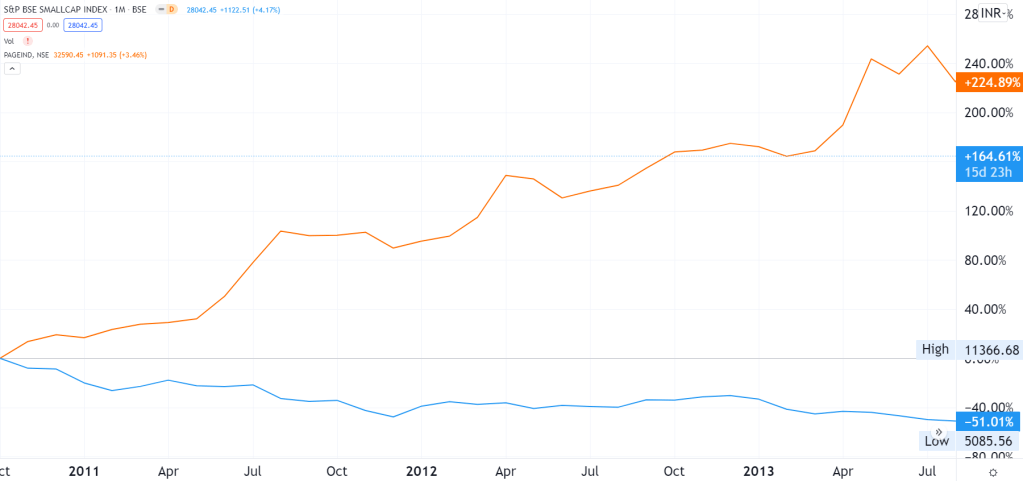

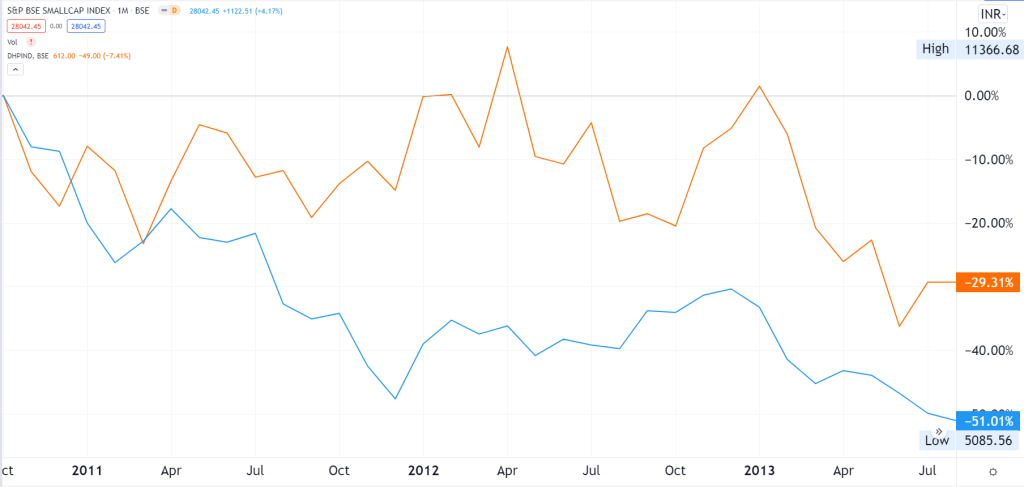

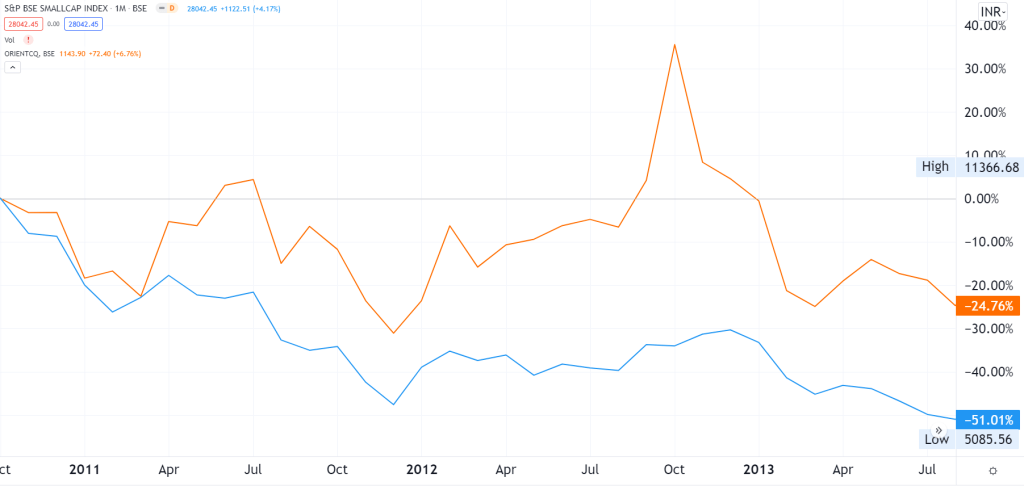

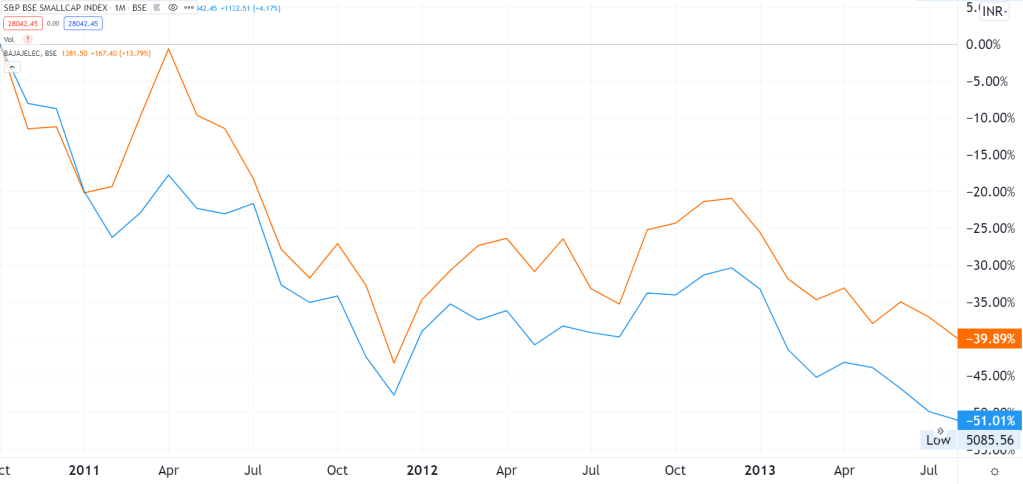

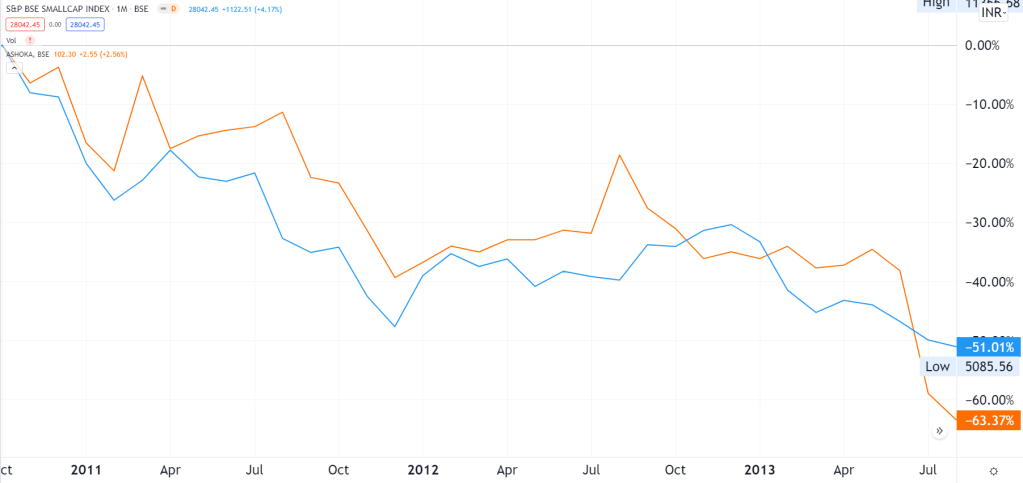

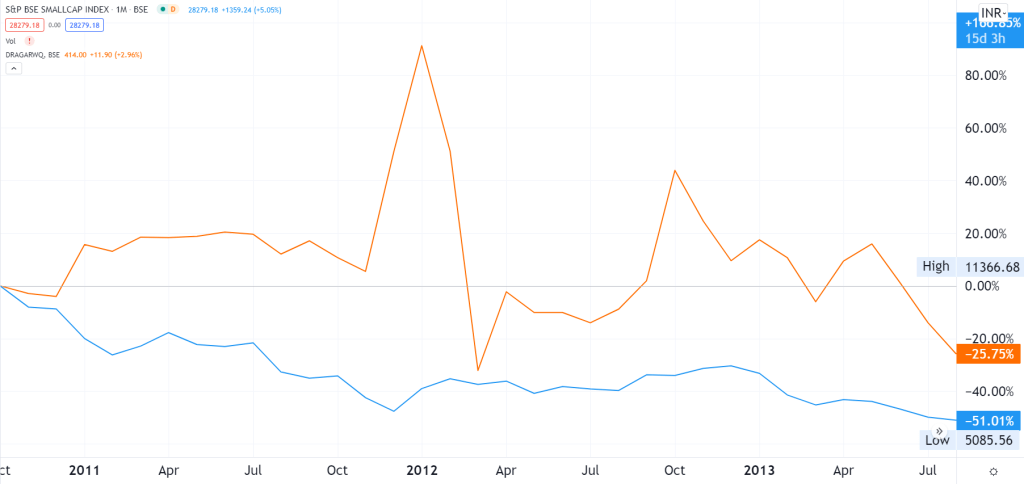

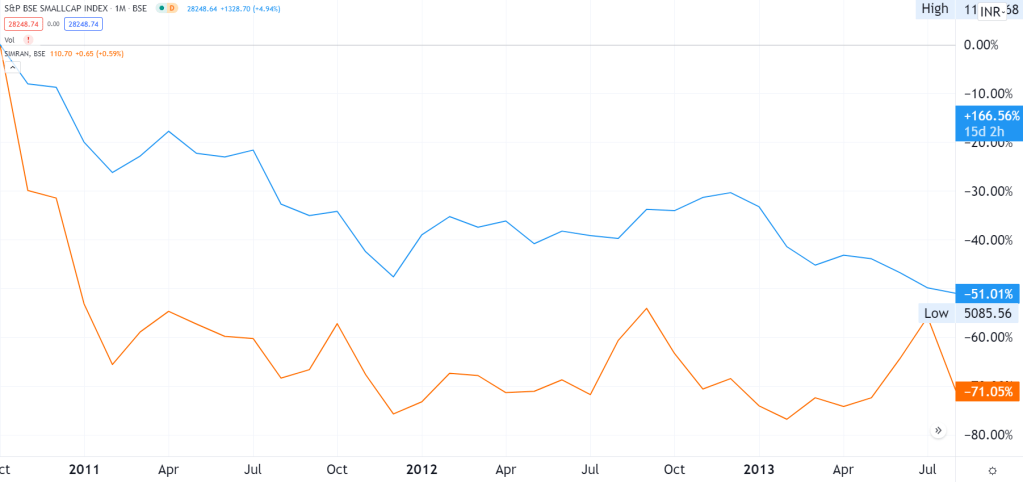

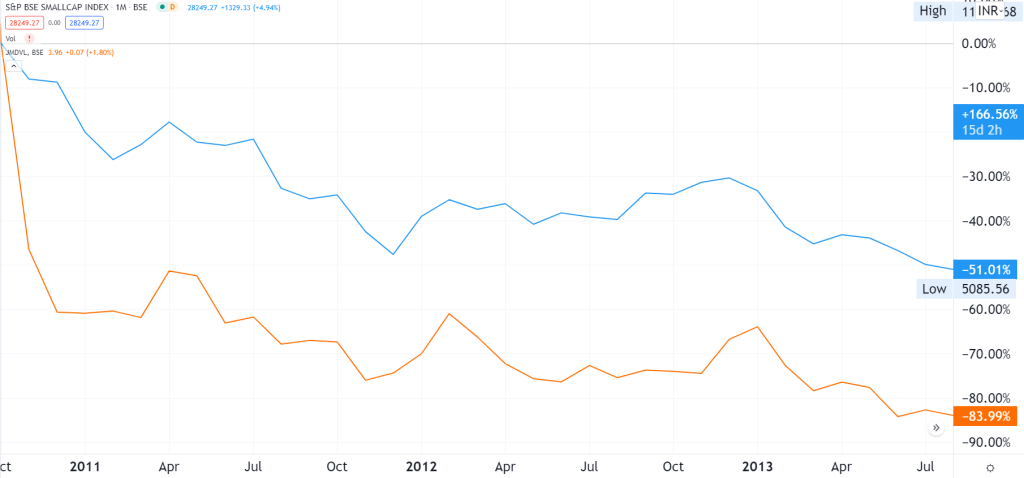

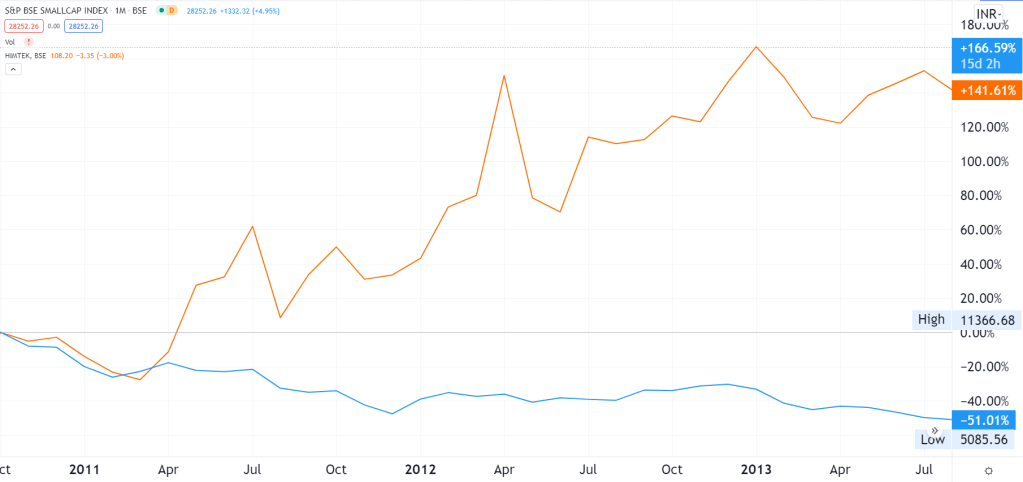

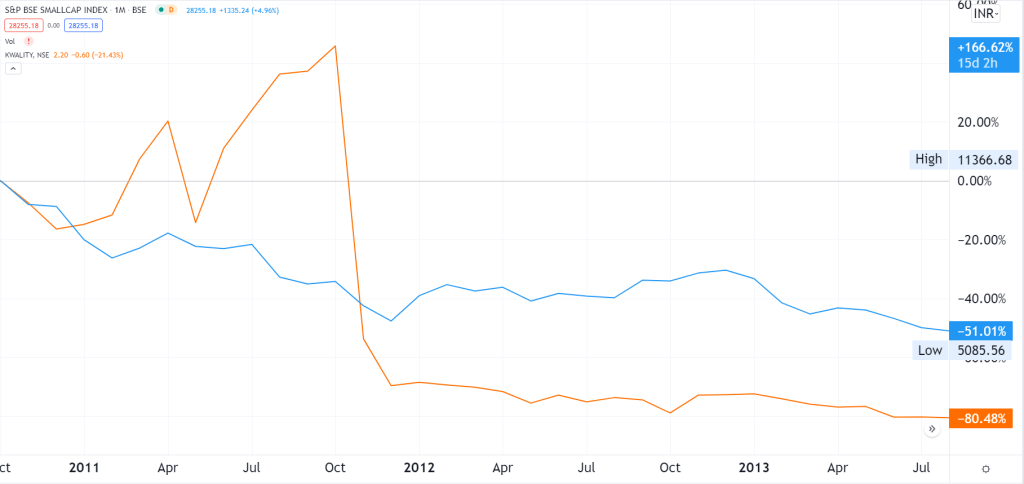

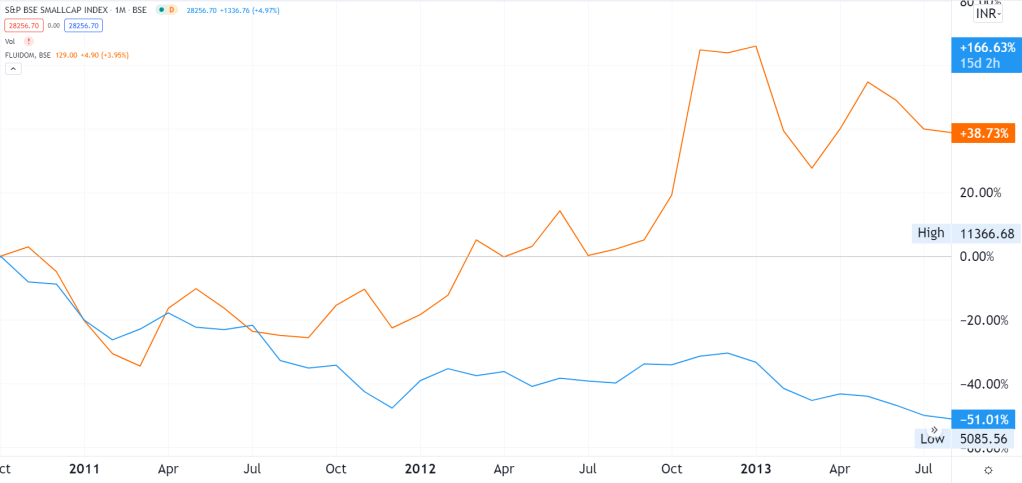

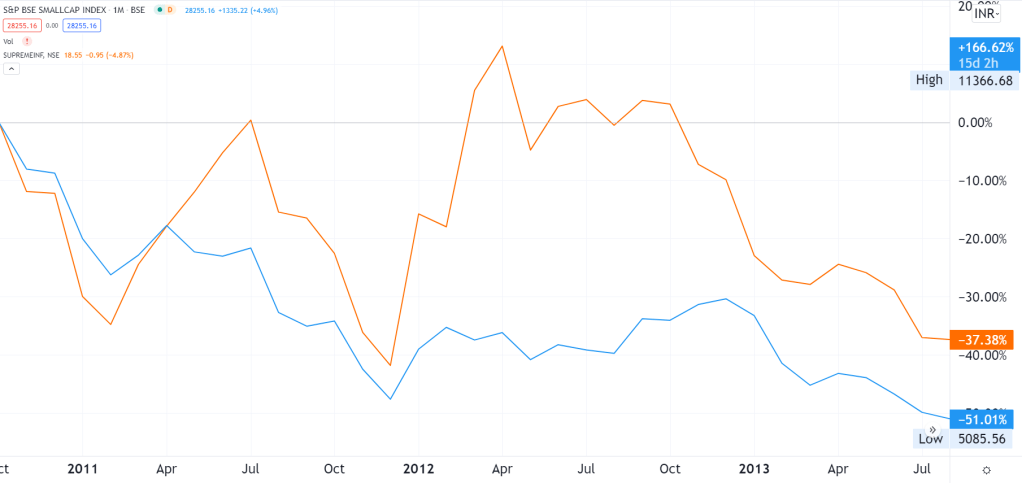

Note: Blue lines in each of the below graphs represent the BSE Small Cap Index while orange lines represent the corresponding stock.

Solar Industries Estimated Market cap in 2010 – 1124 Crs Outperformed vs the small cap index 62% absolute returns

Redington India Estimated Market cap in 2010 – 3671 Crs Outperformed vs the small cap index Negative absolute returns

Apollo Hospitals Enterprise Estimated Market cap in 2010 – 7628 Crs Outperformed vs the small cap index 69% absolute returns

Va Tech Wabag Estimated Market cap in 2010 – 2094 Crs Outperformed vs the small cap index Negative absolute returns

Cadila Healthcare Estimated Market cap in 2010 – 16042 Crs Outperformed vs the small cap index Negative absolute returns

Vardhman Textile Estimated Market cap in 2010 – 1977 Crs Outperformed vs the small cap index Negative absolute returns

Swaraj Engines Estimated Market cap in 2010 – 599 Crs Outperformed vs the small cap index 9% absolute returns

Cera Sanitaryware Estimated Market cap in 2010 – 238 Crs Outperformed vs the small cap index 180% absolute returns

Castrol India Estimated Market cap in 2010 – 12893 Crs Outperformed vs the small cap index 48% absolute returns

Mayur Uniquoters Estimated Market cap in 2010 – 171 Crs Outperformed vs the small cap index 89% absolute returns

Engineers India Estimated Market cap in 2010 – 10029 Crs Under performed vs the small cap index Negative absolute returns

Jenburkt Pharmaceuticals Estimated Market cap in 2010 – 40 Crs Outperformed vs the small cap index Negative absolute returns

Torrent Power Estimated Market cap in 2010 – 17250 Crs Under performed vs the small cap index Negative absolute returns

Exide Industries Estimated Market cap in 2010 – 14350 Crs Outperformed vs the small cap index Negative absolute returns

Indian Toners & Developers Estimated Market cap in 2010 – 39 Crs Under performed vs the small cap index Negative absolute returns

Consolidated Finvest & Holdings Estimated Market cap in 2010 – 297 Crs Under performed vs the small cap index Negative absolute returns

Superhouse Estimated Market cap in 2010 – 79 Crs Outperformed vs the small cap index Negative absolute returns

R S Software (India) Estimated Market cap in 2010 – 63 Crs Outperformed vs the small cap index 177% absolute returns

Pennar Industries Estimated Market cap in 2010 – 782 Crs Under performed vs the small cap index Negative absolute returns

Phyto Chem (India) Estimated Market cap in 2010 – 6 Crs Outperformed vs the small cap index 60% absolute returns

Narmada Gelatines Estimated Market cap in 2010 – 41 Crs Outperformed vs the small cap index 31% absolute returns

Shree Renuka Sugars Estimated Market cap in 2010 – 21040 Crs Under performed vs the small cap index Negative absolute returns

Ushdev International Estimated Market cap in 2010 – 1429 Crs Outperformed vs the small cap index Negative absolute returns

Kama Holdings Estimated Market cap in 2010 – 352 Crs Outperformed vs the small cap index Negative absolute returns

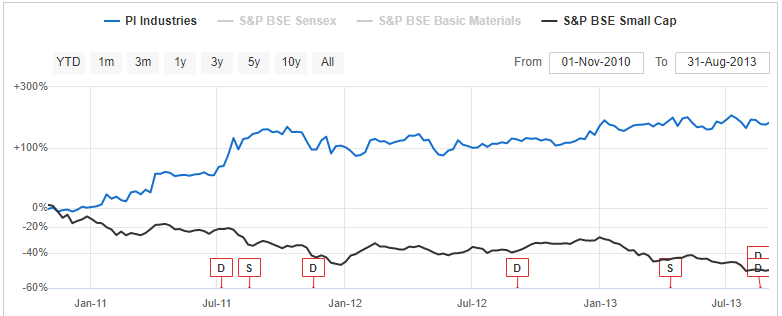

P I Industries Estimated Market cap in 2010 – 771 Crs Outperformed vs the small cap index 140% absolute returns

Supreme Industries Estimated Market cap in 2010 – 2078 Crs Outperformed vs the small cap index 134% absolute returns

Torrent Pharmaceuticals Estimated Market cap in 2010 – 4756 Crs Outperformed vs the small cap index 58% absolute returns

Balaji Amines Estimated Market cap in 2010 – 164 Crs Outperformed vs the small cap index Negative absolute returns

RPG Life Sciences Estimated Market cap in 2010 – 182 Crs Outperformed vs the small cap index Negative absolute returns

Kaveri Seed Company Estimated Market cap in 2010 – 486 Crs Outperformed vs the small cap index 338% absolute returns

Veritas (India) Estimated Market cap in 2010 – 1080 Crs Under performed vs the small cap index Negative absolute returns

eClerx Services Estimated Market cap in 2010 – 1872 Crs Outperformed vs the small cap index 50% absolute returns

Vinati Organics Estimated Market cap in 2010 – 411 Crs Outperformed vs the small cap index 8% absolute returns

Agro Tech Foods Estimated Market cap in 2010 – 108 Crs Outperformed vs the small cap index 54% absolute returns

Stylam Industries Estimated Market cap in 2010 – 28 Crs Outperformed vs the small cap index Negative absolute returns

Garware Polyester Estimated Market cap in 2010 – 641 Crs Under performed vs the small cap index Negative absolute returns

Atul Ltd Estimated Market cap in 2010 – 579 Crs Outperformed vs the small cap index 83% absolute returns

Somany Ceramics Estimated Market cap in 2010 – 286 Crs Outperformed vs the small cap index 35% absolute returns

Vidhi Specialty Food Ingredients Estimated Market cap in 2010 – 21 Crs Outperformed vs the small cap index Negative absolute returns

Page Industries Estimated Market cap in 2010 – 1565 Crs Outperformed vs the small cap index 225% absolute returns

Thangamayil Jewellery Estimated Market cap in 2010 – 240 Crs Outperformed vs the small cap index 12% absolute returns

DHP India Estimated Market cap in 2010 – 11 Crs Outperformed vs the small cap index Negative absolute returns

Sudarshan Chemical Industries Estimated Market cap in 2010 – 468 Crs Outperformed vs the small cap index Negative absolute returns

Oriental Carbon & Chemicals Estimated Market cap in 2010 – 142 Crs Outperformed vs the small cap index Negative absolute returns

Bajaj Electricals Estimated Market cap in 2010 – 3640 Crs Outperformed vs the small cap index Negative absolute returns

DFM Foods Estimated Market cap in 2010 – 106 Crs Outperformed vs the small cap index 138% absolute returns

Ashoka Buildcon Estimated Market cap in 2010 – 1994 Crs Under performed vs the small cap index Negative absolute returns

Manali Petrochemicals Estimated Market cap in 2010 – 312 Crs Outperformed vs the small cap index Negative absolute returns

BASF India Estimated Market cap in 2010 – 3023 Crs Outperformed vs the small cap index Negative absolute returns

India Motor Parts & Accessories Estimated Market cap in 2010 – 303 Crs Outperformed vs the small cap index 19% absolute returns

Gravita India Estimated Market cap in 2010 – 351 Crs Under performed vs the small cap index Negative absolute returns

HSIL Estimated Market cap in 2010 – 278 Crs Outperformed vs the small cap index Negative absolute returns

Caprihans India Estimated Market cap in 2010 – 278 Crs Outperformed vs the small cap index Negative absolute returns

Dr Agarwals Eye Hospital Estimated Market cap in 2010 – 40 Crs Outperformed vs the small cap index Negative absolute returns

Triton Valves Estimated Market cap in 2010 – 103 Crs Under performed vs the small cap index Negative absolute returns

Simran Farms Estimated Market cap in 2010 – 29 Crs (Can be considered a penny stock) Under performed vs the small cap index Negative absolute returns

Ramky Infrastructure Estimated Market cap in 2010 – 2568 Crs Under performed vs the small cap index Negative absolute returns

Josts Engineering Company Estimated Market cap in 2010 – 35 Crs Outperformed vs the small cap index Negative absolute returns

DIC India Estimated Market cap in 2010 – 305 Crs Outperformed vs the small cap index Negative absolute returns

Educomp Solutions Estimated Market cap in 2010 – 7708 Crs Under performed vs the small cap index Negative absolute returns

JMD Ventures Estimated Market cap in 2010 – 297 Crs Under performed vs the small cap index Negative absolute returns

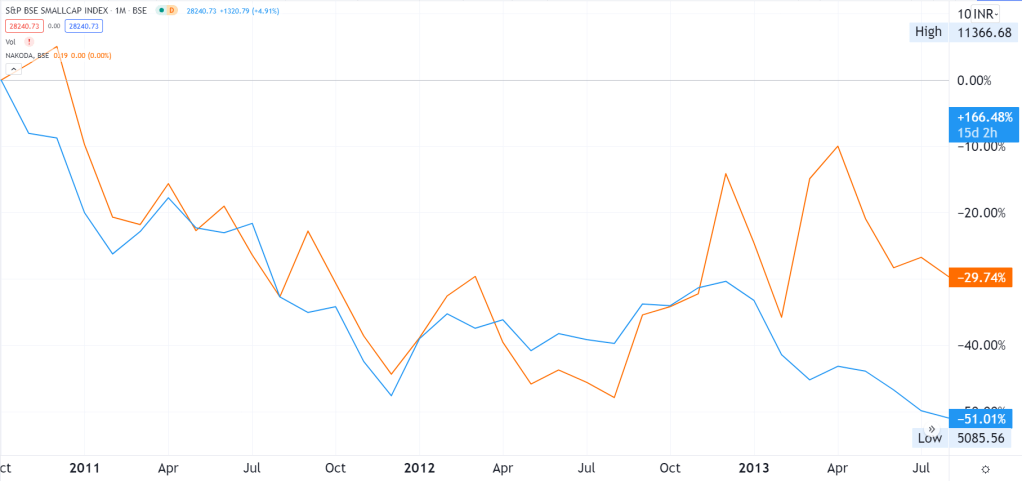

Nakoda Ltd Estimated Market cap in 2010 – 570 Crs Outperformed vs the small cap index Negative absolute returns

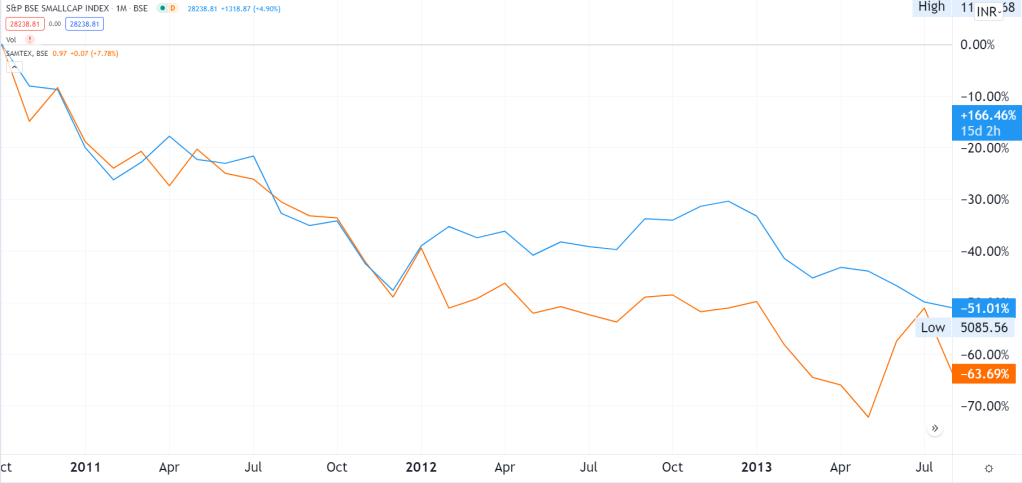

Samtex Fashions Estimated Market cap in 2010 – 53 Crs (Penny stock) Under performed vs the small cap index Negative absolute returns

SEL Manufacturing Company Estimated Market cap in 2010 – 2 Crs (Penny stock) Under performed vs the small cap index Negative absolute returns

Silver Oak (India) Ltd Estimated Market cap in 2010 – 6 Crs (Penny stock) Outperformed vs the small cap index 10% absolute returns

Technofab Engineering Estimated Market cap in 2010 – 192 Crs Under performed vs the small cap index Negative absolute returns

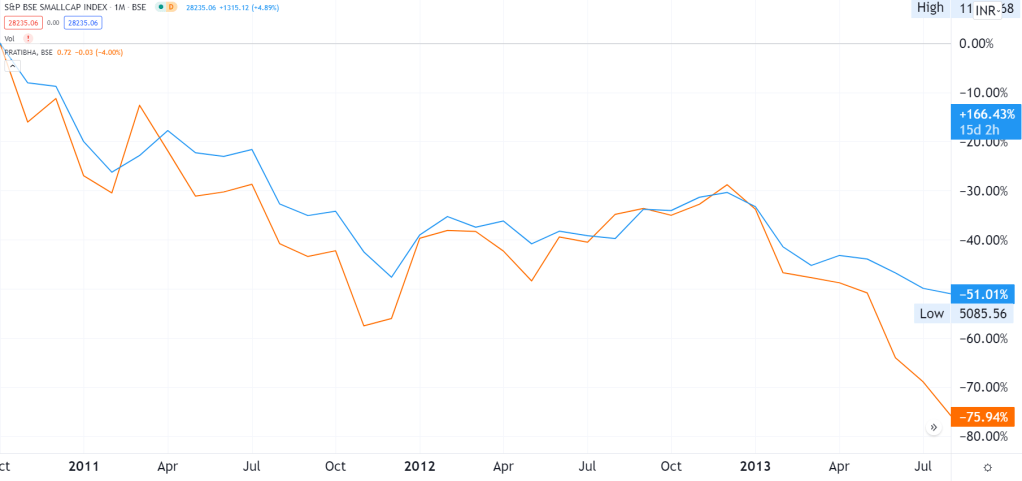

Pratibha Industries Estimated Market cap in 2010 – 1912 Crs Outperformed vs the small cap index Negative absolute returns

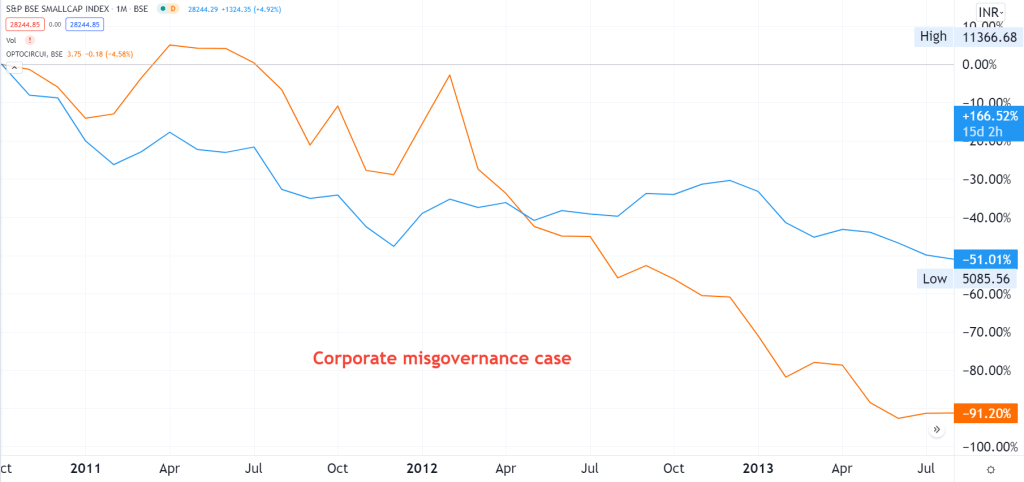

Opto Circuits (India) Estimated Market cap in 2010 – 7063 Crs Outperformed vs the small cap index Negative absolute returns

Him Teknoforge Estimated Market cap in 2010 – 84 Crs Outperformed vs the small cap index 142% absolute returns

Kwality Ltd Estimated Market cap in 2010 – 3084 Crs Outperformed vs the small cap index Negative absolute returnsdue to suspected operator manipulation in the stock

IRB Infrastructure Developers Estimated Market cap in 2010 – 3084 Crs Outperformed vs the small cap index Negative absolute returns

Fluidomat Estimated Market cap in 2010 – 25 Crs Outperformed vs the small cap index 39% absolute returns

Garden Silk Mills Estimated Market cap in 2010 – 619 Crs Under performed vs the small cap index Negative absolute returns

Simplex Castings Estimated Market cap in 2010 – 73 Crs Under performed vs the small cap index Negative absolute returns

Sacheta Metals Estimated Market cap in 2010 – 154 Crs Under performed vs the small cap index Negative absolute returns

Mahalaxmi Rubtech Estimated Market cap in 2010 – 417 Crs Under performed vs the small cap index Negative absolute returns

ARSS Infrastructure Projects Estimated Market cap in 2010 – 3006 Crs Under performed vs the small cap index Negative absolute returns

Supreme Infrastructure India Estimated Market cap in 2010 – 748 Crs Outperformed vs the small cap index Negative absolute returns

Inani Marbles & Industries Estimated Market cap in 2010 – 44 Crs Outperformed vs the small cap index 20% absolute returns

Jindal Hotels Estimated Market cap in 2010 – 45 Crs Under performed vs the small cap index Negative absolute returns

Emmbi Industries Estimated Market cap in 2010 – 39 Crs Outperformed vs the small cap index Negative absolute returns

Paramount Cosmetics Estimated Market cap in 2010 – 20 Crs Under performed vs the small cap index Negative absolute returns

MBL Infrastructures Estimated Market cap in 2010 – 1446 Crs Under performed vs the small cap index Negative absolute returns

XPRO India Estimated Market cap in 2010 – 1446 Crs Under performed vs the small cap index Negative absolute returns

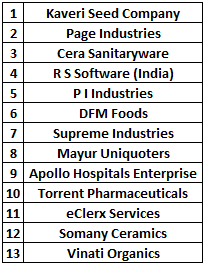

25 stocks that gave positive returns until 2013, despite the small cap index being half of what it was in 2010.

What was different between the companies that outperformed the index vs the ones that didn’t?

Here’s some data to chew.

13 Companies grew their sales by more than 15% throughout 2011, 2012 & 2013.

4 companies grew their profits by more than 15% throughout 2011, 2012 & 2013.

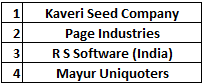

22 out of 25 companies had above average ROEs, throughout.

Now, some of the above companies might have had ongoing capacity expansion projects which might have optically suppressed their ROEs. Yet, these companies’ businesses and stocks continued to do well in what was perceived to be the worst possible time to get into small caps, in many years.

Let’s try some dis-confirming evidence now. First some data.

Total # of companies (small & mid cap) that grew PAT by at least 15% YoY in that period 95 Total # of companies that outperformed 25 Total # of companies that under performed 59 Total # of companies excluded due to corporate actions / lack of data 11

Did any of the companies that showed negative returns, have an ROE of 15% consistently? None. Zero.

Did any of the companies that showed negative returns, have consistent growth of more than 15% per annum? Again, the answer is no.

This would mean that ROE & growth are the engines which drive stock prices.

How can we make this study better?

If you have suggestions on how we can make this study better and as bias-free as possible, please drop me a note at barath@bigvisioninvesting.com or in the comments box below and I’ll try to see how best we can incorporate it.

Conclusions thus far:

Businesses (and stocks) can do well despite all odds. Imagine the pain you’d have gone through, had you sold one of the out-performers because of all the market related noise in the media, thereby trying to time the market.

Stock prices are driven by growth, ROE (& the US Fed) in the long run. And stocks of businesses which tick both boxes can do well, in the worst possible market conditions.

Focus more on the business is doing than on what the market indices will do.

I will do a similar blog for the next small cap cycle which happened from Jan 2018 to Mar 2020 (chart below), just to find out if these conclusions hold good in another time frame. Stay tuned.

Selling stocks is exponentially more difficult than buying. If you sell a winner at the wrong time, you could have the financial regret of a lifetime. On the flip side, there were times I ended up kicking myself for not having sold losing stocks in time, thereby magnifying the somewhat inevitable smaller losses I would have otherwise had.

It takes quite a few trials and errors before one figures out how to sell stocks in time. And even after one thinks he’s got it, could still go wrong.

The context is that like a lot of my peers, I was anxious about how this current bull run will play out. Will we experience another bull market like the one we experienced between 2009 and Feb 2020? Or will the market correct from here? If yes, then I shouldn’t be repeating the mistakes from the last cycle and convert paper profits to cash.

Bear markets sneak in when most poor mortals aren’t expecting them and not when there is a lot of debate on Twitter about whether it will crash this week or the next or the one after that.

While I am no expert at timing the markets or the macros, let me give this a shot anyway. In the aftermath of the 2008 housing bubble, the US Fed’s balance sheet expanded multi-fold and all those newly printed dollars chased equities and markets, the world over, shot up. Will the same story play out yet again over the next decade or so? A layman’s guess would be yes.

And here’s what somebody who has a good handle on macros, said about liquidity. Stanley Druckenmiller (left), one of the guys who famously broke the Bank of England, along with his mentor, the legendary, George Soros (right), in a highly leveraged bet, once said,

“Earnings don’t move the overall market; it’s the Federal Reserve Board. Focus on the central banks and focus on the movement of liquidity. Most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.”

With liquidity, earnings and the several moving parts that work in the background to keep the market engine running, it is hard to make a sure shot prediction about market direction. Think about how many people got out in time before the March 2020 crash and whether the same set of people had the nerve to get back in time before the markets ran up so suddenly.

I don’t think there are easy answers to when a bear market will come or if at all it will be in the near future. While I have been dealing with this uncertainty in my mind, I’ve simultaneously been reading How to make money in stocks by William O’Neil. For somebody like me, who loves reading financial history, this book is an absolute delight.

O’Neil is a genius. He collated fundamental and technical data of historical multi baggers, as early as the year 1885. And he put them into his mainframe computer in the 1960s to analyze what works on Wall Street. So this guy got his hands on a mainframe (remember there was no Windows then) to analyze stocks much before Bill Gates was famously dozing off on his desk, working on computers, in 1968. Woah!!

How O’Neil collated and analyzed so much data at a time when computers used to work like the ones below is quite fascinating.

Anyway, like a lot of other things in life, one naively ignored idea is that of looking at history and seeing how others solved the same problem I am facing today. And here’s how O’Neil solved the problem of being able to sell winning stocks in time. He wrote –

“Have you ever analyzed every one of your failures so you can learn from them? Few people do. What a tragic mistake you’ll make if you don’t look carefully at yourself and the decisions you’ve made in the stock market that did not work. You get better only when you learn what you’ve done wrong. This is the difference between winners and losers, whether in the market or in life. If you got hurt in the 2000 or 2008 bear market, don’t get discouraged and quit. Plot out your mistakes on charts, study them, and write some additional new rules that, if you follow them, will correct your mistakes and let you avoid the actions that cost you a lot of time and money.”

Hmmm.. so he looked at his past trades and so should I. I have this excel sheet where I note down all my buy/sell trades. And here’s what I figured out by doing a post mortem of my past trades from that sheet. There is a bit of hindsight bias here but we’ll just need to work with what we have.

Relaxo Footwears

I initially thought the stock will not do better than 15% returns per annum, and did not buy.

Big opportunity loss due to not averaging up. I was anchored to low valuations or my cost price perhaps.

Position sizing was not sufficient. Should have bought a lot more.

Nesco

Prematurely sold due to fear of losing out gains already made.

Did not apply second level thinking. Should have trusted management would fix the issue, because they would have solved the problem with their business sooner or later.

Kitex Garments

Should not have bought the stock in the first place. I wasn’t looking hard enough.

Averaging down did not help.

Should have sold when EPS fell down. Did not cut losses quickly enough.

Bajaj Finance

What worked – Buying when others were fearful.

What didn’t – Process gap. Not adhering to my stop loss.

Alkyl Amines

What worked – Experimental bet although it was outside my circle of competence.

What didn’t – Not following up. Not averaging up.

The way I look at it is, my journey has been through 3 phases.

Phase 1 – Where I was neither buying nor selling correctly Phase 2 – Where I was buying somewhat correctly but not selling correctly Phase 3 (Hoping I am in phase 3 today) – Where I am buying correctly [High allocation bets like Alembic Pharma (exited), Laurus & RACL have done well since March 2020] and hoping to sell correctly.

It is foolish to keep repeating mistakes and I now have pre-determined stop loss prices for all my long term bets and I am hoping this kind of a process allows me to convert paper profits into real currency. Having pre-determined stops also helps get rid a lot of bias and inaction that comes when the stop price actually arrives. I am hoping this helps me to transition from phase 2 to phase 3 smoothly unless I figure out there are more holes in my process.

Perhaps there is a phase 4 too, that I can’t visualise today. Having said that, I am glad to have made it this far, the future seems exciting and there’s a lot more yet to be accomplished.

Note to self:

Not backing up positions with enough capital, is a costly mistake. How many of your bets go right is less important than how much you allocate to the ones that go up. To quote Jeff Bezos, “Big winners pay for several failed experiments.” I seem to have fixed this mistake, by allocating 25% of my portfolio to Laurus Labs, last year.

Avoid slow or non-growth businesses altogether. Just doesn’t work for my investing personality type.

Not cutting losses quickly is a lacuna to be avoided.

Imagine you are a senior employee, at a company, with several years of experience and you know things are going like this.

By year 6, you know that the company’s equity has been wiped out and it goes into BIFR, a fancy name for potential bankruptcy proceedings.

Once it is clear that the chances of survival are almost zero, in most cases, employees are the first ones to flee a sinking ship because it is easier to switch to a different job than to go down with the ship. To understand the scale of losses incurred, there were no employees in this co. earning more than a lac a month, in year 6, at a time when it incurred a loss of 5.4 Crs.

In this context, I present to you the story of an entrepreneur who managed to save a business from dying. The above numbers are of RACL Geartech, an auto ancillary company that was about to go belly up in 2001 (Year 6). But, due to one employee and his team’s persistence, managed to survive.

A few years later, due to a stroke of good luck, he met a potential client (Kubota, a leading Japanese player in tractors) on a flight and convinced them to give a small order. And that resulted in a domino effect of being able to thrive in a sector that is famous for a lack of pricing power.

Turnaround was led by current promoter, Mr. Gursharan Singh

The company came out of BIFR in Nov 2007. And here’s how they’ve turned around a business that had almost gone to the grave.

Sales have grown at 12% between 2016 & 2021, despite Covid lockdown impact Profits have grown at 42% CAGR between 2016 & 2021

Higher margins were led by exports growing faster than lower margin domestic sales.

Higher exports also led to better returns on shareholders’ funds.

Clients

Most of the company’s growth has come from BMW, Kubota, KTM & Piaggio, which are all giants in their respective businesses.

Typically, in such situations, the supplier gets squeezed. But this is not what happened in RACL’s case, indicating there is something more to this business than being just an also-ran auto ancillary player.

What would a new entrant need in order to compete with RACL?

Moat # 1 – Peer Margins & ROE

I ran a screen to check which auto ancillary companies have the best margins in the industry. RACL is the only growing co. which showed high margins coupled with high ROE over the last 2 years. In an industry with low or no pricing power, high margins and high return on equity are good indicators of a presence of a sustainable advantage over competition. Why else would no other names show up on the list?

Moat # 2 – Technical know-how

Lets think about it. Why would multi-billion dollar companies let a tiny supplier like RACL make high margins and high ROE, when they might as well go to other auto-ancillary co’s and give them lower margins?

Thomas Phelps, in his wonderful book, 100 to one in the stock market, said “Know-how is a competition reducer. The longer it takes to learn how to do what your company is doing, the fewer competitors will be around to do it for less.”

And here’s what management said about technological know-how in their maiden concall in Feb 2021.

Basically, they were saying, employees at their manufacturing plants have built their skill set over several decades. Plus, the machinery is prohibitively expensive. Even if another ancillary co. does put up the money to buy costly machinery, they will need to go through a learning curve, which could take many years. The other option is to poach a ton of employees from RACL, which is less likely because a lot of RACL’s employees have been around for decades and seem to be quite loyal to the co. I speculate, this is perhaps because the co. went through potential bankruptcy at some point, and led to a closely knit team.

To a potential new entrant, this would be like a chicken and egg problem. “Do we spend a ton of money on the machinery first or do we poach employees first?” I am not saying a new entrant can’t accomplish that. I am saying chances are less. Another thing to note is that the count of employees has been more or less the same over many years, despite all the growth, which possibly indicates very few employees leaving the co. for better and potentially risky opportunities.

Moat # 3 – Plant location

This is from the book “The Unusual Billionaires”.

“In the 1980s, Maruti used to give its suppliers thirty days of notice for the components it needed. Now, it instructs the supplier the previous night about the specific two-hour slot the next day when the components have to reach Maruti’s assembly line. It takes a new entrant into the Indian auto market many years, sometimes decades, to create a supply chain as efficient as this. That’s the power of architecture— it brings different companies together into a common network with a common goal in mind.”

The supply chains of global customers are considered super-efficient. A BMW or a Kubota, would want their suppliers’ plants to be in and around their own plants. But that is not the case with RACL. Forget being close to the customer’s plants, their plants are not even close to the port. RACL’s plants are located around Delhi, which is hundreds of kilometres away from the nearest port. If large OEMs are okay with a gear vendor being located hundreds/thousands of miles away (which is reflected in RACL’s growth over the last few years), it tells us something about RACL’s competitive advantage. No?

Moat # 4 – The gears that RACL makes require very high precision

This is based on hearsay and from another video made by somebody I haven’t interacted with, and hence I don’t know the source. So, take it with a pinch of salt if you want to 🙂

In 2014, KTM decided to launch a bike by 2017. RACL was given orders in 2014 and they delivered parts the same year. Before launch, KTM planned to run a bike for 50,000 KMS. The part failed after 47,000 KMS. This led to a delay in launch by 6 months. So, instead of KTM saying, we’ll fix it as we go, they said, we will wait until RACL fixes the issue, which they eventually did a few months later. Given this level of clients’ focus on precision, a new entrant is likely to encounter several technical roadblocks, over several years, before he cracks a contract to make high precision gears for a BMW, a KTM, a Kubota or any other large player.

Risks

The buzz word in auto nowadays is electric vehicles. This is perceived as a major risk for auto ancillary companies. But is EV a real risk?

Imagine you are a European who aspires to buy a luxury bike that costs several thousand Euros. Even in Europe, most salaried folks, can’t afford such high-end bikes. If you’re spending a bomb on an expensive luxury bike, what are you more likely to consider? Would you even think about the fuel economy that the bike provides? Would you not prioritise style and power and thereby not even consider an electric bike? I would imagine, somebody who considers spending that kind of money would almost certainly not worry about whether the bike is electric or not.

That being said, consumer preferences can change faster than we expect and EV adoption would stay a key aspect to track while staying invested in this co.

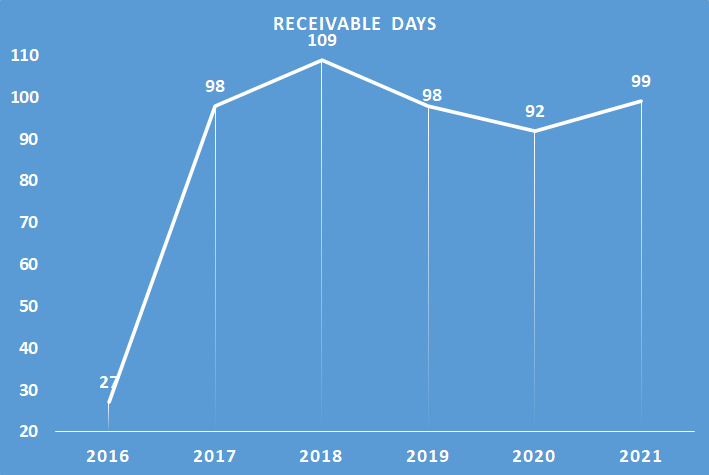

Another risk is that of high receivable days. RACL’s receivable days have trended in the range of 90-110 days, over the last 5 years, up from 27 days in 2016. Although 3+ months is a long time to recover cash from their clients, the good thing is that the trend has been flat, since 2017.

As per management, one of the reasons for receivables being high is that their plants are not located close to the port and that adds 15 days to the number. The usual number for exports is in the range of 60-70 days.

Typically, when receivables are high, businesses have trouble converting profits into cash. However, that is not the case here. RACL has been comfortably converting it’s reported profits to cash. Had receivables been taking a toll on the business, we would see much shorter orange bars, in the below graph.

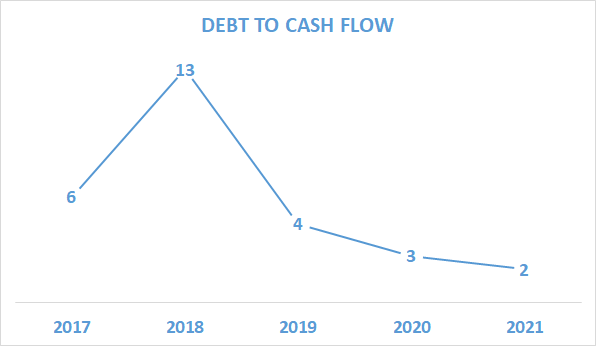

Addendum – I missed to add a key risk yesterday. Debt to Equity is on the higher side and is another risk to this business’ future prospects. Also, the co. plans to take on more debt to fund Capex in the next year or so and one will need to watch how well the co. is able to monetize the additional capacity they will be putting up, most of it using debt.

The icing on the cake is that current debt is equal to 2 years of FY 2021 cash flows and has been trending downwards. I don’t expect the co. to pare down debt in the next few years, given the huge growth expected. The only case where I foresee debt being reduced is either, when future cash flows are better than expected or the management decides to increase equity by issuing new shares (Equity Dilution).

Scalability

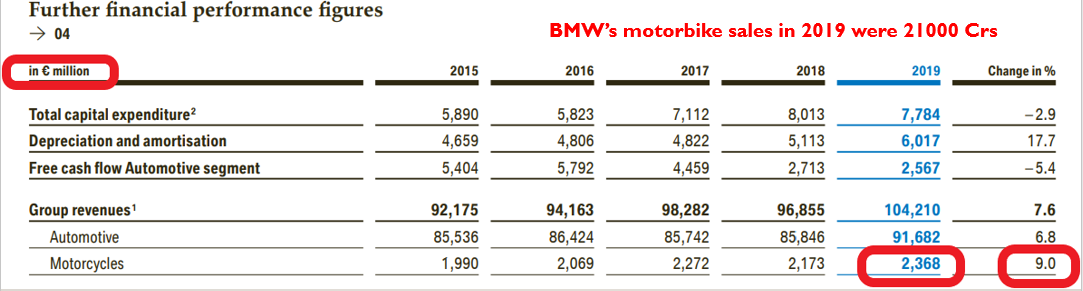

RACL has several multi-billion dollar clients. BMW, for example, sold bikes worth 21000 Crs in 2019. And RACL’s annual sales is a paltry 1% of BMW’s. And this is just from one client. Will RACL be able to scale up their business multi-fold across geographies and across clients? Time will tell.

Another interesting thing that happened was that Kubota recently did a JV with Escorts and despite Escorts being the local partner did not bring in their own gear manufacturer. Instead the Japanese partner, Kubota, roped in their supplier, RACL. This is important because RACL’s big client is taking them along, into whatever newer markets they are going into. This opens up a very wide range of possibilities for RACL.

Capacity expansion during an industry down cycle

The co. announced Capex worth 50 Crs in FY2020 AGM. This is at a time, when their fixed assets were 100 odd Crs. Why would a co. that sells non-compulsory goods, increase capacity by 50% during a pandemic? It is not like they are selling roti, kapda, makaan, or anything close to that.

I think it is because they have high visibility for future orders, from clients, which is why they are taking such a huge risk of putting up 50 Crs, that too, 3/4th of it through debt.

Valuation

When it comes to valuation, the best thing one can do is to keep things simple, instead of using fancy excel models. I like to compare the earnings growth rate to P/E and here’s how it looks.

RACL vs Nifty

RACL

Nifty

EPS growth – 5 years

37%

9%

P/E

14

29

RACL compares well to Nifty and most other indices in terms of earnings growth as well as it’s valuation.

Disclosure – I have a position in this company and my views are certainly biased. This blog is not to be construed as an investment advice. Please consult your investment advisor before investing.

Disclaimer: This is NOT investment buy/sell/hold advise. I am not SEBI registered. May change stance on above business anytime with new developments and/or new insights, and/or overall market conditions. May NOT be able to update periodically. Please do your own diligence and/or take professional advise, before investing.

I have high regards for Peter Lynch’s investing wisdom. His investment track record was one of the best, of his era. An important thing that is most often missed, is that he achieved a 29% return over 11 years, despite having a big big handicap of not being able to invest more than 5% in his highest conviction bets, due to prevailing mutual fund rules, at that time.

And he was an investor who advised not owning more than 5 stocks in a DIY individual investor’s portfolio. Had the rules allowed him to back up the truck, to say 20% of Fidelity Magellan, chances are, he would have outperformed his peers by an even better margin.

Here’s what he wrote about his highest conviction bet, in the early 90’s.

“During my final three years at Magellan, XXXX was the biggest position in the fund—half a billion dollars’ worth. Other Fidelity funds also loaded up on XXXX. Between the stock and the warrants (options to buy more shares at a certain price), Fidelity and its clients made more than $1 billion in profits on XXXX in the 1980s. This was the year I backed up the truck. Backing up the truck is a technical Wall Street term for buying as many shares as you can afford. Now 4 percent of Magellan’s assets were invested in XXXX, and toward the end of the year I reached my 5 percent limit. It was my largest position by far.“

I’ll reveal the name shortly. Just stay with me.

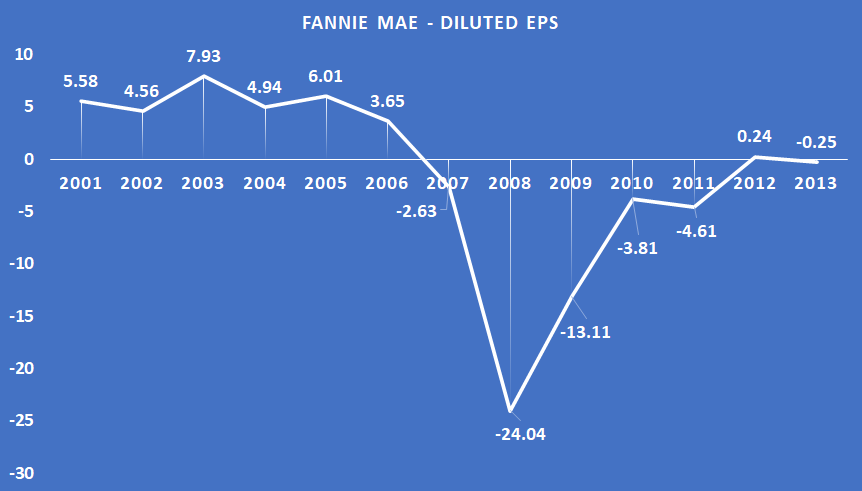

These kind of returns happened, because the company’s earnings per share grew at 18% CAGR over 15 years, from 50 cents in 1986 to $5.60 in 2001. Btw, he called this the best business in America. And, this came from an investor who compared it to thousands of other American businesses.

And yet, he seems to have lost money on this 27 bagger. The stock was that of Fannie Mae, which was the American equivalent of HDFC Home Loans in India. In a Sep 2008 article published in the Wall Street Journal, Lynch was expecting the beaten down Fannie Mae’s business to bounce back by 2011. By the time this article was written, Fannie Mae’s stock price was already down from a peak of $86 in 2001 to $2 in 2008.

WSJ article published in Sep 2008

But then, just like with most hope based investing situations, Fannie Mae’s diluted EPS never recovered post GFC, and so did it’s stock price.

Whether or not he ever sold his Fannie Mae position eventually, is not known. If an experienced investor as smart as Peter Lynch did not sell a winning position in time, it tells us how difficult endowment bias can make it for us to sell our ex-winners.

That led me to thinking what if he had sold his position much earlier, when the company’s growth had slowed down? Fannie Mae had not been doing well since 2003 anyway, as seen from their blue EPS chart above. Assuming he was holding a big position in Fannie Mae from 2003 to 2008, he would have saved a fortune by getting out of the stock once the company’s business had slowed down, say by 2006 itself, much before the price tanked all the way.

Now let me tell you a story of somebody who did not make the same mistake as Peter Lynch, and sold Pantaloons because the price had started tanking. He’d started buying Pantaloons at ₹7. The stock went up all the way to ₹ 875 and then when it came to ₹300, he sold the stock, a price it never went back to, ever again. Below, he explains his rationale.

What if I had stuck to selling at pre-determined stop loss prices, in the past?

Well I used to be this “buy and hold and forget” investor a couple of years back. But not any longer.

I’d started buying Kitex Garments at 500 levels in Oct 2016 (not adjusted for splits) and then averaged down at 400 levels too. It is easy to hide under the garb of “buy and hold” despite the market giving you enough signals that you are wrong. Here’s what I had written in my trading journal, in Feb 2018, at a time when I should have been selling.

The same pattern has repeated for me in stocks like Bajaj Finance, Manappuram Finance, etc. and when I should have been selling these stocks, I didn’t – A mistake I am almost certain, not to repeat in the future. I now have a process wherein I set pre-determined alerts for stocks that I own. This takes out a lot of bias, when trying to cut losses quickly. So if and when the price of stock goes down below that level, I force myself to sell. Sometimes, it makes sense to think Mr. Market is smarter than you, control your risks and protect your limited capital.

Unknown Unknowns

Thinking about it, such a strategy could potentially protect my portfolio, from potential black swans in the future, such as the world wide web going down all at once, or a nuclear attack or a bio attack, another pandemic that is way deadlier than we are experiencing today or the US dollar blowing up or some freakin’ unknown unknown that nobody ever anticipated to begin with. I really hope none of these scenarios ever materialize but one can never know.

My own experience has been that problems in companies come from areas nobody anticipates. From 2014 to 2018, I had been invested in Nesco, the company that owns the lucrative Bombay Exhibition Center and a couple of IT buildings, which it leases out to MNCs. The problem eventually came from their exhibitions causing several hour long traffic jams outside the Bombay Exhibition Center. The problem was compounded by the fact that there was metro rail construction (an unknown unknown that no research analyst had anticipated) going on at the Western Express Highway and I got rattled out of my position despite having held the stock for 4 years. You could blame this failure on a lack of my thinking about second order effects. What I did not foresee was that when their kingdom was at stake, the management would use its contacts and all its liquid resources to resolve the problem quickly with the Bombay City Corporation.

The other unknown that nobody anticipated for this otherwise foolproof business was Covid19. Not one analyst had predicted that a pandemic would put off returns for some this company’s oldest shareholders, by a few years, resulting in huge opportunity costs.

And here’s what Morgan Housel wrote about unknown unknowns in The Psychology of Money “Beyond the predictable struggles of running a startup, here are a few issues we’ve dealt with among our portfolio companies: Water pipes broke, flooding and ruining a company’s office. A company’s office was broken into three times. A company was kicked out of its manufacturing plant. A store was shut down after a customer called the health department because she didn’t like that another customer brought a dog inside. A CEO’s email was spoofed in the middle of a fundraise that required all of his attention. A founder had a mental breakdown. Several of these events were existential to the company’s future. But none were foreseeable, because none had previously happened to the CEOs dealing with these problems—or anyone else they knew, for that matter. It was unchartered territory.Avoiding these kinds of unknown risks is, almost by definition, impossible. You can’t prepare for what you can’t envision.“

Some more anecdotal evidence

Here’s what Mark Minervini wrote in one of the Market Wizards books – “Were there any other major pivotal points in your transition from failure to success? After I had been trading for several years following my initial wipeout in the markets, I decided to do an analysis of all my trades. I was particularly interested in seeing what happened to stocks after I sold them. When I was stopped out of a stock, did it continue to go lower, or did it rebound? When I took profits on a stock, did it continue to go higher? I got tremendous information out of that study. My most important discovery was that I was holding on to my losing positions too long. After seeing the preliminary results, I checked what would have happened if I had capped all my losses at 10 percent. I was shocked by the results: that simple rule would have increased my profits by 70 percent.”

To conclude, this article is not to question a very smart investor’s wisdom but to understand how difficult investing in stocks, particularly selling, can really be, at times. And more importantly, how critical it is to cut your losses quickly rather than slowly. The difference between both can be night and day.

Remember the market cliché about some of the best track records coming from those of dead people’s inactive portfolios? This comes from a supposed study that was done by Fidelity, in which they noted an internal performance review on accounts to determine which type of investors received the best returns between 2003 and 2013. The customer account audit revealed that the best investors were either dead or had forgotten about their portfolios.

From Business Insider

This happens because emotions and opportunity costs are not a factor in dormant portfolios. Does that mean, one should not try to maximize returns from one’s portfolio by switching to better ideas? I don’t think that would be the perfect thing to do, considering the dormant portfolio data. I’ll tell you why. Imagine you were an investor in Wipro in Feb 2000 and somebody told you about inactive portfolios doing better than the active ones and based on that you’d decided not to sell. You’d have had 20 years of zero returns while the indices ran up multi-fold.

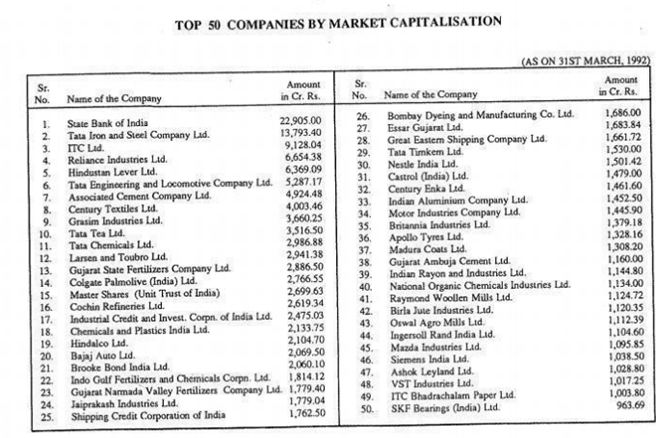

Very few companies survive the relentless onslaught of competition, technology, changing consumer preferences, changing government regulations and various other factors. See for example, the below list of top 50 companies by market capitalization in 1992.

Most of the above got replaced by better, sexier, smarter companies. And, most of the ones that did survive in today’s top 50, did so because of issuing new shares. Take State Bank of India for example. From a market cap of 22900 Crs in 1992 to 318,000 Crs today, SBI’s market cap grew at a pitiful 9.5% CAGR. I am not even getting into equity dilution which would chop shareholder returns down to much lower single digits.

Or take ITC, a much debated hot stock. ITC’s market cap went from 9000 Crs to 2.6 Lac Crs, delivering a return of 12% CAGR, excluding dividends. That ITC would grow at a faster clip, 2021 onward, when it is 28x bigger, and is likely to be much more bureaucratic than it was in 1992, will possibly become a case study in hope based “long-term” investing, in the future.

Going back to 1992, as investors who believed in the India growth story, and who wanted to maximize their ROI, why would we have stayed invested in SBI/ITC when there were much better fish in the pond, provided one knew where to look? Shouldn’t we have been looking for faster growing high ROE companies, than the below large caps?

Company

1992

2021

CAGR (excluding dividends,dilution,spin-offs)

State Bank of India

22905

318787

10%

Tata Iron & Steel

13793

86385

7%

ITC

9128

259594

12%

Reliance Industries

6654

1310616

20%

HUL

6369

544606

17%

Tata Engineering & Locomotive

5287

N/A

N/A

Associated Cement

4924

N/A

N/A

Century Textiles

4003

5225

1%

Grasim Industries

3660

92495

12%

Tata Tea

3516

N/A

N/A

Tata Chemicals

2986

18958

7%

Larsen & Toubro

2941

196339

16%

Gujarat State Fertilizers Company

2886

N/A

N/A

Colgate Palmolive

2766

41860

10%

Master Shares (Unit Trust of India)

2699

N/A

N/A

Cochin Refineries

2619

N/A

N/A

Industrial Credit and Investment Corporation of India (ICICI)

2475

N/A

N/A

Chemical and Plastics India

2133

N/A

N/A

Hindalco

2104

73500

13%

Bajaj Auto

2069

104174

14%

Brooke Bond India

2060

N/A

N/A

Indo Gulf Fertilizers and Chemicals Corp

1814

N/A

N/A

Gujarat Narmada Valley Fertilizers & Chemicals

1779

4456

3%

Jaiprakash Industries

1779

N/A

N/A

Shipping Credit Corporation of India

1762

N/A

N/A

Bombay Dyeing

1686

1468

0%

Essar Gujarat

1683

N/A

N/A

Great Eastern Shipping Company

1661

4513

4%

Tata Timkem

1530

9447

6%

Nestle India

1501

159778

17%

Castrol India

1479

12166

8%

Century Enka

1461