Let me just start by saying that my views are positively biased because I have stayed invested in this company since much lower levels.

This post is an attempt to articulate what I have learnt so far, about Indian Pharma.

We have all read recent news reports about the Chinese government cutting power to polluting factories in certain areas. These power supply cuts mean that the factories operating out of such provinces will have lesser capacity to produce goods and operate at a much lesser scale.

This change could mean that if Chinese manufacturers are unable to produce as much chemicals or APIs (active pharmaceutical ingredient) or Key Starting Materials, as before, there would be a shortage of these products across countries. This could possibly lead to higher prices of these products for whoever is able to make them and thereby result in increasing sales and margins. These manufacturers could be from China, India, Timbaktu or anywhere else.

In our case, it could either be beneficial or not, depending upon which side of disruption, the companies that we are invested in, are on.

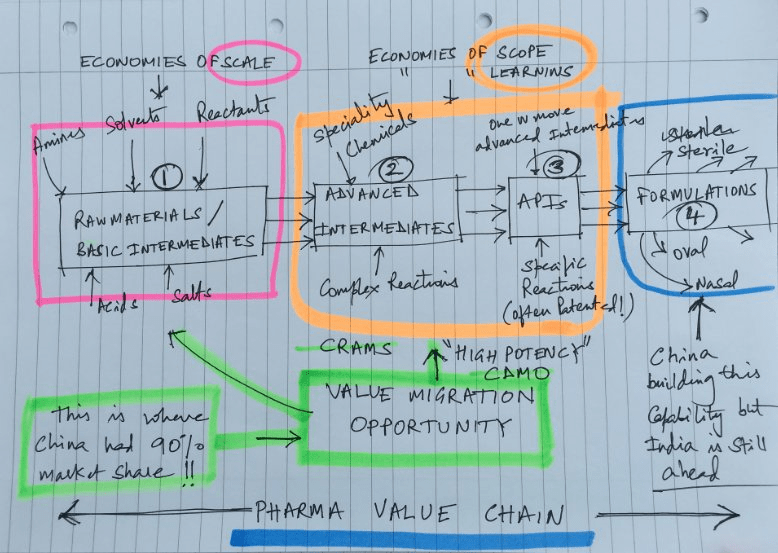

What are Key Starting Materials (KSM)?

The textbook definition of KSMs – Critical input used in the manufacturing of an essential generic medicine, as well as ingredients or components that possess unique attributes essential in assessing the safety and effectiveness of such essential generic medicines, including excipients and inactive ingredients.

From what I have understood so far, KSMs include stuff like Amines, Solvents, Reactants, Acids & Salts. Maybe there are things beyond this too.

With this background, let’s define the problem now. Raw material supplies for Pharmaceutical companies are likely to get hit and these shortages will lead to spikes in input costs.

Question – Who will be impacted negatively and who will be impacted positively, by this change?

There are certain products where Indian API manufacturers are completely dependent on China for APIs and KSMs. For instance, fermentation-based products like anti biotics, statins, vitamins etc. These players may see cost escalations in input costs of fermentation based products and some of them will pass it on to their end customers over time. Conversely, Pharma players without pricing power won’t be able to pass on these increased costs and their margins will get negatively impacted.

Since I am interested in Laurus Labs, I was worried about this angle and decided to deep dive.

What will happen if Laurus Labs is not able to pass on these price increases to their customers?

Here’s what I found.

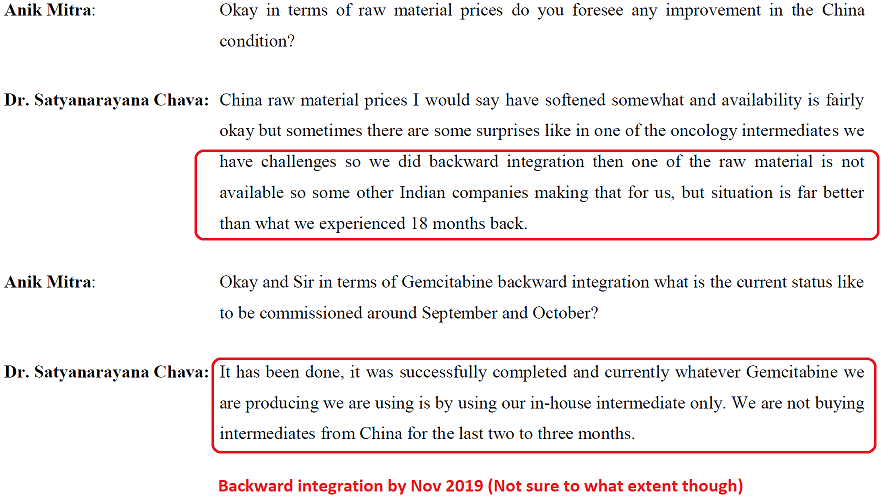

This China problem is not new. It keeps cropping up every once in a while. They had a similar issue in 2019 as well.

And here’s how they handled it.

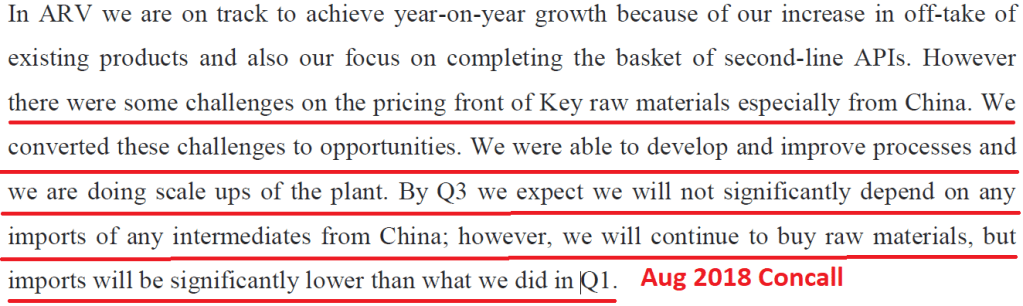

Let’s go back another year now. The year is 2018 and they were having the same troubles. Prices of key raw materials had gone up and Laurus was able to convert a challenge into an opportunity.

Based on the above events, one gets a gut feel that even if there are challenges in the supply chain, here’s a team that can do things, to resolve the issue.

Now let’s look at the situation from the vantage points of various stakeholders involved.

The Chinese factory owner: Last week it was the pollution control officers. This week it is the damn power cuts. How am I gonna pay my bills? How am I to pay salaries to all those people working on the shop floor? I am not sure how long I can sustain in this business.

The Indian Entrepreneur: There’s a plant closing down in China. I am sure there are opportunities out there for me to go out and grab, and thereby grow my business. While that happens, my margins could take a hit and let me keep my eye on the ball and focus on the long term.

The Customer: Everything was going so well and then thanks to all the polluting factories, I need to find another skilled guy in another business friendly geography where my supplies are guaranteed with equal or perhaps better quality.

Mr. Market: He is swinging in between what will happen in the next quarter and what will happen over the long term. On days when he is worried about the next quarter, he offloads his stake. And on days when he is focused on the long term economics of the business, he thinks “This China + 1 thing is real after all. More and more business could fall into this company’s lap. Let me just hold on to this business. Better yet, let me increase my stake in this business.”

Let’s look at some disconfirming evidence too. Below is one instance wherein they were unable to pass on price increases to their customers.

That being said, here are my conclusions.

- Equity investing is not a science. Sometimes, we just need to stomach the volatility, the uncertainty & the self-doubt that accompanies falling stock prices. Particularly so, if the entrepreneur has a decent, execution track record.

- Disruption in APIs isn’t new. It’s been there for a couple of years and is here to stay. And entrepreneurs who have handled it successfully before, could possibly handle it well in the future too.

- What Mr. Market perceives as disruption, is perceived by the entrepreneur as an opportunity. There are times when blind belief in the entrepreneur is foolhardy. Yet there are times, when you need to go with your gut feel and just trust that the jockey will make things right.

You don’t want to be that guy who calculates too much and thinks too little.

Disclaimer: I have been wrong with my thesis in the past and could be wrong this time or in the future too. These are my thoughts today and could change as and when the situation evolves or whenever disconfirming evidence presents itself.

Barath Mukhi

11-Oct-2021

Thank you Barath for your thoughts.

Even I believe that the current market reaction and resulting sharp correction in Laurus doesn’t make sense.

Perhaps this is to be used as an opportunity to load up more at relatively lower levels.

Nothing has changed in terms of fundamentals – staunch/proven promoter credentials, diversification of business into high growth areas (non-ARV, Synthesis, Laurus Bio etc), aggressive targets to grow the topline over next couple years, massive capex underway etc.

However, when you see even senior/experienced investors like Hitesh Patel (Valuepickr forum) being heavily bearish on a stock like this, it does make one question the conviction 🙂

I guess part of the conundrum is perceived opportunity cost of staying put in Laurus and sitting through this volatility versus deploying the capital towards benefiting from the on-going sector rotation in this bull market. For example would it make sense to exit Laurus and deploy capital into, maybe, Union Bank (any PSU or even auto-ancillary like Pricol) and POSSIBLY make money over few quarters and come back to Laurus at a more lower level when it has bottomed out. This is akin to trying to time the market I guess. At the end of the day this is a call each individual has to take for him/herself.

Do let me know if you have any additional thoughts on this from the above perspective.

LikeLike

Hey Avishek,

I exited around 560 levels on Friday because I was uncomfortable with the way Laurus’ price was moving and it hit my stop loss. I set stop losses for all my long term holdings because while we should be willing to hold a stock for long periods of time, we should be wary of unknown unknowns too and for me stop losses take care of that problem, at least partly.

For example, nobody knows for sure, how long prices of KSMs are going to keep rising. It depends on the whims are fancies of the chinese government, with multiple potential layers of bureaucracy in between. In such a scenario with so many unknowns, being able to predict which way the profits of the company will swing is a big question mark. I don’t bother with stop losses when I am absolutely certain about the company’s future prospects. However, even if there is an iota of doubt, I put in stop losses because I don’t want a profitable position to turn into a dud because of an inability to decide at a critical moment.

William O’Neil, the inventor of the CANSLIM investing system, said this in the book “How to make money in stocks” – “Selling decisions, however, are made mostly by looking at the charts. If you wait for the fundamentals to become poor, you will often sell late.”

Markets discount the future precisely more often than not. Take the example of HEG in 2018. The stock corrected by close to 25%+ after Sep 2018 results. And this was despite the fact that Dec 2018 results were still very good. Yet the markets didn’t care because participants were predicting bad results 2 quarters down the line, well in advance.

When a sector goes out of favor, (API sector in this case) it is sometimes a safe course to not play the smart Charlie in town and step aside and let the market take its own course because when a sector goes out of favor, the bad news just doesn’t stop coming.

These are my views and I could very well be wrong about my sell call on Friday. If I turn out to be wrong, I’ll be okay to humbly accept the market’s verdict and be comfortable to get back into the stock at much higher levels, provided I still feel that the story is still intact, So, one needs to take his/her own call depending upon one’s own investment framework.

LikeLike

Now that the results are out and company has given explanation about the relatively lacklustre performance while also mentioning longer term growth trajectory and revenue targets remain unchanged, what’s your view?

I feel stock will see price pressure at least for 2-3 quarters but if management is able to deliver as per stated projections/plans, this is still a good business to hold over the longer term.

LikeLike

I would wait for the numbers to show up before jumping back in.

This could mean getting back in at a higher price than I sold and I am perfectly okay with that, because the style of investing I follow involves being in companies that keep showing growth and if I stay invested I ignore opportunity costs. I might as well get into something more promising.

If the investing style you follow, involves averaging down in companies that are facing temporary problems and if you are confident that Laurus’ management will walk the talk, then hold on or perhaps even add more. Even now Laurus might be a good stock for a long-term investor but it is still an overpriced stock for someone with a short/medium-term view.

Generally speaking, while averaging down, we need to know the business in & out + the business needs to be one with very few moving parts. If we are averaging down, we need to know we are playing with fire and we better be very very sure about that the business in question will deliver as expected.

Coming to longer term growth projections, management has given a guidance of 7400 Crs of revenue by 2023. This works out to 27% CAGR topline between today and March 2023. Mathematically speaking, if they don’t deliver 27% growth, the number increases to higher than 27% every quarter. And history shows very few companies deliver consistent growth of 20% plus. Laurus may well be an exception and until that happens, I wouldn’t think so.

LikeLike

Thanks for sharing your thoughts!

Makes sense.

For now, I am wanting to give the management some leeway until at least Q1 FY23 to see how it plays out before taking a sell decision. My investment horizon (if thesis plays out – even if they can achieve ~18-20% CAGR of topline growth), is certainly longer term until there are clear signals of persistent degrowth.

Laurus is about 11% of my portfolio (not heavily concentrated, yet not minuscule allocation either) but I am willing to soldier on for two quarters at least.

Caveat: if the situation worsens or there are early indicators over next few months of a more persistent problem, I might pull out.

LikeLike

astonishing! Details Emerge on [Developing Story] 2025 wonderful

LikeLike