There’s this German company that makes a key component for automotive, aerospace, and industrial uses. The company initiated a restructuring program in Sep 2020. Due to rising costs, management wanted to reduce headcount & manufacturing capacity in Germany.

Here’s the press release from the company in Sep 2020.

Now, if we were to read between the lines, a big chunk of these jobs and production capacities would be moved elsewhere.

How do we know where these jobs are moving to? One, by reading between the lines and two with some data. First, let’s see what the management of the Indian listed entity of the same group, is saying.

So the Indian co. is saying, they will grow their exports but cannot reveal, at what rate. My guess is they either don’t have a go ahead from the parent due to geo-political reasons or perhaps it is an evolving situation and they don’t know themselves, what their German bosses have in mind.

Now let’s move to the data. A rising export trend, indicates that management is walking the talk and business is indeed moving to India and could be an indicator of things to come.

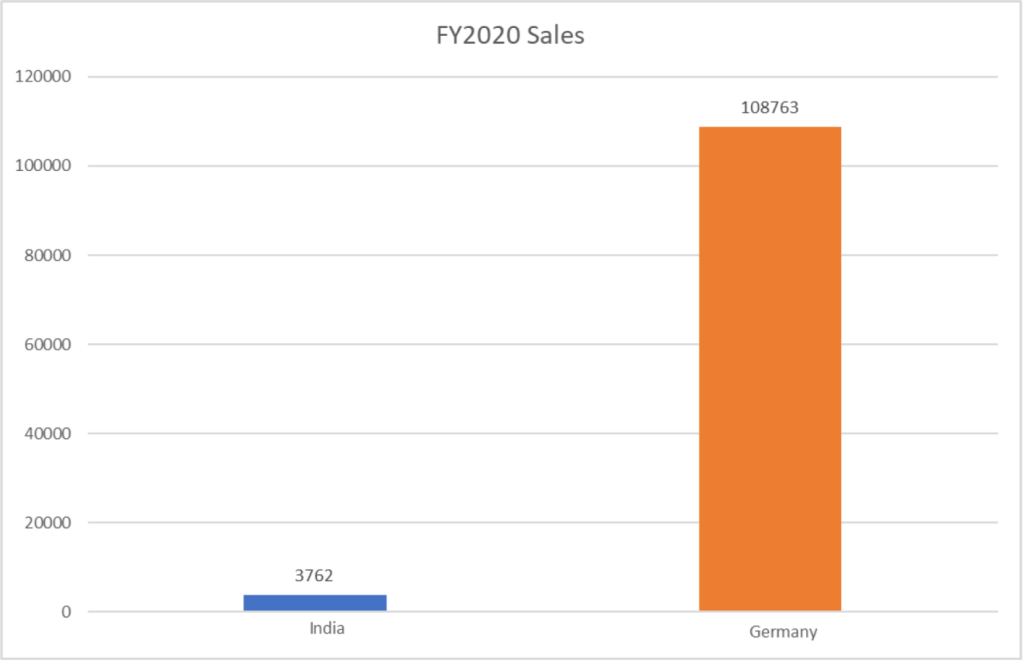

Now let’s look at, what sales look like for the German parent and for the Indian entity.

The German group’s worldwide sales are 29 times that of the Indian entity’s 3762 Crs, last year and that means there is a lot of room for growth here and scalability is not likely to be an issue.

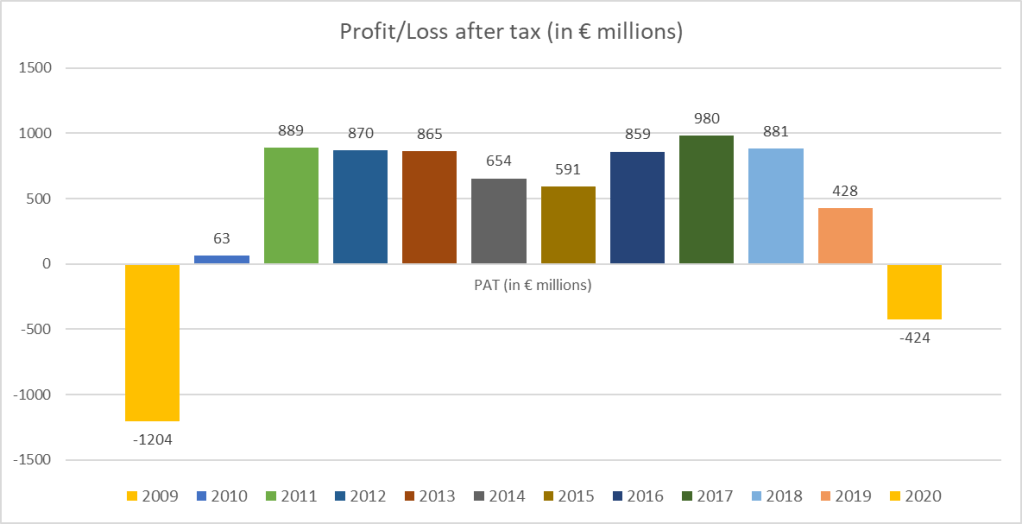

Now, this is not a company that is struggling to sell its products. It is a company which is trying to cut costs and move jobs to lower cost locations such as our very own. In fact, it is an seven decade old company which holds a significant global market share in the segment in which it operates.

Risks

- Plants are operating at full capacity and future growth relies on Capex. Current fixed assets = 1000 Crs. Capex for next 3 years = 1200 Crs.

- German politicians are already doing everything they can to retain jobs within their geographies. As of today, cost economics are winning over politics and business is moving to India. This may or may not turn out to be the case, in the future.

- Margins drop due to fluctuation in raw material prices. Although margins have stayed relatively stable for the company in the past, there is no guarantee that they will be able to pass on commodity price risks over to their customers in the future and remains a key risk for investors.

At the time of this writing, the business trades at 50 times earnings. For a business where things can change quickly, does it make sense to value the business based on a P/E multiple?

I’ll leave you with that thought.

Disclaimer: Invested in the Indian co. from lower levels. These are my views and are not to be construed as investment advice. As always, please do your own research before proceeding to buy/sell/hold.

Barath Mukhi

5th Jan 2022

No…PE would be misleading here . But Barath, the 14 EU plants(12 in Germany) , do they account for all the sales of the german entity ? Are there other factories besides those 14 ?

LikeLike

That is an unknown. What is known is that they have 43 plants in Europe and 10 R&D centers. How much of that comes to the Indian entity remains to be seen.

LikeLiked by 1 person