I have high regards for Peter Lynch’s investing wisdom. His investment track record was one of the best, of his era. An important thing that is most often missed, is that he achieved a 29% return over 11 years, despite having a big big handicap of not being able to invest more than 5% in his highest conviction bets, due to prevailing mutual fund rules, at that time.

And he was an investor who advised not owning more than 5 stocks in a DIY individual investor’s portfolio. Had the rules allowed him to back up the truck, to say 20% of Fidelity Magellan, chances are, he would have outperformed his peers by an even better margin.

Here’s what he wrote about his highest conviction bet, in the early 90’s.

“During my final three years at Magellan, XXXX was the biggest position in the fund—half a billion dollars’ worth. Other Fidelity funds also loaded up on XXXX. Between the stock and the warrants (options to buy more shares at a certain price), Fidelity and its clients made more than $1 billion in profits on XXXX in the 1980s. This was the year I backed up the truck. Backing up the truck is a technical Wall Street term for buying as many shares as you can afford. Now 4 percent of Magellan’s assets were invested in XXXX, and toward the end of the year I reached my 5 percent limit. It was my largest position by far.“

I’ll reveal the name shortly. Just stay with me.

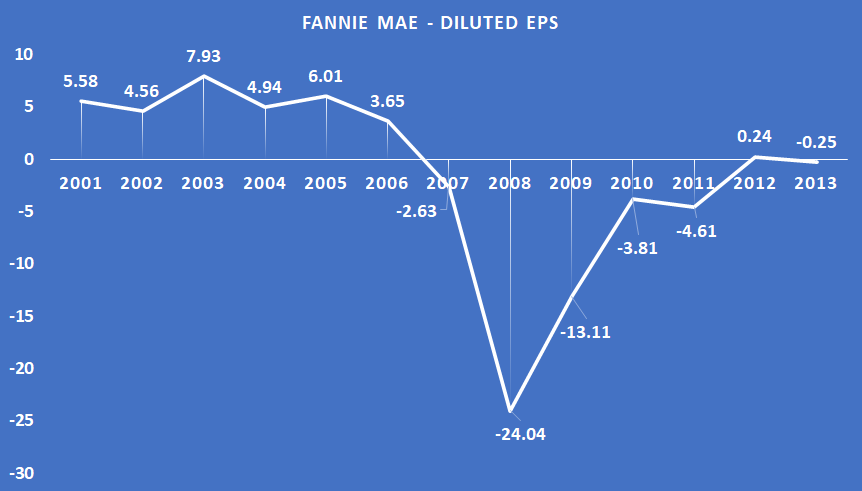

These kind of returns happened, because the company’s earnings per share grew at 18% CAGR over 15 years, from 50 cents in 1986 to $5.60 in 2001. Btw, he called this the best business in America. And, this came from an investor who compared it to thousands of other American businesses.

And yet, he seems to have lost money on this 27 bagger. The stock was that of Fannie Mae, which was the American equivalent of HDFC Home Loans in India. In a Sep 2008 article published in the Wall Street Journal, Lynch was expecting the beaten down Fannie Mae’s business to bounce back by 2011. By the time this article was written, Fannie Mae’s stock price was already down from a peak of $86 in 2001 to $2 in 2008.

But then, just like with most hope based investing situations, Fannie Mae’s diluted EPS never recovered post GFC, and so did it’s stock price.

Whether or not he ever sold his Fannie Mae position eventually, is not known. If an experienced investor as smart as Peter Lynch did not sell a winning position in time, it tells us how difficult endowment bias can make it for us to sell our ex-winners.

That led me to thinking what if he had sold his position much earlier, when the company’s growth had slowed down? Fannie Mae had not been doing well since 2003 anyway, as seen from their blue EPS chart above. Assuming he was holding a big position in Fannie Mae from 2003 to 2008, he would have saved a fortune by getting out of the stock once the company’s business had slowed down, say by 2006 itself, much before the price tanked all the way.

Now let me tell you a story of somebody who did not make the same mistake as Peter Lynch, and sold Pantaloons because the price had started tanking. He’d started buying Pantaloons at ₹7. The stock went up all the way to ₹ 875 and then when it came to ₹300, he sold the stock, a price it never went back to, ever again. Below, he explains his rationale.

What if I had stuck to selling at pre-determined stop loss prices, in the past?

Well I used to be this “buy and hold and forget” investor a couple of years back. But not any longer.

I’d started buying Kitex Garments at 500 levels in Oct 2016 (not adjusted for splits) and then averaged down at 400 levels too. It is easy to hide under the garb of “buy and hold” despite the market giving you enough signals that you are wrong. Here’s what I had written in my trading journal, in Feb 2018, at a time when I should have been selling.

The same pattern has repeated for me in stocks like Bajaj Finance, Manappuram Finance, etc. and when I should have been selling these stocks, I didn’t – A mistake I am almost certain, not to repeat in the future. I now have a process wherein I set pre-determined alerts for stocks that I own. This takes out a lot of bias, when trying to cut losses quickly. So if and when the price of stock goes down below that level, I force myself to sell. Sometimes, it makes sense to think Mr. Market is smarter than you, control your risks and protect your limited capital.

Unknown Unknowns

Thinking about it, such a strategy could potentially protect my portfolio, from potential black swans in the future, such as the world wide web going down all at once, or a nuclear attack or a bio attack, another pandemic that is way deadlier than we are experiencing today or the US dollar blowing up or some freakin’ unknown unknown that nobody ever anticipated to begin with. I really hope none of these scenarios ever materialize but one can never know.

My own experience has been that problems in companies come from areas nobody anticipates. From 2014 to 2018, I had been invested in Nesco, the company that owns the lucrative Bombay Exhibition Center and a couple of IT buildings, which it leases out to MNCs. The problem eventually came from their exhibitions causing several hour long traffic jams outside the Bombay Exhibition Center. The problem was compounded by the fact that there was metro rail construction (an unknown unknown that no research analyst had anticipated) going on at the Western Express Highway and I got rattled out of my position despite having held the stock for 4 years. You could blame this failure on a lack of my thinking about second order effects. What I did not foresee was that when their kingdom was at stake, the management would use its contacts and all its liquid resources to resolve the problem quickly with the Bombay City Corporation.

The other unknown that nobody anticipated for this otherwise foolproof business was Covid19. Not one analyst had predicted that a pandemic would put off returns for some this company’s oldest shareholders, by a few years, resulting in huge opportunity costs.

And here’s what Morgan Housel wrote about unknown unknowns in The Psychology of Money “Beyond the predictable struggles of running a startup, here are a few issues we’ve dealt with among our portfolio companies: Water pipes broke, flooding and ruining a company’s office. A company’s office was broken into three times. A company was kicked out of its manufacturing plant. A store was shut down after a customer called the health department because she didn’t like that another customer brought a dog inside. A CEO’s email was spoofed in the middle of a fundraise that required all of his attention. A founder had a mental breakdown. Several of these events were existential to the company’s future. But none were foreseeable, because none had previously happened to the CEOs dealing with these problems—or anyone else they knew, for that matter. It was unchartered territory. Avoiding these kinds of unknown risks is, almost by definition, impossible. You can’t prepare for what you can’t envision.“

Some more anecdotal evidence

Here’s what Mark Minervini wrote in one of the Market Wizards books – “Were there any other major pivotal points in your transition from failure to success? After I had been trading for several years following my initial wipeout in the markets, I decided to do an analysis of all my trades. I was particularly interested in seeing what happened to stocks after I sold them. When I was stopped out of a stock, did it continue to go lower, or did it rebound? When I took profits on a stock, did it continue to go higher? I got tremendous information out of that study. My most important discovery was that I was holding on to my losing positions too long. After seeing the preliminary results, I checked what would have happened if I had capped all my losses at 10 percent. I was shocked by the results: that simple rule would have increased my profits by 70 percent.”

To conclude, this article is not to question a very smart investor’s wisdom but to understand how difficult investing in stocks, particularly selling, can really be, at times. And more importantly, how critical it is to cut your losses quickly rather than slowly. The difference between both can be night and day.

Barath Mukhi

30-May-2021

One thought on “Why is selling more difficult than buying stocks?”