On 29th May, 2020, LT Foods showed up on my screen, because it had reported a good set of numbers.

3 other items caught my attention.

Sales had grown by 20% while PAT had grown by 167%

Branded business (Daawat Basmati Rice) had done well

Debt to EBITDA had reduced from 4x in FY19 to 2.9x in FY2020

Company presentation

Another important thing to note was that, unlike other sectors, production had not been affected much despite the Covid lockdown because the company’s products fall under the essential commodities category.

News article

By the time I read this article, the stock price had already gone up from ₹24 to ₹26, a jump of 8%. What caught my fancy though, was the fact that a branded business was now available at 4 PE whereas it’s competitor, KRBL (India Gate Basmati Rice Brand) was available at double the valuation. Since I was reading the news on a Friday evening, I had the weekend to think about whether I should buy this stock on Monday morning.

Time for some scuttlebutt

Next I remembered, one of my close friends knows a contact who happens to be a big distributor of another brand of Basmati rice. So through my friend, I contacted this distributor and the feedback I received was that exports of Basmati rice to countries like Iran, are likely to be affected this year due to logistical challenges.

In the end, I felt the risk reward equation was favorable, given that the stock was selling cheap (compared to KRBL as well compared to the PE it which it has historically traded at), and allocated 10% of my portfolio to this stock on 1st June, 2020 at ₹26. Fast forward to today and I am sitting on gains of 60%+ (The current stock price is ₹42). Worked out to be a good trade!

When to sell?

This is no high quality business and was a pure opportunistic play. My plan is to ride the stock as long as it continues going up and exit once it goes to ₹35 or less.

I know I might get a lot of brickbats from the NBFC bulls for writing this post. Anyway, this post is an attempt to capture what I have been thinking while exiting NBFCs during the crisis. I acknowledge that my exit call may be proven wrong in the future and looking at this post, a few years down the line, people might think wow this guy got scared out of his NBFC stock holdings.

Or they may say, wow that was a good call, in the middle of a crisis. We’ll see how this plays out.

So here’s what Ben Graham, the famed role model, once said.

Notice that he puts safety of principal before an adequate return. He did not put an adequate return first. So, let’s explore how this applies to the ongoing Covid19 situation and how it concerns NBFCs (and should concern their investors). Are NBFC investors really putting safety of principal before an adequate return? Or are they prioritizing returns over potential risks that are hiding behind the curtains?

So, before the Coronavirus situation started, I was invested in 2 NBFCs, one was a popular multibagger stock and another was a lender whose loans were secured by the yellow metal. I will not be taking company names for obvious reasons and leave it to the reader to guess what those names are. I will be addressing the first company as the unsecured lender and the second as the secured lender.

Cutting losses quickly vs Staying invested for the long term is a paradox every value investor runs into, at some point in their investing journey. But what makes this game interesting is exactly this dilemma.

So here are the thoughts that came to my mind before I exited these 2 stocks.

Reasons for exiting the unsecured lender’s stock

Macro analysis is not my forte. My circle of competence lies in picking quality growth stocks at reasonable prices and I should stick to that. By investing in an NBFC or by continuing to stay invested in an NBFC today, I am becoming a macro analyzer and by definition, straying outside my circle of competence. More on this further down in the blog.

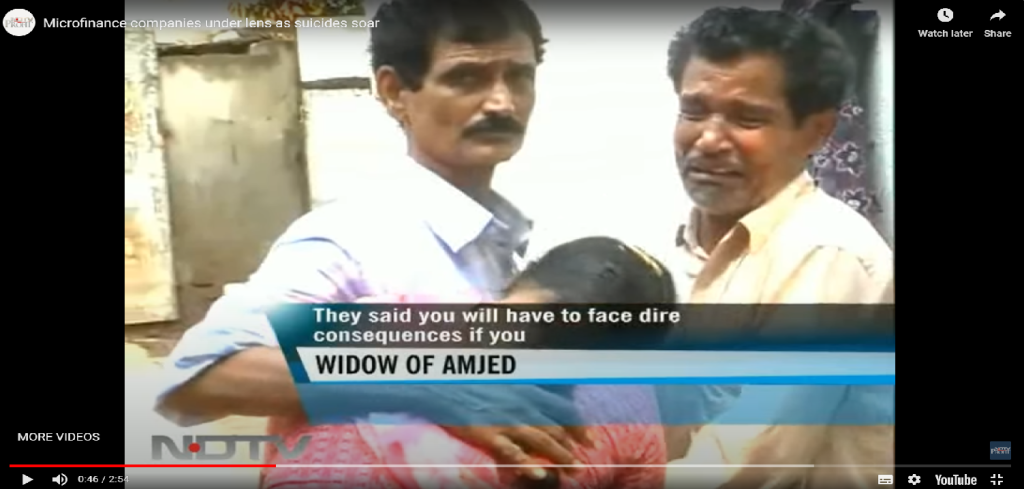

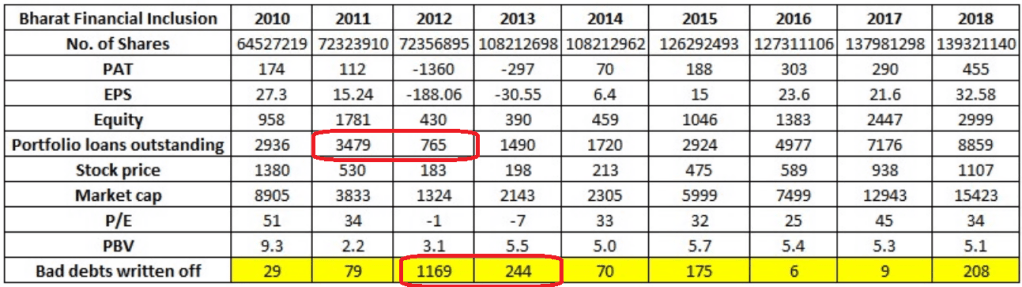

We all know what happened to SKS microfinance (subsequently renamed Bharat Financial Inclusion) when Andhra’s politicians stepped in to pass a law to protect their vote bank from loan sharks, back in 2010. Will history repeat itself and will the government intervene again and tell lenders, boss you are not going to use hard tactics to recover your bad loans. What happens to those low NPA numbers then? What happens when shit hits the ceiling? Nobody knows. And here’s what happened to SKS Microfinance and it’s continuing shareholders when a crisis happened. I realize this is not THE perfect example but what the heck, that’s the best correlation I can think of.

So here’s how the SKS MFI story played out back in 2010-11.

SKS were an aggressive but successful MFI lending company. They had grown their loan portfolio at a phenomenal 150% between 2007 & 2010 and PAT at a staggering 250% !! The unsecured lender I was invested in, had high growth rates as well, but not nearly as high as those of SKS.

Looking at their scorching growth, other MFI players entered the Andhra Pradesh MFI market.

Next, bad lending and recovery practices became the new normal, for both borrowers and MFI lenders.

What happens when you lend without checks and balances is your borrowers start defaulting and in Andhra this took a turn for the worse. Due to hard handed recovery tactics, some of their borrowers committed suicides.

Next came the politicians who wanted to obviously protect their vote banks. Some of them might have had good intentions of protecting borrowers from loan sharks, but the crux of the story is that the AP govt. subsequently passed a law which halted operations of MFIs in the state, adversely impacting lenders’ recovery and liquidity.

And as a consequence of this law, out of the total 3500 Crs of loans that SKS had lent in 2011, they had to write off 1400 Crs or 40% of their total loan book.

Climax – The company’s equity shrank by 78%, from 1780 Crs in 2011 to 390 Crs in 2013. This led to the company’s stock price never coming back to the high of 1380, that it had touched in 2010, even until 2018 when the company was taken over by Indus Ind Bank. And this was despite the fact that SKS’ was trading at a princely PBV multiple of 5 in 2018. This was also despite a string of sustained growth in sales and profits between 2014 & 2018. Eight years and the stock was still below it’s pre-crisis high. WTF!!

Will bad behavior drive out the good, yet again? How will bad borrowers influence the good borrowers in the case of the unsecured lender I was invested in? In 2010, the total number of MFI related suicides in Andhra was reported to be between 50 & 60. Can 50-60 borrowers on their own, cause an MFI to lose 1400 Crs. Mathematically speaking, no. Because the average ticket size of each MFI borrower was just a few thousand rupees. But the psychological impact of these suicides was devastating for SKS, the bad loan borrowers, the good loan borrowers, the politicians and all other stakeholders in that ecosystem, and rightly so. After all, the SKS management team might have looked the other way, when their goons were out there, in those villages, harassing their borrowers.

What kind of an impact will the moratorium have on the unsecured lender’s borrowers’ psyche? Nobody knows. Will some of them think, not paying EMIs is the new normal? Will the moratorium be extended beyond the current 6 months? Who will bear the interest costs during the moratorium period? The borrower or the lender or the lender’s lender aka we the investors? Some folks are already disputing the logic of interest getting accrued during the moratorium period.

Next, I come to opportunity costs and cutting losses quickly. By staying invested in the unsecured lender, I was ignoring the opportunity costs of investing in other companies. At one point NBFCs had tailwinds and so I invested in 2 of those. Today, they don’t have tailwinds or at least it looks like that. So shouldn’t I be moving my money to a sector like Pharma or Specialty chemicals where I can foresee growth. Isn’t growth a core component of the GARP investing style? And if these lending companies aren’t promising me growth, why should I continue holding them? Buy and Hold does not mean Buy and Forget. It means Buy and Monitor and most importantly, act, and cut losses quickly when the time comes. As Ian Cassel put it beautifully, fall in love with companies that execute, but be prepared to divorce quickly.

I am not the proprietor of this lending company. I am a minority shareholder. And as a minority shareholder I have the advantage to move my money to a business/sector with better prospects over the next 3-4-5 years. Why would I even want to give up this advantage? As Lord Keynes had once said “When facts change, I change my mind. What do you do, Sir?” And there’s no denying that the world has changed for lenders.

Now, coming to the “somewhat secured” lender’s balance sheet. The first table shows their share of secured and unsecured loans. And the second table shows the potential downside in a case wherein, their unsecured loans go bad by 20, 30, 40 & 50%. For example, SKS had bad loans to the tune of 40% of their loan book. If such a thing happens to this secured lenders’ balance sheet, then the potential downside could be in the range of 54% or more, depending upon Mr. Market’s mood swings.

The other thing that could happen is that the MFI subsidiary will be forced to declare bankruptcy with no support from the parent and is non recourse to the parent co. This would mean business as usual for the secured lending part of the parent’s business. What would be the financial and psychological implications of such a move from the company? How will Mr. Market treat the parent for orphaning his MFI child? Will the parent’s borrowing costs go up because his kid defaulted? I don’t know the answer to this and it’s difficult to even make an educated guess, I suppose.

Another point noteworthy is that, back when the SKS crisis happened, MFIs were NOT regulated by RBI. Today, they are. So we don’t know how RBI will step in to save the MFI industry.

Subjective vs Objective probabilities

Objective probabilities are those which stay constant regardless of the external environment.

Subjective probabilities, on the other hand, are those which depend upon the probability that something will occur.

Let’s take NPA numbers of these NBFCs for example. In the past, both the secured and the unsecured lending companies, kept reporting a very good set of low NPA numbers. Now some investors might have assumed these to be objective numbers. But were they? They were subject to the following dependencies-

The overall economy doing well.

A subset of this was the rural economy had to do well for the secured lender’s MFI business to do well.

And since a big chunk of the rural economy depends on agriculture which, in turn depends on monsoons, the rain gods become another factor as well.

For their Vehicle Finance and SME lending business to do well, India’s GDP needed to keep growing at 5-6-7%. In the absence of growth, boy there are problems in an economy. Go check out the period when America’s GDP kept shrinking after the 1929 stock market crash and the subsequent recession. GDP Growth is like oxygen. It’s presence is barely noticed and it’s absence is sorely missed, as some unsecured lenders may learn, over the next few years, if not quarters.

Do we know how long borrowers will be out of their jobs or for how long borrowers’ businesses are going to be down? No. By staying invested in this lending company we are assuming it’s borrowers will be back up, on their feet, in the next 4-6-8 quarters.

Are we also assuming once borrowers’ incomes are back to pre-crisis levels, they will start paying back their loans immediately, leaving aside other priorities they might have deferred during the lockdown, such as paying their children’s school fees, getting their sore tooth removed, fixing their leaking roofs, taking a small vacation or whatever else. In the pre-crisis era, these same people had been programmed to borrow, to meet their requirements. But now that the lender has locked his wallet, in a safe, what will these borrowers do, in order to meet their needs and wants?

How many of these companies’ borrowers will lose jobs? How many borrowers will close their businesses, for good? How many of those closed businesses are big ticket borrowers?

As you can see, when you think NPAs, there are so many moving parts, that making an educated guess could well be a fool’s errand. NPAs are not objective probabilities, they are subjective. Subject to the factors stated above, among so many other things.

Next, I explore what happens to shareholders’ psyche during market crashes.

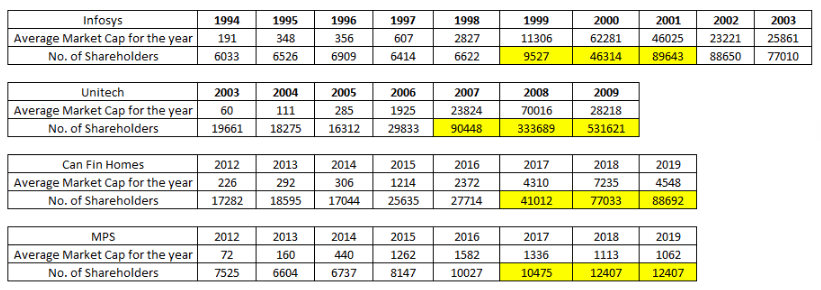

I think it’s lies in our sub conscious nature to catch falling knives. Here’ what the data says and as Sherlock Holmes says, it’s an error to argue against data.

As we can see, the number of shareholders almost always goes up when a sector leader falls. Even after these companies’ glorious days were over and their market caps were decreasing, the number of new shareholders kept increasing. Like everything else in the stock market, there will be exceptions to this rule. But generally speaking, this pattern plays out. So we should watch out and not fall in the trap called Anchoring bias. Could the number of shareholders increase in these 2 NBFC sector leaders in their FY20 annual reports? If I had to bet, I would say yes, this pattern is likely to be seen in NBFC annual reports for FY20 as well.

Fear of Missing Out and What if I go wrong with this bearish view that I have?

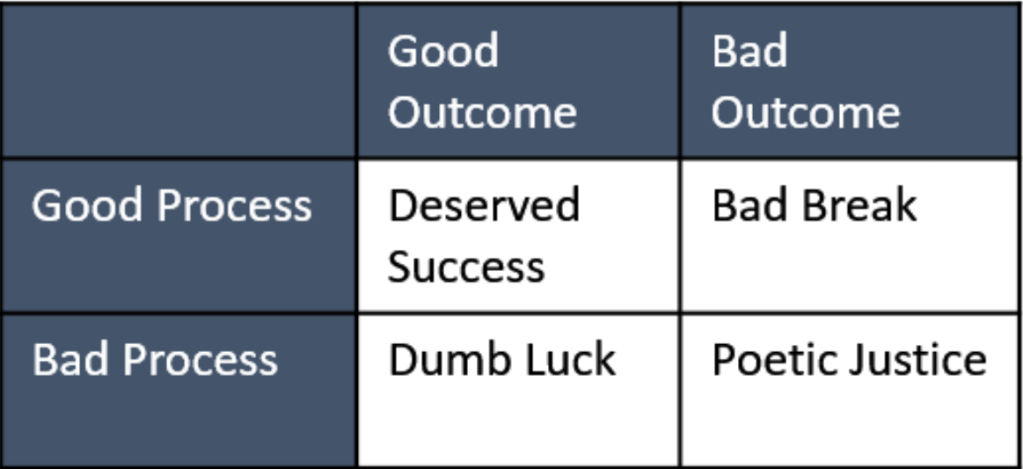

If the process of buying or selling is good, eventual outcomes will be good. In other words, I should be worried about whether or not my process is good and not what my clients will be thinking, should my sell decision go wrong and the stock price starts moving up after I sell. My duty is to have a good process, such that the outcome takes care of itself. Occasionally, a good process will result in a bad break and as a fund manager I am okay to accept a bad break, provided, the process of buying/selling was good. Should I be worried, that I will lose out on potential gains that could come from continuing to hold onto the stock? Yes that worry is real. But it comes with risks attached, that I do not want to take with mine and my clients’ money.

With that being said, I am ready for the brickbats from NBFC bulls. There’s no messenger of bad news, who doesn’t get trolled after all.

Every crisis brings with it, changes, and some of those changes spell OPPORTUNITY. Of course, not all opportunities pan out the way we intend them to. But what if we manage to ride one such opportunity and manage to benefit from it.

This is my first attempt to understand a Pharma business and I started deep diving only after the Covid19 situation started evolving, since I thought it might be a good idea to expose my clients’ portfolios to fast growing companies from an industry which is basically, recession proof. It would be fair to say I am quite new to this industry and have been trying to understand a very complex business. On the other hand, from my interactions with several value investors, over the years, Pharma as a sector, is a black box in a lot of value investors’ minds, due to the complexity involved, and that exactly, makes it a bias worth exploiting.

The purpose of this post is to be able to come back a few years later, do a post-mortem and understand what worked and what didn’t. My views are biased and what follows is, how I look at the situation today. My opinions could change rapidly, depending upon how internal and external factors play out over time.

On 21st March, Donald Trump tweeted this.

There are quite a few listed companies that produce Hydroxychloroquine & Azithromycin. So here’s what differentiates Alembic Pharmaceuticals, a company that I started investing in, in Sep 2019. My initial reason for buying was the company was growing well, was run by a fantastic management team and the price was attractive, given the growth numbers.

What the company sells..

What are Generics / Generic Drugs?

Generic drugs have a similar chemical composition as branded drugs. They are accepted globally and are of the same quality with a lesser cost as compared to branded drugs. Along with no compromise on quality, they are also cost-effective as the cost of R&D and drug discovery is not included in the case of generic drugs.

Generic drug manufacturers like Alembic fall in the latter category because they help reduce prices of essential drugs vs companies like Valeant Pharmaceuticals which work to increase prices. We all know what happened to Valeant and some of it’s very savvy investors, a few years ago.

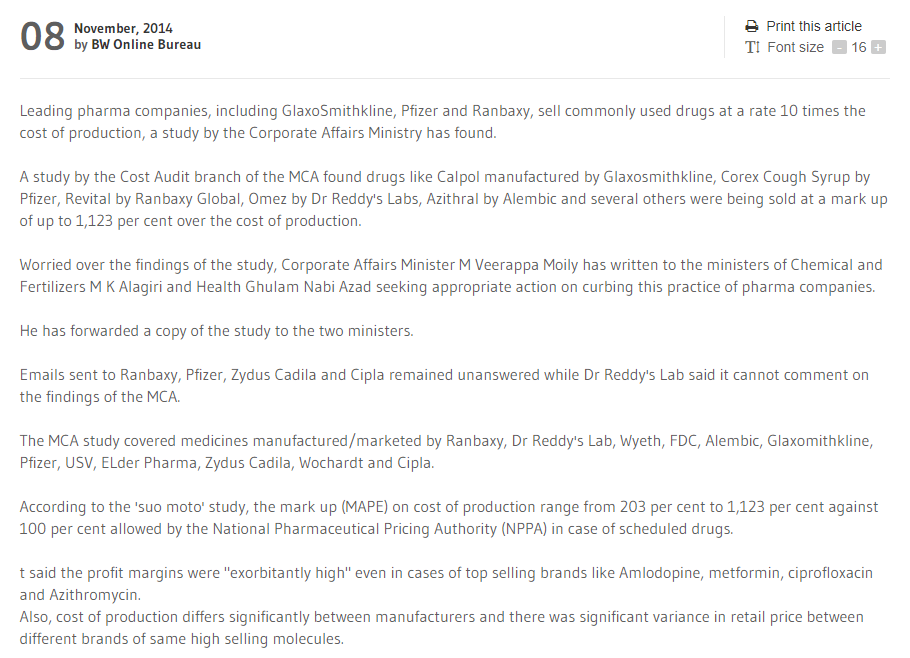

Below is an old news article that shows staggering price differences between Generic & Branded drugs

An old article shows Pharma Firms Sell Common Drugs At 10 Times The Cost: MCA

And here’s what happens when a company creates win-win situations for itself and it’s customers, by selling drugs at a fraction of the prices that branded drugs sell at. The company wins by increased sales and customers are happy to buy the same unbranded drugs at unbelievably low prices.

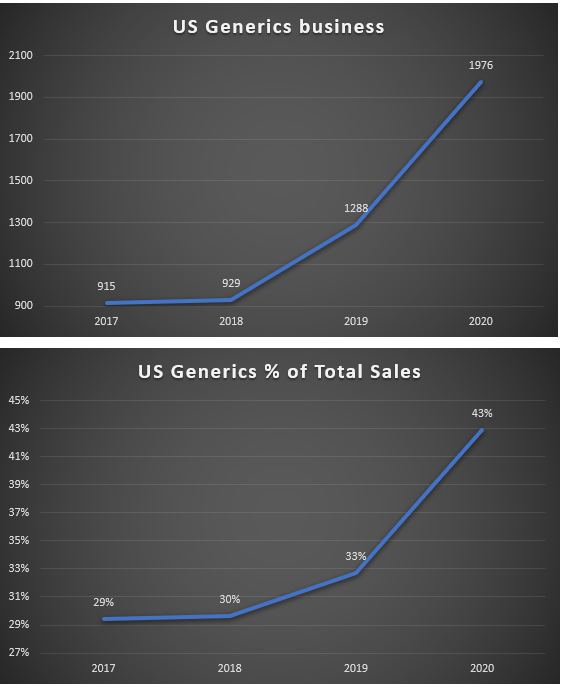

Contribution of US Generics business to Alembic’s overall sales is increasing

Branded drugs – A company develops a drug over several years, secures approvals from FDA or equivalent regulatory bodies, secures patents for it and then milks the cow. Medical patents typically last for 17-20 years after which other companies are legally allowed to manufacture the same drug using the same ingredients. Since the company manufacturing the generic drug, has not incurred R&D and related costs, it sells the drug at a fraction of the branded drug’s prices.

API Business

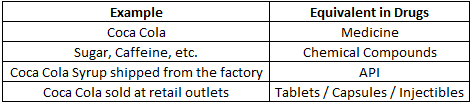

API (Active Pharmaceutical Ingredient) means the active ingredient which is contained in a drug. API and raw materials are often confused due to similar usage of the two terms. An API is not made by only one reaction from the raw materials but rather it becomes an API via several chemical compounds. In layman terms, Medicines are composed of APIs, and APIs, in turn, are composed of raw materials that go through various manufacturing processes before they turn into APIs. To give you an analogy, let’s take Coca Cola.

Peter Lynch once said “When there’s a war going on, don’t buy the companies that are doing the fighting; buy the companies that sell the bullets.” In the current context of war against the virus, one can equate APIs with bullets being used to fight the war against Coronavirus. Effectively, Alembic is fighting the war (through their Azithromycin drug) as well as supplying the bullets (APIs) to MNCs like Pfizer.

Icing on the cake – Azithromycin shortage in the USA& other countries

As per the US FDA website, there has been continuous shortage for Azithromycin all the way until 8th May, 2020 and the shortage continues as of the time of writing this blog. Only 3 companies out of 10, seem to be in a position, to supply the drug. And because, Alembic manufactures the API as well as the end product, it seems to be better placed to continue supplying the drug vs it’s competitors.

Alembic has the capacity to manufacture 10 Crore tablets a month. Retail price in the USA is between ₹120 & ₹174 per tablet. This price does not exclude retailer / distributor’s margins and how much of an upside this situation brings for Alembic, is hence open for debate. I believe there could be significant upside from this opportunity for the company, this year, and leave it to your judgement as to how much of an upside there is.

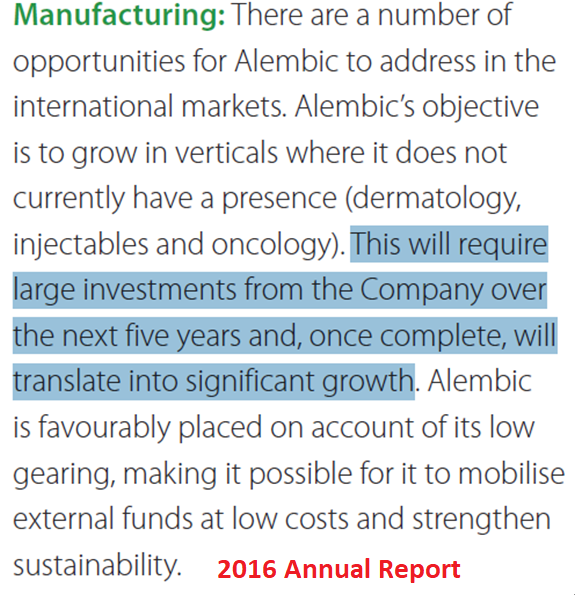

Capacity expansion

The company has been investing a good chunk into expanding their production capacity and this should take care of the next leg of growth for the company. The company’s balance sheet shows Capital work in progress has grown by 17x between 2016 & 2020. Sales has grown by 1.5x during the same period.

Potential to increase sales per rupee of assets, from 1.4 in FY2020 to a higher number, once the company starts monetizing the R&D & Capex spends it has done over the last 3-4 years

There is no denying that the company is capitalizing some of it’s R&D and related costs. On the other hand, the purpose of the above graph is to roughly understand what kind of an upside potential there could be. Before the company started expanding capacity in 2016, it used to have sales of ₹4 for every ₹ of Fixed assets and CWIP. Even if we were to assume, the company moves to ₹2.5 of sales for every ₹ of fixed assets and CWIP, coupled with increased assets in the future, from the current ₹1.4, the upside could be significant.

Earnings quality check

In FY2020, Alembic earned a return on equity of 26% after incurring high R&D expenses. While ROE can be used to measure a company’s efficiency, it is also my hunch (based on number crunching several fraud cases), that companies with 20%+ ROE in some industries are less likely to give us things to worry about vs the ones with lower ROEs. Barring exceptional cases, companies with ROEs above 20% and high cash flows are less likely to result in permanent loss of capital for minority shareholders. In most cases where there are corporate governance issues, you’ll either find low ROEs or low cash flows as compared to PAT. This is a shortcut that I use to filter companies quickly.

What are a few things that can kill this idea?

Exporter risk – Early in March 2020, the government of India, banned exports of APIs and some basic chemicals. If the situation changes, and exports are banned again, for reasons (unknown-unknowns) that we can’t anticipate, this would adversely impact the company.

Infection risk at plants – At least 2 other pharma companies have reported several of their employees got infected, recently, possibly at work.

Pricing power risk – The company may not end up being able to pass on the increase in API costs or other raw materials to it’s customers. We will need to wait and see how this plays out over the next few quarters. This risk also applies to their generics business. Other generics players producing the same drugs may result in margin erosion for the company.

For example, data from an article from the US FDA site states, higher the number of generic players, lower the drug prices.

So if the branded drug sells at ₹100 and there is just 1 generics player, then the generic drug would sell at ₹61. However, if there are 6 Generics players, then the generic drug gets sold at an abysmal 5 bucks.

Other risks include Macro risks due to uncertainty around Covid19, Opportunity cost risk, Logistics / Raw material risks & Dilution / Leverage risk (The company has been growing faster than the ROE it delivers)

Valuation

Why investors are likely to pay top dollar for pharma companies in the near future?

The markets hate uncertainty and given the current uncertainty around earnings prospects of most companies, one sector that is recession proof is Pharma. This is because, no matter how the Covid situation impacts the economy or no matter how long it takes scientists to develop a vaccine, patients are not going to reduce consuming medicines. For example, I looked up sales numbers for pharma companies between 2008 & 2010 and a majority of pharma companies’ sales went up, although every other sector was hit by a recession. I believe it is reasonable to assume that pharma companies (and other sectors with good earnings visibility) will see better valuations in the near future, compared to sectors which have low or no earnings visibility, such as Oil, NBFCs, Real Estate or Auto, etc. Moreover, if lockdowns are extended or reintroduced, Pharma companies are less likely to have a production impact since they serve an essential human need which cannot be deferred to a future date. Unlike most other industries, there is no concept of pent up demand in the essential drugs business and patients cannot postpone consuming drugs to a later date.

Scarcity of high growth companies in the current environment is likely to drive up valuations for the ones that promise growth in tough times. Some investors may perceive 17-18 PE as expensive but I disagree with that notion, and believe we should buy growth and not PE. For example, in 2009, Page Industries’ stock was selling at 17-18 PE at some point and some people considered it expensive and fell into the statistical cheapness trap. They ignored the fact that Page had grown revenues at 45% CAGR between 1996 & 2009 and PAT had grown at 68% CAGR between 2005 & 2009. We all know the outstanding returns it subsequently delivered for the ones who looked at growth instead of PE.

In his wonderful blog on VST industries, Prof. Bakshi mentioned this

I believe, at my buying price, this would apply to Alembic too. At 17-18x TTM reported earnings, for a company with high R&D exp and one that’s rapidly growing, the downside looks limited, whereas there is option value embedded in the stock in the form of an upside from the Azithromycin opportunity as well as the other approvals that the company hasn’t monetized yet. In other words, I may be wrong on how much upside there is from the Azithromycin situation, but I don’t think I have paid too much for the growth I anticipate from it. My average buying price is a little less than 700 bucks, which is marginally higher than, what the market was pricing this company’s stock before the Azithromycin opportunity knocked the company’s doors.

If the Azithromycinsituation plays out as I expect, then it’ll result in a significant growth in earnings for the company.

If it doesn’t play out, then there is a high chance the company might still continue to grow well, as it has demonstrated over the last few years.

Besides, economic earnings are higher than reported earnings because the company spends a fortune on R&D. A high R&D expense shows that the management is willing to forego immediate benefits, in order to ensure future growth and has the deferred gratification gene. The management team mentioned they are looking at 700+ Crores R&D Exp in FY2021, on their latest concall & this increased R&D Exp is in a year where most other sectors are announcing layoffs, cost cutting measures, etc.

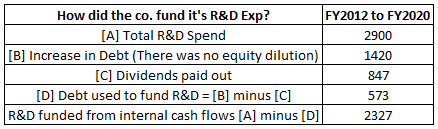

How did the company fund it’s massive R&D program?

The company spent a total of 2900 Crs on R&D between 2012 & 2020. In the same period, their debt increased by 1420 Crs. Out of this 1420 Crs, 847 Crs were paid out to shareholders as Dividends. So these guys went to the bank, borrowed 1420 Crs from the bank and out of this 1420 Cr loan that they took, they passed on 850 Crs to Shareholders as dividends. So that left them with 573 Crs which they could now use to fund some portion of their R&D. So, this means the company funded 2300 Crs or 80% of it’s R&D exp from cash flows that the business generated and 573 Crs or JUST 20% of R&D from debt. Was it funded by diluting equity? No, because no new shares were issued. So that leaves us with the only other source of funding which is Cash Flow from Operations. So 80% of their R&D exp was generated by cash that the business generated.

The co. funded 80% of R&D Exp from internal cash flows and 20% from debt

The outcome of all this R&D expenditure can be seen in the new approvals that the company receives from the US FDA.

Some folks I spoke to, raised concerns about high R&D expenses (investments?) by the company. Lets think about what happens when, a company has a lot of approvals.

By securing more approvals with potentially huge payoffs, the company gets more exposed to positive black swans. A case in point would be Alembic’s opportunistic plays at 3 different times. Alembic,

benefited from the opportunity in Abilify drug back in 2016 or thereabouts

is benefiting from the ongoing opportunity in Sartans drugs in 2018 (expected to last until Dec 2020 or beyond)

has the potential to benefit from the ongoing opportunity in Azithromycin in 2020

Was it a case that company got lucky thrice or was it because the company had so many approved products / approvals in place, which ensured they were (almost) exclusive sellers of 3 products that were in solid demand? Were they thinking “Heads I win big, tails I don’t lose much”?

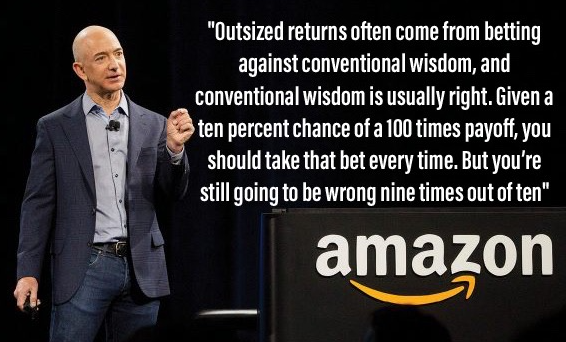

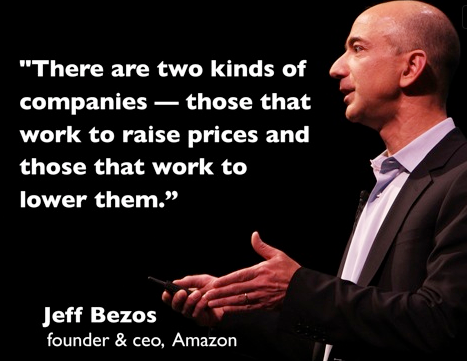

In my view, Alembic seems to be taking the approach outlined by Jeff Bezos – Given a 10% chance of a 100 times payoff, you should take that bet every time.

Here’s what somebody somebody wrote about ANDA filings elsewhere. And this is one hell of a way, to think about the big number of ANDA filings this company has, in comparison to other companies of similar sizes.

I personally think of filing ANDAs as Making Dices which the pharma company gets to roll once. If you roll and you get “6”, you get a windfall. If you roll the dice and get “4” or “5”, you get a reasonable amount. If you roll the dice and get “1” or “2” or “3”, you get nothing. The more dices you manufacture, the more number of times which you can possibly roll. There is a role of luck, but for that to happen you have to have a dice in your hand. And possibly as many dices as you can. Abilify was one of the dices which alembic rolled and luckily got a “6”. With the money from this, Alembic is now manufacturing many more dices . We don’t know which dice in future would be a jackpot, but what we know is that Alembic is surely producing many more dices to roll in future.

From the book – 100 to 1 in the Stock Market by Thomas Phelps

Imagine Nifty was a single company. Which of the following companies is likely to have better prospects?

Here’s a good way to think about High R&D expenses. From Prof. Bakshi’s Relaxo lecture.

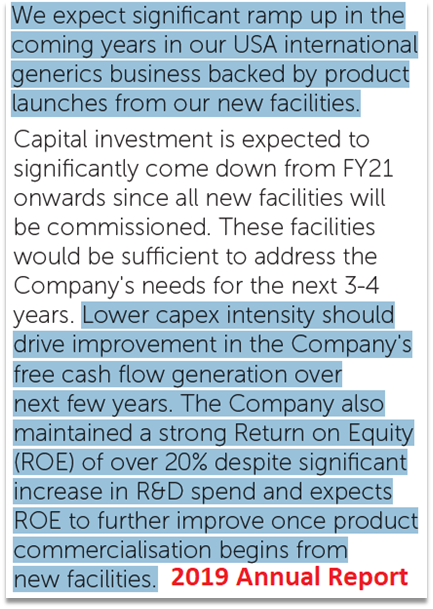

As stated earlier, Alembic earned a return on equity of 26% after incurring high R&D expenses in FY20. And here are the managements’ thoughts on R&D exp, ROE and Free Cash Flows in the next few years.

Addendum – Writing about some questions I was seeking answers to – 26th May, 2020

Why are margins high?

The company’s FY19 annual report states – “A good supply chain helps protect margins and also provides us with some room to improve our pricing.” I believe the reasons for higher margins could be the company’s supply chain + their US front-end marketing team + some pricing power due to the Sartans issue.

With this I conclude my investment thesis on the company.

Disclosure – I and my clients have substantial positions in this company and my views are certainly biased. This blog is not to be construed as an investment advice. Please consult your investment advisor before investing.

Disclaimer: This is NOT investment buy/sell/hold advise. I am not SEBI registered. May change stance on above business anytime with new developments and/or new insights, and/or overall market conditions. May NOT be able to update periodically. Please do your own diligence and/or take professional advise, before investing.

This is Barath and what follows is my first blog post. I am an investor based out of Bangalore and have been investing in Indian stock markets since 2010.

In the below post, I am gonna share how I have been thinking about investing during this whole Corona Virus situation, this little devil, that has brought the entire planet, down on it’s knees, at least temporarily.

The all-important question, that practically nobody has an answer to – Now that the Indian markets have fallen by 30%+ the question on my clients’ minds is whether to –

Wait for things to settle down and buy at the bottom (Neither sell nor buy stocks)

Subset of option 1 – Sell everything today and buy again at the bottom

Buy on the way down (Average down)

I’ll now list the thoughts that have been coming to my mind over the last month or so based on all the things I’ve read about this small thing that has choked the world.

Arguments in favor of Option 1 – Waiting for things to settle down and buying at the bottom

The market hates uncertainty. Nobody knows what’s gonna happen over the next few months. Chances are the market is going to stay down until somebody finds a sustainable solution to this terrible disease. How can the market price in an unknown unknown like this one? Maybe Mr. Market still hasn’t fully priced in the impact corona is gonna have on various economies / companies / people’s psychology.

The ripple effects of closing down entire countries and restricting movement of people and goods might be a lot worse than the market has already priced. Nobody knows the consequences of consequences of consequencesand so on. Take for example, the price of gold – in a typical market crash, the price of gold tends to go up as investors look at gold as a form of protection but a couple of days back even gold prices went down along with the market. That’s crazy and the thing is almost NOBODY has an answer to why it should have gone down, yet.

This is the time to protect your capital and prepare your family for Financial Armageddon. If Corona doesn’t end the world (as some investors seem to be pricing certain companies), then you might lose gains to the extent of perhaps 20-30-40% from current levels and you should be leaving those 20-40% returns profit on the table for the next guy. Let somebody else take the risk on those remaining small profits(and get back in later).

On the other hand, if the market goes down further, your capital is protected. Between protecting capital and making a return shouldn’t your priority always be to protect your capital? In investing, it’s not how much you make that counts, it’s how much of it you can take home (Basant Maheshwari). Anything multiplied by zero is zero (Warren Buffett).

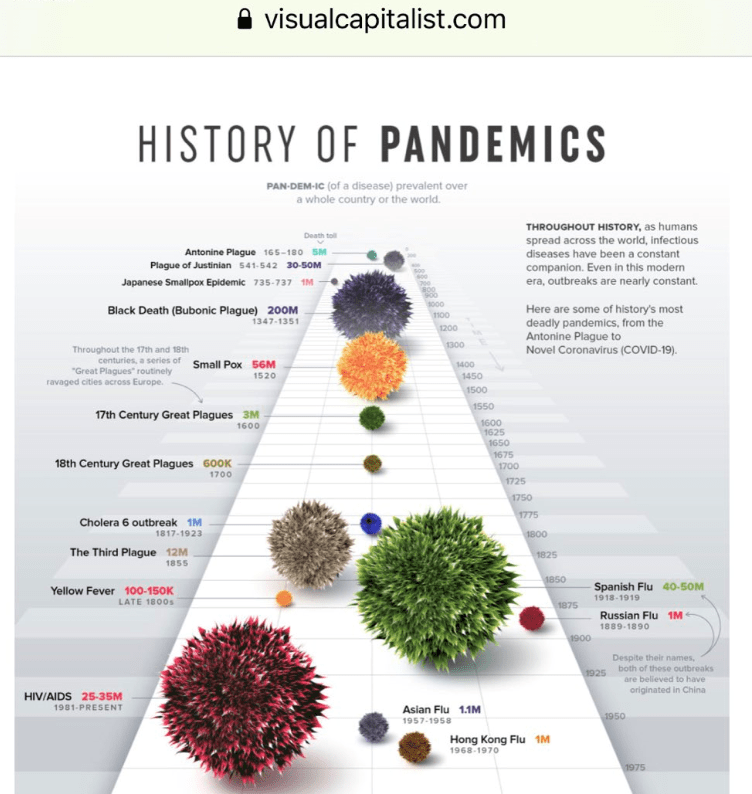

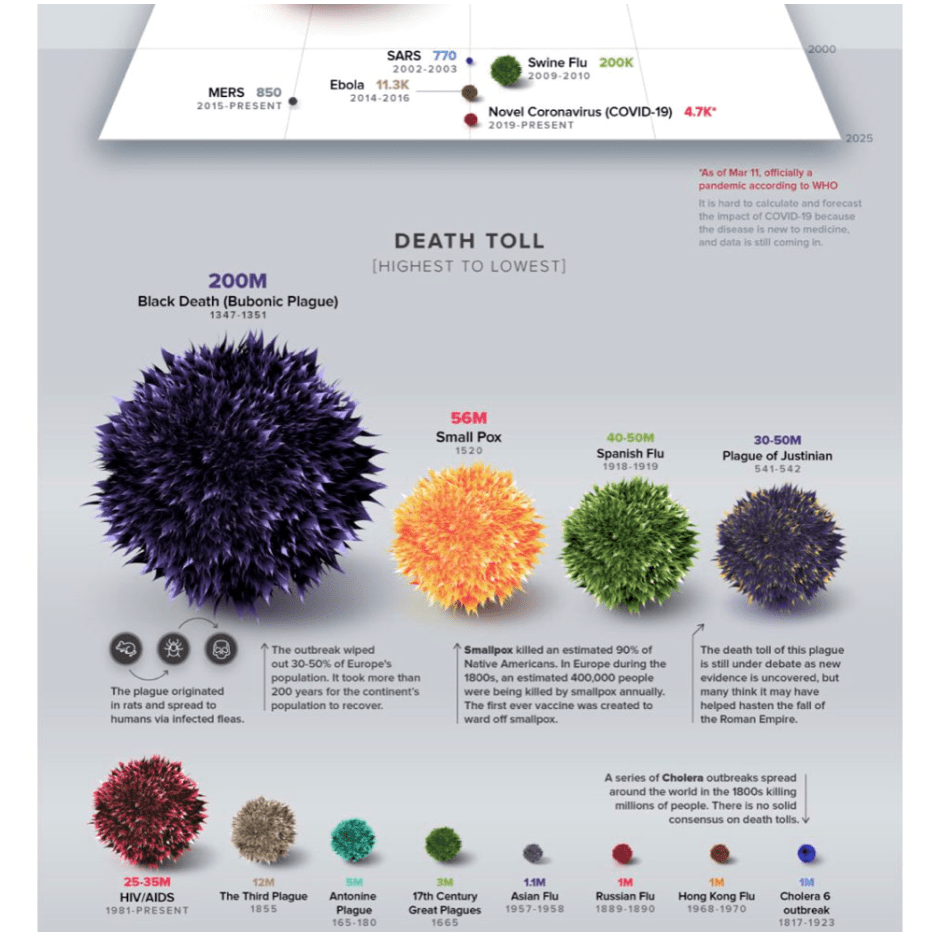

It is not a good idea to compare Corona with pandemics from the past (Like the Flu epidemic in 1918, which killed between 2 & 5 Crore beings or the Cocoliztli in 1576 which killed 2-2.5 Crore men & women and many such diseases) because the world wasn’t as connected back then, as it is today. On the flip side, the world hasn’t seen such a scale of quarantining ever. So the good thing about quarantining is, the Corona might not turn out to be as bad as an epidemic from the past, wherein people would not even have known what really hit them or their loved ones. From reading Taleb I learnt “Things that haven’t happened before happen occassionally” and Corona might as well be one of those “never happened before but happened this time” situations. The proverbial Wolf from the Wolf and the Shepherd story might have arrived after all.

Arguments in favor Option 2 – Buy on the way down (Average down)

Even the experts don’t know how drastic this is gonna be – During the Ebola scare in January 2015, some experts predicted Liberia and Sierra Leone will have approximately 550,000 or 1.4 million total cases, including reported and unreported Ebola cases. (1.4 million assuming there were 2.5 unreported cases for each reported case) The actual number – 21000. That’s way way off. These experts did not think about the second order effects of potential new patients changing their response in response to the Ebola outbreak becoming better known.

Best time to buy is when the macro (economy) is looking bad (Hiren Ved). Clarity is one of the most expensive things to buy in the market (Basant Maheshwari / Ken Fisher).

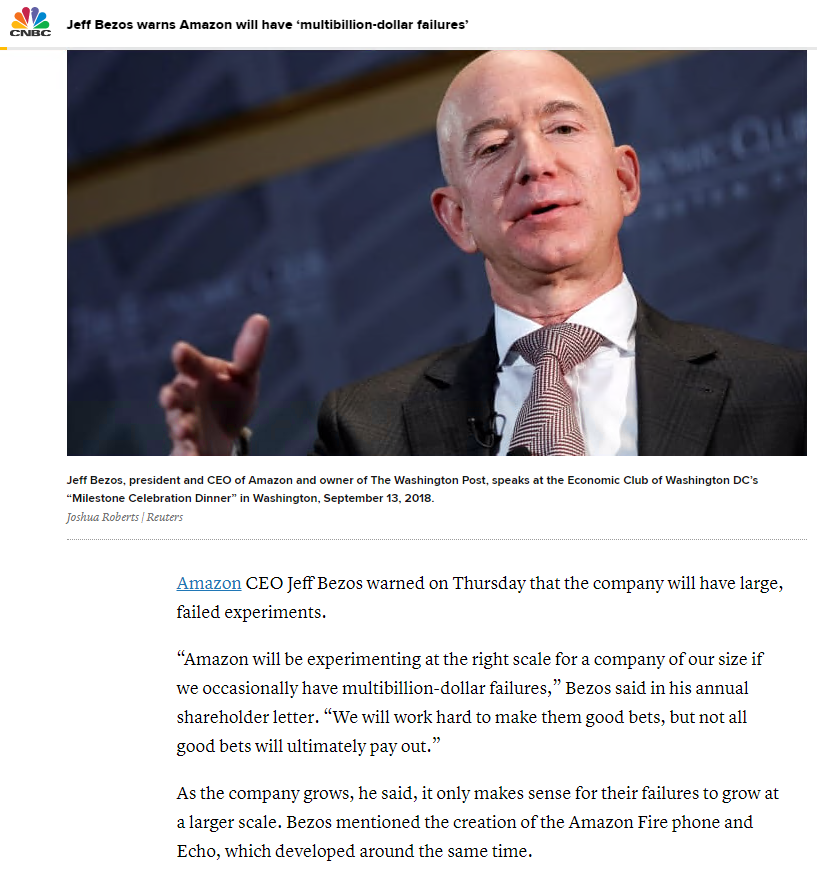

I love this quote from Amazon’s Jeff Bezos – Most decisions should probably be made with somewhere around 70% of the information you wish you had. If you wait for 90%, in most cases, you’re probably being slow. Plus, either way, you need to be good at quickly recognizing and correcting bad decisions. If you’re good at course correcting, being wrong may be less costly than you think, whereas being slow is going to be expensive for sure.

Seth Klarman – You must buy on the way down. There is far more volume on the way down than on the way back up, and far less competition among buyers. It is almost always better to be too early than too late, but you must be prepared for price markdowns on what you buy.

Howard Marks – I’ve never considered it a legitimate goal to say you’re going to invest at the bottom. There is no price other than zero that can’t be exceeded on the downside, so you can’t really know where the bottom is, other than in retrospect. That means you have to invest at other times. If you wait until the bottom has passed, when the dust has settled and uncertainty has been resolved, demand starts to outstrip supply and you end up competing with too many other buyers. So if you can’t expect to buy at the bottom and it’s hard to buy on the way up after the bottom, that means you have to be willing to buy on the way down. It’s our job as value investors, whatever the asset class, to try to catch falling knives as skillfully as possible.

You’ll drink a hell of a lot more Coke if it’s always available. So said Charlie Munger. Just because the price of stocks is “Available” to you daily, should you be selling stocks of your favorite companies that you expect will do well over the next 2-3-5 years or more? Would you do that to a property you own? Suppose, sellers were trading properties daily on a market exchange like the BSE/NSE would you sell and buy the RE property back, after prices started going up? If you’d done that between 2000 & 2010, for most real estate investments, you’d have regretted and perhaps been considered bonkers, unless you were an expert at timing RE investments. Point is just because prices are available, you should avoid getting sucked into consuming (selling at) whatever prices Mr.Market is offering you. You should alse be skeptical about all this noise around Corona.

Remember the 2014 ebola scare? Many people were afraid of infection, but paradoxically, didn’t get a flu shot. Six times as many people died from the flu in the United States than died from ebola worldwide. This is the heart of the availability bias. When something is at the forefront of our thoughts, we assume it to be the correct answer. Sometimes this works. Sometimes it doesn’t, and usually that involves 2nd level consequences.

History has shown Humans have survived several such epidemics. From the book – Guns, Germs & Steel – “Within a year of the first European settlers’ arrival at Sydney, in 1788, corpses of Aborigines who had died in epidemics became a common sight. The principal recorded killers were smallpox, influenza, measles, typhoid, typhus, chicken pox, whooping cough, tuberculosis, and syphilis.”

Bear markets are deceptive. Each bear comes with a different face and Corona could well be one of the many faces we’ll see in our lifetimes of investing.

In 1929 the bear attacked after the roaring 20s bubble burst

In 1987, the bubble was burst due to automated selling which didn’t consider effects of effects of effects.

In 2009, it was the Lehman crisis

In 2020, it is the Coronavirus pandemic

What is my bear market strategy?

Buy in a staggered manner (In addition to stocks that I already own). Deploy cash that I have kept out of the market over the last few years.

Get rid of some CAGR killers that haven’t performed for a while now.

Avoid WhatsApp, Twitter, News channels and other social media. because I feel (& I might be reacting like an Ostrich) the news flow is way too negative than reality and this negative news impacts my ability to take potentially rational decisions.

Undertaker in a plague(Peter Lynch) investment theme. Even in bad times, people will need roti, kapda, makaan, education, medicines, hospitals, etc. The stocks of such companies are likely to do well despite a prolonged impact of Corona.

Pre Mortem – What are the top 3 things that can kill the above idea?

Consequences of consequences of consequences lead to the economy not recovering for a decade or more. Also, when there is trouble, everything corelates (Buffett)

Medical science is unable to come up with a vaccination for 3 or more years.

Leverage could totally ruin some weak balance sheet companies and fragile business models which depend on the kindness of strangers (Warren Buffett).

What do the various role models say?

Taleb says – “Be Paranoid”

Buffett – I don’t know what the stock market will do in the next year. What I do know is that, if you go back to the 20th century, 100 years, you had two great wars, you had other very large wars,you had the Great Depression, you had the FLU EPIDEMIC, you had a dozen recessions and panics, you had all kinds of things.At the end of that century the Amer– the average American was living seven times as well as- the start of the century. The DOW Jones average went from 66 to 11,497. With all those problems

Buffett – “You don’t buy or sell your business based on today’s headlines” — on coronavirus sparking a frantic market sell-off.

Buffett- Although this is scary, it shouldn’t affect what we do in stocks.

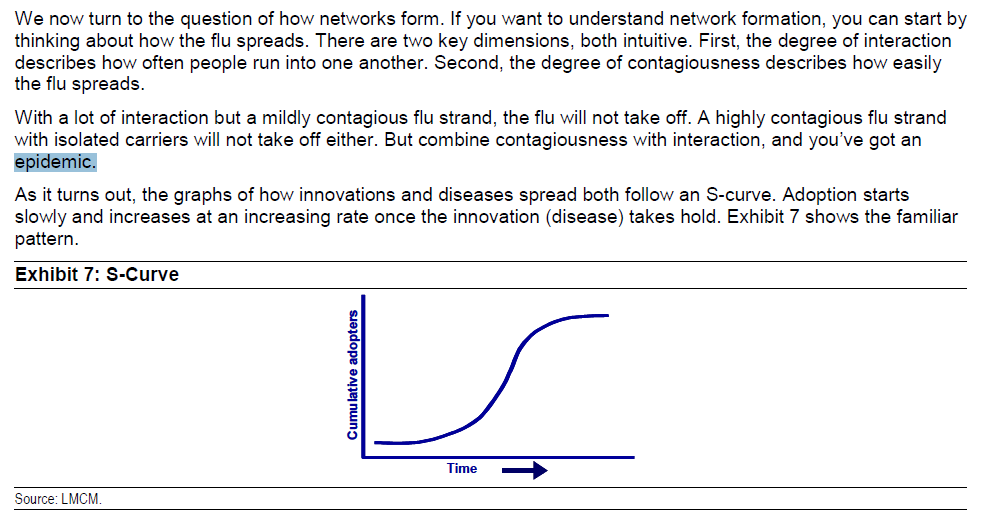

Based on the below snippet from famed Statistician Late, Hans Rosling‘s book, Factfulness, there is a good possibility that the Coronavirus epidemic might die down like the ones that preceded it.

Epidemics tend to follow an S-Curve. They start slowly, grow exponentially and then slow down. In some cases die down.

From some paper about epidemics, that I pulled up while researching Coronavirus – Can’t remember where I found this

Prof. Bakshi – The human mind also has another tendency. It tends to put an arrow at the end of a trend line. Basically the human mind is not wired such as to think in terms of mean reversion. It’s a natural tendency to believe that trends are destiny, but all trends are not destiny and it takes a bit of deprogramming to internalize the mean reversion concept and to use that to come to the conclusion that things will change. It looks bad now or this is too good to be true. This is not normal and the normal is going to come. Of course, there are exceptions, sometimes the trend line is destiny, and sometimes what you see as light at the end of the tunnel is actually an oncoming train.

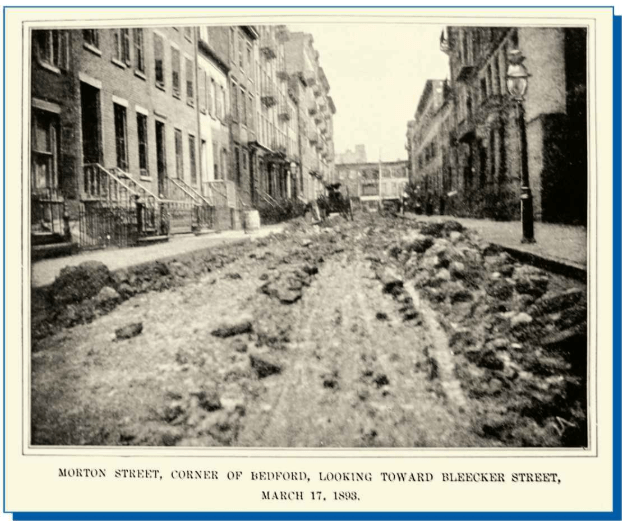

Let me end this post with a seemingly unsolvable problem that New Yorkers faced way back in the late 1800s. When New York city was getting increasingly modern, one of the primary modes of transporting people and products was the Horse Cart. Eventually, it led to a problem. From the Book – Freakonomics – “The average horse produced about 24 pounds of manure a day. With 200,000 horses, that’s nearly 5 million pounds of horse manure. A day. Where did it go? Decades earlier, when horses were less plentiful in cities, there was a smooth-functioning market for manure, with farmers buying it to truck off (via horse, of course) to their fields. But as the urban equine population exploded, there was a massive glut. In vacant lots, horse manure was piled as high as sixty feet. It lined city streets like banks of snow.

Today, when you admire old New York brownstones and their elegant stoops (Staircases), rising from street level to the second-story parlor, keep in mind that this was a design necessity, allowing a homeowner to rise above the sea of horse manure.

All of this dung was terrifically unhealthy. It was a breeding ground for billions of flies that spread a host of deadly diseases. Rats and other vermin swarmed the mountains of manure to pick out undigested oats and other horse feed—crops that were becoming more costly for human consumption thanks to higher horse demand. In 1898, New York hosted the first international urban planning conference. The agenda was dominated by horse manure, because cities around the world were experiencing the same crisis. But no solution could be found. “Stumped by the crisis,” writes Eric Morris, “the urban planning conference declared its work fruitless and broke up in three days instead of the scheduled ten.” The world had seemingly reached the point where its largest cities could not survive without the horse but couldn’t survive with it, either. And then the problem vanished. It was neither government fiat nor divine intervention that did the trick. City dwellers did not rise up in some mass movement of altruism or self-restraint, surrendering all the benefits of horse power. The problem was solved by technological innovation. No, not the invention of a dungless animal. The horse was kicked to the curb by the electric streetcar and the automobile, both of which were extravagantly cleaner and far more efficient. The automobile, cheaper to own and operate than a horse-drawn vehicle, was proclaimed “an environmental savior.” Cities around the world were able to take a deep breath—without holding their noses at last—and resume their march of progress.

This is perhaps not very surprising. When the solution to a given problem doesn’t lay right before our eyes (Think Coronaas it stands today), it is easy to assume that no solution exists. But history has shown again and again that such assumptions are wrong. This is not to say the world is perfect. Nor that all progress is always good. Even widespread societal gains inevitably produce losses for some people. That’s why the economist Joseph Schumpeter referred to capitalism as “creative destruction.” But humankind has a great capacity for finding technological solutions to seemingly intractable problems, and this will likely be the case for global warming (Again think Corona). It isn’t that the problem isn’t potentially large. It’s just that human ingenuity—when given proper incentives—is bound to be larger. Even more encouraging, technological fixes are often far simpler, and therefore cheaper, than the doomsayers could have imagined.

I presume, somebody is gonna figure out a solution to a terrible problem that impacts the world we live in, sooner rather than later.

Buy now or wait till a lower bottom – I bet nobody knows and so do I. What I do know, is some of these businesses will thrive, a couple of years from now and today is the time to think and act long term, not short term.