Let’s do a thought experiment. It’s August 1997 and you are in the trading ring at the Bombay Stock Exchange. In between the chaos of that place, there are thousands of listed companies. An investor friend, tells you “Buy Infosys”. You are unconvinced and don’t buy because you’ve burnt hands buying stocks recommended by others before. And you forget about the co.

The question I am seeking an answer to is – If Infosys subsequently became a mammoth wealth creator, why didn’t a lot of investors buy it in the early 90s? What biases were involved in causing the massive opportunity loss that followed, due to not buying the stock of this co.?

Let’s go back in a time machine. Here’s what it looked like in mid-1997.

ROE for all 5 years kept increasing YoY and ranged between 21% and 33%.

The P/E ranged between 15 & 25.

Infy also had a 15 year track record of growing sales at 28% CAGR from 1982 to 1992. So even in 1997, it was not some microcap co. with no track record. It was a fast grower for 15 years, with decent credentials.

Let me quote what some veteran investors have said about Infosys and other technology companies of that era.

Basant Maheshwari – “Between 1994 to 1998, Infosys came right under my nose. We saw their good results, but there was always these thoughts like – “Who would buy Infosys if you take away all their employees tomorrow?” or “It only has computers and chairs and what are those worth for?” or then “I can create an Infosys by hiring all those people.”

Anil Goel – “I had never invested in IT companies. I didn’t understand that business and I did not understand the valuations. The valuations just did not make any sense. The market cap of one Computer Education Company exceeded the combined market cap of the few large conglomerates at that time. That saved me from technology crash of 2000.”

Here’s how the company’s market cap went ballistic, 1997 onwards.

1997 to 1999 – 19 x

1997 to 2000 – 127 x (not excluding new shares issued)

What would have happened if one had purchased the stock in 1997 or prior to that?

Assuming most people could not sell Infy at it’s peak, they would have still done well, had they bought the stock prior to 1997 and sold it post-crash, in 2001.

The point I am trying to make is, just like one cannot be right all the time, one also cannot be wrong all the time either. What was a growth stock for 6 years (1993 to 1999), became a bubble stock in 2000 and most people who bought in 2000, were likely to have been nastily injured. Had one purchased the stock any time between 1993 and 1998, they’d still have done well.

Ramesh Damani, who understood Infy, due to his technology background and made a ton of money from it’s stock, said “Lot of the old hands in Dalal Street didn’t understand technology since there were no physical assets, and all the real assets walked out at five in the evening. They had no idea how to value these companies.”

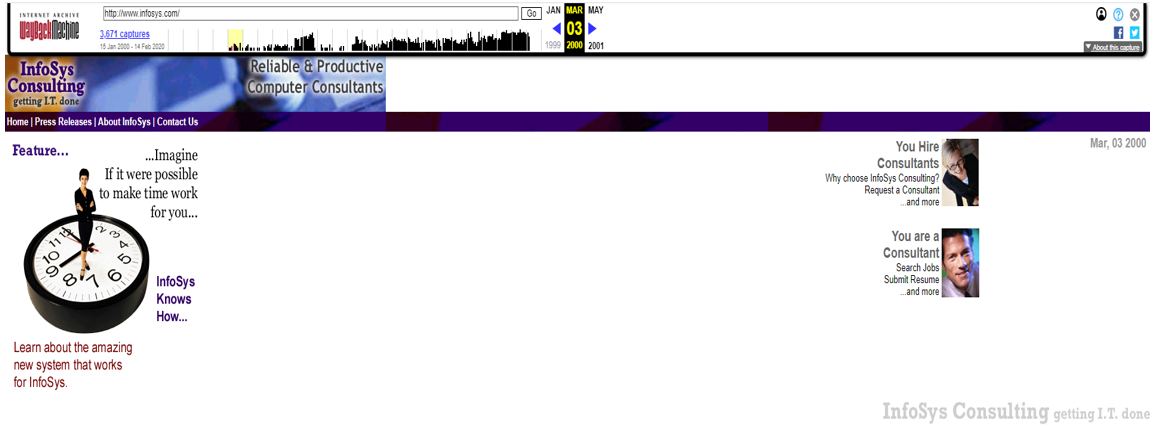

Would it have been easy to buy this stock without a tech background? No. As a wise investor once said “The risks of this trade always appear lower, after the rewards have been made.” Here’s what Infy’s website looked like in 2000. No investor relations. No annual report PDFs. This was the world back then.

Now let’s look at the situation from the perspective of an investor who had NO tech background.

I am not trying to find fault with investors who didn’t invest in Infy. I totally respect the wisdom, the investors I’ve quoted, have. I am just trying to present the situation from various vantage points, as investors saw it back then.

Here’s what Raamdeo Agrawal’ investment thesis in Infy was, in 1997 (I have shortened & rephrased this a bit). He had NO tech background, just like most people of that time.

“In the Y2K boom, we made Rs. 100 crore. We were 80% invested in technology, 40% of which was in Infosys. Mr. Narayana Murthy taught us that Indian cost was unbeatable. What Americans were doing in Boston for the last 20-30 years, Infy was doing for 1/5th or 1/6th the cost. Due to a friend’s suggestion, to learn about globalization, I started reading The Financial Times, The Economist, Business Week and Fortune. Somewhere in 1997, I read about the effects and challenges of Y2K. It explained what problems would occur when the systems would change from 1999 to 2000 and how it will need to be changed in computer systems for continuity of various industries. I could see a big elephant approaching and that the gate is small. And that it is a dated event. In the market, you rarely get to know about a future event that is dated, that this transition has to happen in just 3 years. The demand was high and the supply was not as much. The IT companies were growing at 100%, but were still available at 20 P/E in the beginning.”

Selling a bubble stock

Ramesh Damani – “When we saw that the 2000 Technology, Media & Telecom (TMT) bull market was getting over, I realized that these values wouldn’t hold. Infy was trading at 150+ forward P/E. Even if you try to hold the stock, the markets rattle you out of the position. Infy went up three straight circuits to Rs. 13,000 and then started falling. So when it fell to Rs. 8,000-10,000 levels, I sold it, as I could not handle the stress of holding it since so much money was involved.”

Raamdeo Agrawal -“When these companies were trading at 100-200 P/E, we did start selling. I started selling Infy at 11,000 per share. And I sold the last bit in September 2001, at around 2,500.”

Rajashekar Iyer – “My 1995 experience had taught me that when stocks are highly overvalued and start declining, the safe course is to sell them and not be a ‘long term investor’. All IT stocks were tremendously overvalued by Jan 2000 and so when they started falling in February, I sold them as quickly as I could. I could not sell at the peak, mostly 15% down from the peak. One IT company’s stock that I had bought at Rs. 60, came down from Rs. 510 to Rs. 360 by the time I could sell. I sold it almost 30% down from the peak, but it finally ended at Rs. 12.”

Conclusions:

- For most investors, it takes a lot of time to adapt to new business models created by the arrival of new technology. Learning about these new business models quickly is sometimes the difference between great returns and mediocre returns.

- Holding such investments is never easy. Think how difficult it is, to own Bitcoin today, given all the noise. I don’t own it btw.

- Having bought early, if you find yourself invested in a bubble, stay put. Booking some profits intermittently and keeping trailing stop losses may be a good strategy, although stop losses may not help at times, given that there could be severe gap downs and no buyers.

- Cut losses quickly. If you don’t, you may find yourself holding a loser for 8 years. (It was not until 2008, when Infy crossed it’s 2000 high price).

- No matter how good a business or a management team is, at some price it becomes stupid to buy it.

Barath Mukhi

6th-March-2021