Here’s a story of Ajanta Pharma, a business which created tremendous value for it’s shareholders between 2010 & 2016.

Buying & holding such a stock must be easy. If you are a little late for a 120 bagger party in a stock like Ajanta Pharma, just follow the strategy of buying at 52 week high prices and you should have the next big stock in your portfolio. Just buy and forget. Correct?

The above chart is full of hindsight bias. And I am here to tell you why.

Based on some 900 odd posts I read about the company, across this time period, below are the concerns, investors had with regards to buying or continuing to hold the company’s stock.

As we can see, people were full of concerns about this phenomenal wealth creator. Holding this stock, would have in no way, been easy. At 11-15 PE, in Aug 2012, Mr. Market thought, the re-rating was over. And this might have been a reasonable assumption to make, back then, given all the risks involved in the stocks of a Pharma co. Eventually, the stock hit 40+ PE.

Had the story played out differently, I wouldn’t be writing this post today.

Take-aways from this story:

Holding multibaggers (particularly in Pharma) is gut wrenching.

Do not invest in any Pharma co. without understanding the risks involved.

There will be long spells where you may question your thesis. You may have doubts in your head, making it difficult to hold. You may wonder whether you have invested in the right co. at all. This would be the time to go re-check your facts about the co. If your facts are supporting your thesis. just hang in there.

Is the current rally in Pharma stocks like Alembic, Aarti & Laurus (current sector leaders & market favorites based on growth in sales & profits) being driven by supply chain disruptions due to Covid19 or is this a secular growth story we investors are looking at?

Will investors lose money yet again, chasing hot stocks of a sector, everybody’s talking about?

To the answer this question, lets look at the sales data for all 3 companies.

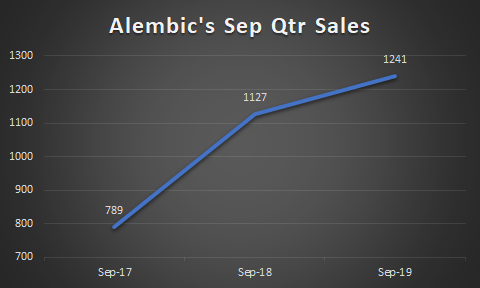

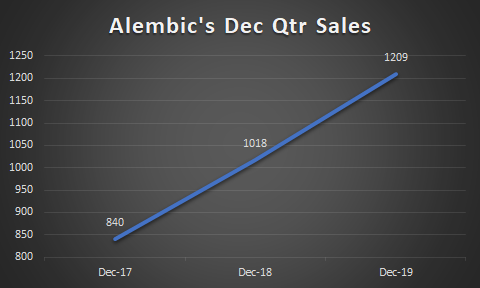

Alembic Pharma

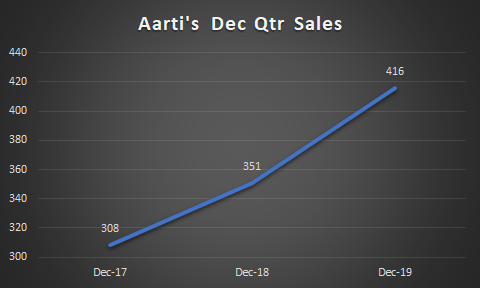

Aarti Drugs

From Aarti’s Q4 FY2020 Concall

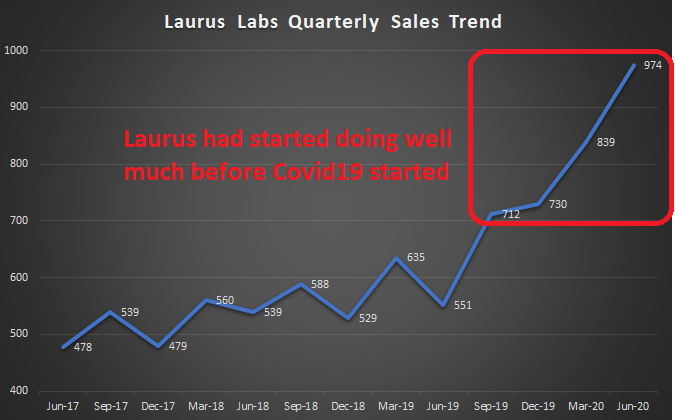

Laurus Labs

Conclusion

The consistent growth in quarterly sales of sector leaders from the API segment is suggesting that certain tailwinds are helping the API sector (Laurus & Aarti), and this is more likely to be a long term trend rather than a one-off jump in performance due to Covid19 disruption. As the above charts depict, both Aarti & Laurus started doing well, at least 2 quarters before Covid19 disrupted API supplies.

Meanwhile, Alembic started doing well (Most of Alembic’s sales come from Generic drug exports), due to it’s focus on R&D and strategizing well, much before Covid19 tailwinds came by.

I believe, (and could be wrong), all 3 companies are likely to do well over the short to medium term because of the reasons mentioned above.

Disclosure – I and my clients have substantial positions in Alembic Pharma and Laurus Labs and my views are certainly biased. As of 19th August 2020, I do not have a position in Aarti Drugs. This blog is not to be construed as an investment advice. Please consult your investment advisor before investing.

Disclaimer: This is NOT investment buy/sell/hold advise. I am not SEBI registered. May change stance on above businesses anytime with new developments and/or new insights, and/or overall market conditions. May NOT be able to update periodically. Please do your own diligence and/or take professional advise, before investing.

Firstly, I have been invested Laurus Labs since 600 odd levels and added more on the day this company declared Q1 FY2021 Results. Currently this co. forms a little over 10% of my portfolio.

Here’s how I thought about the company before investing.

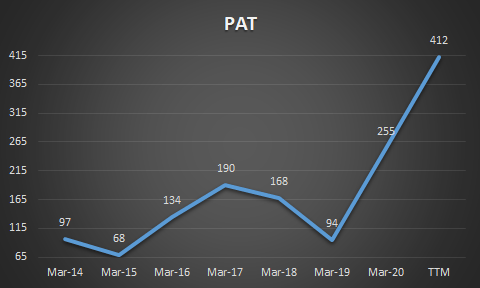

Firstly, sales had been growing well.

I love straight lines, particularly the ones that are goin’ up and indicating there’s something nice cooking there.

Q1 FY2021 Revenue sources

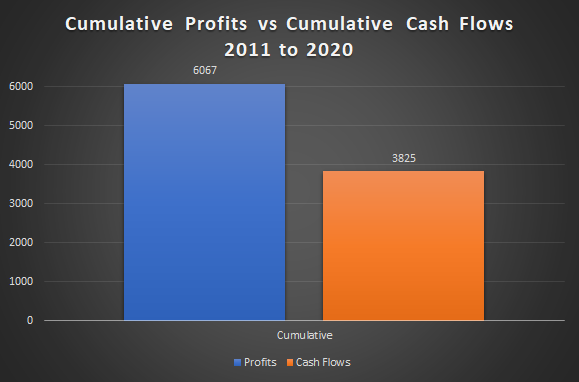

Cumulative cash flows vs Cumulative profits are good.

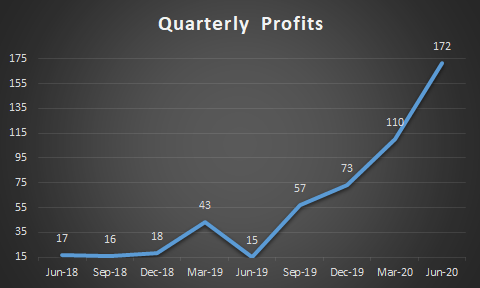

Quarterly Sales were showing a nice uptrend. The co. had been on my radar since Mar 2020 because it had shown 2 quarters of growth in sales as well as Profits. In retrospect, I could have bought it a little earlier.

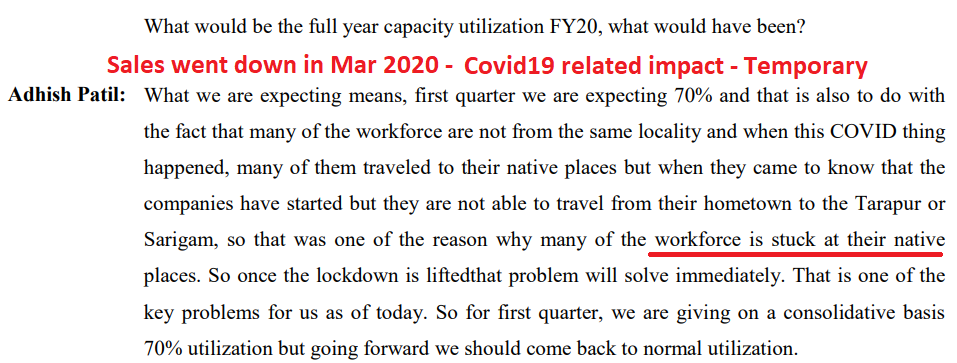

Anyway, the below increase in sales and profits should be seen in the context of the current Covid19 situation where every other business is struggling.

But see what was happening here, at Laurus.

5 quarters of increasing sales and profits in an environment where lockdowns and job losses are the norm, at least temporarily. Wow!

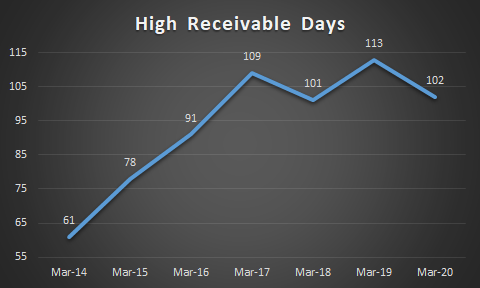

What got me worried though, was the trend in receivable days. Almost a third of the companies sales are being done on credit and not cash.

So, I came across a superb thought by another investor who said, receivables in the pharma sector usually don’t end up being bad debts and write offs because transactions between the seller and the buyer are usually over several years and customers are likely to be dependent on Laurus for future supplies. A data point to validate this would be the company’s sales growth. So there seems to be good demand for the company’s products and write offs seem unlikely.

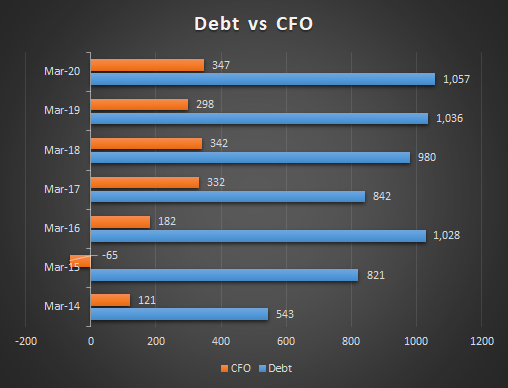

High debt

Debt is 3 times cash flows generated by the co. If good times continue, then the co. may be able to pay off their debt in due time.

Debt to Equity at 0.6x. The cost of debt as per the company’s latest concall is 6.6% which provides some comfort because it is way lower than the Return on Equity of 15% delivered by the co. in FY 2020. And this ROE was delivered despite a significant amount spent on Capex.

Free Cash Flows – From the company’s FY2020 Annual Report

Changing Revenue Mix

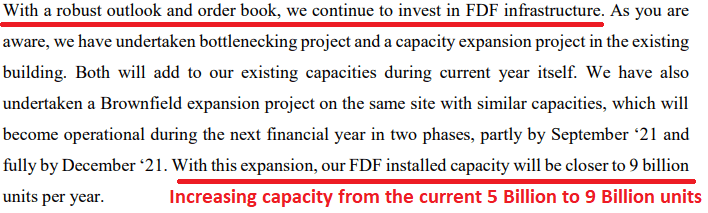

Booming Generic Finished Dosage Forms Business (FDF)

In Q1 FY 2021 alone, the company’s Generic FDF division delivered sales of 351 Crs compared to 46 Crs in all of FY 2019 and just 6 Crs in all of FY 2018.

Growth expected to continue in FDFas per Q1 FY2021 Concall

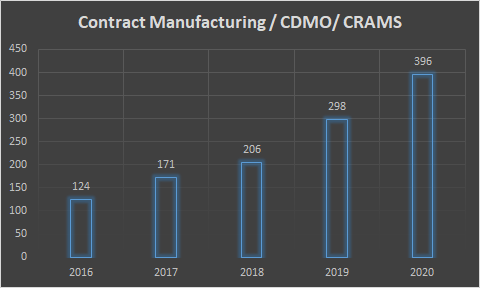

Booming Contract Manufacturing / CDMO / CRAMS Business

Growth in CRAMS expected to continueas per Q1 FY2021 Concall

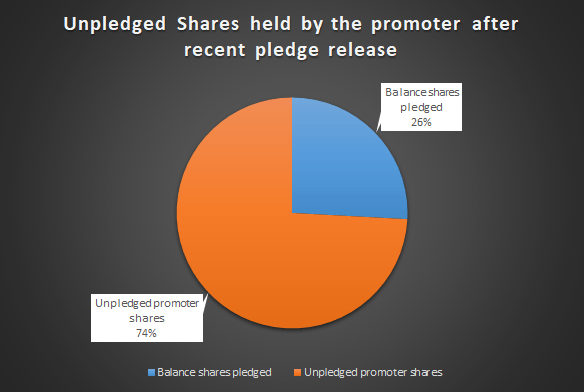

Pledged Shares

There are concerns that promoters have pledged shares and this combined with the fact that this co. is based out of Hyderabad (rings a bell, fellow investors?) seems to make a lethal combination. Doesn’t it?

So as per a recent disclosure the 3 promoters who have a cumulative 1 Cr shares pledged out of their total holding of 3 Cr shares, recently got 25 lac shares released from Axis Finance Ltd.

The below graph shows the 3 promoters still own a lot of unpledged shares in the company. Besides, promoters of fast growing manufacturing companies are often expected by lenders to pledge shares to ensure skin in the game. So the promoters pledged a third of their stake to do capex and grow the business, which is fine, in my view.

I bought the stock at a little below 20 times FY20 earnings. For a fast growing co. with a reasonable ROE of 15%, and with tailwinds due to global supply chain disruptions, this is an attractive valuation in my view.

Free Cash Flow vs Growth

Some investors recently raised a red flag about the company lacking free cash flows, on Twitter. This is the typical debate that occurs between a value investor and a growth investor.

Growth investors want the co. to keep reinvesting as long as there are good opportunities for high return on capital growth.

On the other hand some value investors look for companies with cash on their books. I counter that by saying that the markets reward companies that can reinvest all that money and keep the ROE above the critical threshold of say, 15%. Mr. Market doesn’t like companies keeping cash in the bank and I have a ton of such examples.

Promoters

Day to day affairs of the co. seem to be headed by Dr. Satyanarayana Chava. He started the co. in 2007 by investing Rs. 60 Crores of his own money.

It is a phenomenal achievement to have reached 3000 Crs + Revenue in a span of 13 years. So, the gentleman certainly knows what he’s doing. In the past, he was the COO of Matrix Laboratories and has a few decades of experience in the Pharma industry. It always excites me to partner with first generation businessmen who’ve come up the ladder despite all the challenges they might have faced in their entrepreneurial journey.

Risks

Around 15 to 20 Crs out of Q1 FY2021 profit of 172 Crs came from Forex gains. So Forex gains contributed about 10-11% of last quarter’s PAT. This may or may not continue depending upon currency movements.

Increase in interest rates could lead to pressure on margins, if debt is not reduced.

If demand tapers off, then Capex cost may not translate into profits.

Who succeeds Dr. Chava in the future will decide the growth trajectory of this co. whenever the time comes from him to step down.

Disclosure – I and my clients have substantial positions in this company and my views are certainly biased. This blog is not to be construed as an investment advice. Please consult your investment advisor before investing.

Disclaimer: This is NOT investment buy/sell/hold advise. I am not SEBI registered. May change stance on above business anytime with new developments and/or new insights, and/or overall market conditions. May NOT be able to update periodically. Please do your own diligence and/or take professional advise, before investing.

Alkem Labs seems to be an upcoming investment opportunity in Pharma, a sector which has tailwinds in it’s favor, during the ongoing Covid19 situation. Here are my thoughts on why this company could turn out to be an interesting investment candidate.

Sales from various businesses in FY2020

The company’s Domestic as well as US businesses demonstrated good sales growth in FY2020.

FY2020 Sales growth in various segments

Consistent growth in domestic as well as export portfolios

Overall sales trends over the years

PAT trends over the years

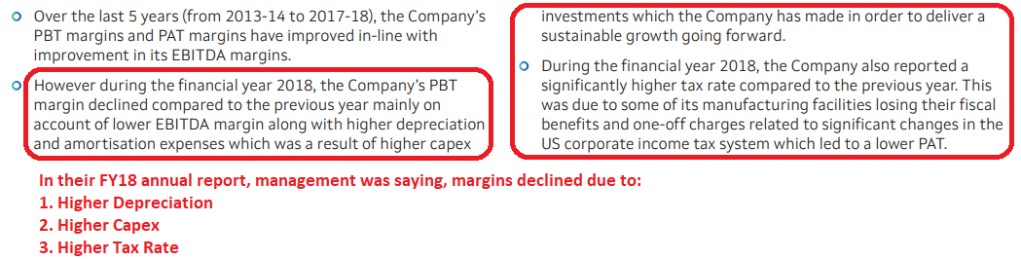

So, one may observe profits went down from 892 Crs in FY17 to 631 Crs in FY18. Let’s dig into why there was a drop of 261 Crs in FY18 despite Sales going up that year.

Snippet from the company’s FY2018 Annual Report

The company’s 2018 Annual report does show that their Tax expense increased from 60 Crs in 2017 to 287 Crs, an increase of 227 Crs. This tells us that a good chunk of the drop in profits was due to the increase in taxes.

Return on Equity – A good return on equity is at least twice the current AAA bond yield. Why? Because, over the long term, return from an equity share almost always equals the ROE delivered by the company. In the short to medium term though, PE expansion can deliver much more than ROE. So, if you are taking all those risks attached to equity investments, and you are investing for the long term, you should at least be demanding twice the risk-free return offered by government bonds. The current bond yield in India is about 6% & twice that would be 12%, which is the benchmark ROE one should look at.

Risks

Credit sales for Alkem are on the rise. This is particularly critical for domestic focused companies like Alkem because the laws pertaining to collecting dues in India aren’t perceived to be as easy as collecting dues from customers based in developed countries, where the laws are more stringent.

The company isn’t very good at converting profits into cash flows.

Let’s take a look at the Cash Flow Statement for FY2020

So as we can see, 21% of the company’s FY2020 profits went to receivables, 12% went to loans given and 23% went to inventories, resulting in profits not getting converted to cash flows. Just 52% of the company’s PAT was converted to cash and that’s not good.

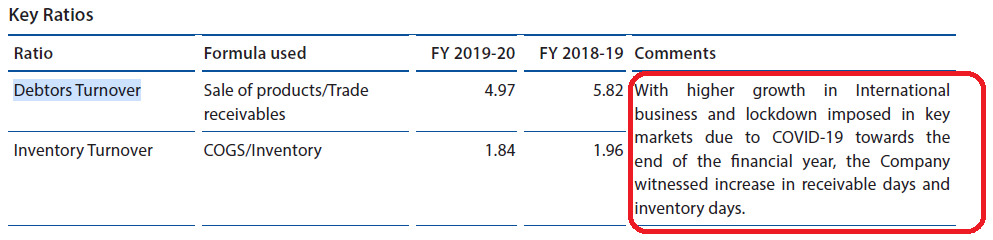

The company’s FY2020 annual report offers some insights into their current status of receivables.

The company’s FY2020 annual report also states the potential impact of Covid19 on further issues with their cash collections (Increase in receivables from customers as well as a pile up of inventories in their warehouses)

The Case for high receivables Now, one of the investors I highly respect, mentioned this recently – “Receivables in pharma sector usually don’t end up being bad debts and write offs because the relationships between the company and its clients are multi year and hence there is a lot of inter dependence.”

Conclusion The company has been growing really well in both, domestic as well as international businesses along with a good return on equity.

Key surveillance items

Receivables may further go up due to the impact of Covid19

Domestic sales may get impacted due to the company’s sales team not being able to meet doctors

Inventories pile up because of point # 2, further impairing the company’s working capital position, at least temporarily

Disclosure – No positions in this stock as of writing this blog. This is NOT investment buy/sell/hold advise. I am not SEBI registered. May change stance on above business anytime with new developments and/or new insights, and/or overall market conditions. May NOT be able to update periodically. Please do your own diligence and/or take professional advise, before investing.