“The most important thing in communication is hearing what isn’t said.”

Below, I will try to cover ideas that are implied in One up on Wall Street, but aren’t explicitly stated or points that don’t get as much attention as they actually should, in my view.

Be obsessed with financial history

Peter Lynch was a master of gathering data for companies that had done well in the past. It must have been like going back in a time machine and figuring out what had worked and what had not worked, in the market, in the 1950s, 40s, 30s and so on.

I speculate that Lynch simulated successful investments before his time, copied key ideas, and followed the advice subsequently outlined by “Bond King”, Bill Gross.

For example, Lynch quotes the example of Masco Corp.

“And how about Masco Corporation, which developed the single-handle ball faucet, and as a result enjoyed thirty consecutive years of up earnings through war and peace, inflation and recession, with the earnings rising 800-fold and the stock rising 1,300-fold between 1958 and 1987? It’s probably the greatest stock in the history of capitalism.“

Peter Lynch was born in 1944. And he’s talked about Masco doing well since the 1950s, at a time when he was a teenager. He probably gathered historical data for Masco from Value Line publications or from Masco’s historical annual reports.

He (or his team) was doing this in a world without the internet. The lesson for us is to have access to the right kind of data and make sense of it. Over time, dot-connecting, recallable, well organised data, becomes a remarkable informational advantage.

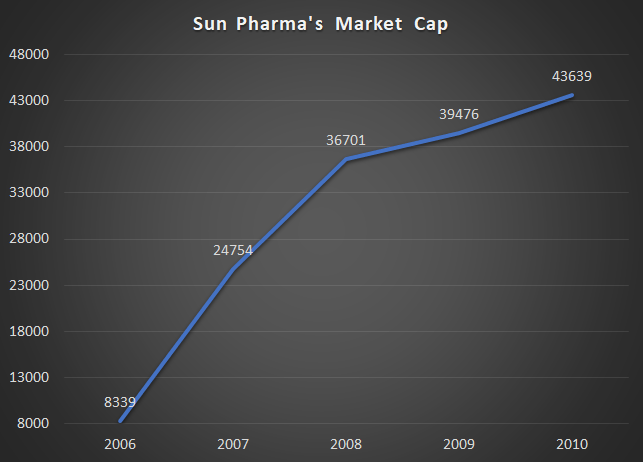

For example, a widely used metric by some very smart and experienced investors today, compares the cash flow from operations to net profit declared by any co. over a few years. Cash flow of below 80% in comparison to declared profits, is usually a red flag. Consider one company’s CFO to PAT from 2006 to 2010, for instance.

Looking at the above table, a forensic accounting focused investor might have come to a conclusion that this company was destined for failure because the co. was probably not managing it’s working capital well (trade receivables, payables & inventories). But surprise, surprise.. The above is data for the stock of an Indian wealth creator, Sun Pharma. Despite low CFO vs PAT, Sun Pharma’s market cap went up by 5x, EPS went at 18% CAGR while the market doubled the stock’s PE multiple, between 2006 & 2010, and way higher, subsequently.

Sun Pharma is an exception rather than a rule and most co’s that did well in the past, had high CFO in comparison to PAT. However, studying this historical example tells us one should look at the holistic picture rather than just one metric (like CFO vs PAT) and then decide whether or not a business is worthy of your investment.

Or how about breaking some notions, using history as a guide?

| Notion | Exception |

| Cement companies don’t create value because they are cyclical businesses | Shree Cements grew it’s earnings at a CAGR of 45% for 13 years (2004-2017) |

| PSU stocks are always wealth destroyers | BEML grew it’s earnings at 110% CAGR (2002 to 2007) |

| Retailing is a tough business | Pantaloons Retail’s stock went up by more than 300x (2001 to 2008). Thanks to a boom in retailing. |

Coming back to the book, Lynch has also studied about Electric co’s being fast growers in the 1950s and 1960s and about buying great companies that that did well despite the great depression of 1929-1934. Going back in time machines gives you perspectives like nothing else.

Reject businesses quickly

In a separate interview, Peter Lynch had said his philosophy was “The person who turns over the most rocks, wins the game.”

Now you may say, “But, I don’t have time to read these many annual reports.”

Mr. Lynch has partly answered this question too, in the book. He says “there’s a way to get something out of an annual report in a few minutes, which is all the time I spend with one.”

My guess is he must have figured out a way to quickly glance through the financial statements based on 1-2-3 parameters. He must have been thinking –

- Oh, too much debt. Skip.

- Oh, declining sales/profits. Skip.

- Oh, they have an unsexy product. Skip.

- Oh, this business has been growing really well. Hmmm.. Let me spend some more time on this.

And so on..

In another book, Rajashekar Iyer articulated this aspect well – “If you are able to look at 100 companies faster than others, you can find the two good companies which are really interesting. If you are slow in rejecting, you will only be able to look at 10 companies. It’s like reading. If you read 20 books in a month, you may find two good books. If you just read two books in a month, you may find only two good books a year. It is similar in stocks. So if you tell me that you like a particular stock – how much time do I have to spend on the company before I can say it’s not for me? If I can do that fairly fast, then I can look at more ideas in the time available.”

In a world, where we have beautifully designed investor friendly websites like screener.in, turning over a lot of rocks should be easy. If Lynch could do it without screeners, we can at least do it with all the luxury, the net gives us. No?

Conclusions: Gather data and analyze companies that did well before you became an investor. What were their failure patterns? What were the patterns of success in companies like Asian Paints, Pidilite, HDFC Bank, etc?

Turn over a lot of rocks, every single day, to find those hidden gold nuggets. Figure out a way to reject companies quickly and put most of them into your too hard pile.

Barath Mukhi

25-Jan-2021